Relationship between Cost of Production and Sales Volume:

The cost of production and volume of sales are the inter-dependent determinants of profit. The analysis of cost behavior in relation to the changing volume of sales and its impact on profit is very important to determine the break even level of a firm.

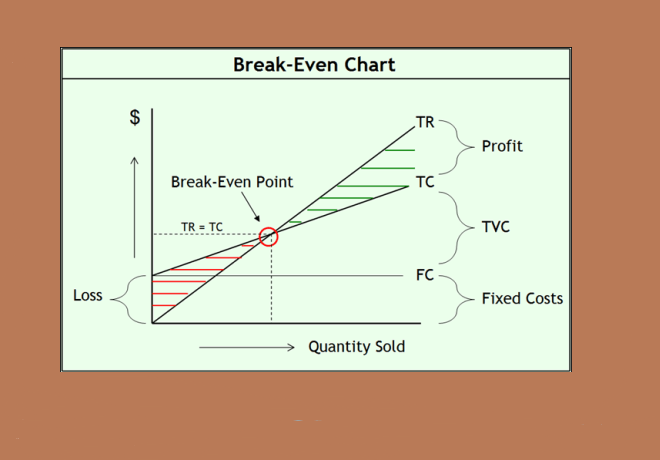

The level at which total revenue equals total costs, is said to be the break even level where there is no-profit or no-loss. Sales beyond break-even volume bring in profits.

Generally production is preceded by the process of demand forecasting, to decide on the volume of production, the produce of which will be absorbed by the market. Pricing and promotions come at a later stage. Costing is done to predict the costs of production and resultant profits at various levels of activity.

Cost Volume Profit or CVP Analysis:

CVP analysis or Cost-Volume-Profit analysis helps a firm to study the interrelationship between these three factors and their effect on clean profit. The process also includes an analysis about the external factors that affect the volume of production, such as market demand, competitor threat and internal factors such as availability of infrastructure, capital and labor force.

This CVP analysis is a boon to the managers to locate the bottlenecks that hinder the productivity and find a way out, by adjusting either the levels of activity or controlling the cost.

Picture Courtesy : The Power of Break-Even Analysis

Pricing:

Pricing is the most important factor that makes your product competitive. The costs of production can be classified into fixed costs, variable costs and semi variable costs.

Fixed costs remain constant and tend to be unaffected by the changes in volume of output; whereas variable costs vary directly with the volume of output and semi-variable as the name implies are partly fixed and partly variable.

Cost accountants of the modern era fully support variable costing for the purpose of cost accounting, listing its merits as follows:

Some applications of variable costing that facilitates management decision making:

Budgeting:

Flexible budgeting and cost control are possible by variable costing technique and the striking feature is the treatment given to fixed costs, where it is treated as a period cost and not apportioned among all the departments and products that enable the firm to understand the movement of profits in the same direction as that of the sales.

Although considered to be a controversial technique and weighed against the conventional methods of costing such as absorption costing, it is believed that it is to stay and exist as the next step in the evolutionary method of cost accounting.

Note:

© Copyright 2022, Managementguru.net. All Rights Reserved.