Accounting is not to be feared

Accounting is a subject that is intertwined with our day-to-day lives yet people think it is quite a complicated subject to deal with.

The fancy of the subject is such, that many of us fail to understand that it is quite simple, un-complicated and all it talks about is balance.

Rather than barging into equations that make us grip with fear, let us start with the basic question of WHAT=WHO?

“What” deals with whatever we have in hand or otherwise ASSETS and “Who” deals with the claims, both other’s claims and our own claims on the product we have in hand.

Other people’s claims are known as LIABILITIES and our own claim on the product is called Owner’s equity.

Now if we take “WHAT=WHO”, it can be translated into the following equation ASSETS= LIABILITIES+OWNER’S EQUITY

Accounting: Get Hired Without Work ExperienceUNDERSTAND WHAT = WHO

What = Who

Stuff = Who

Assets = Who

Assets = Who Has Claim

Assets = Claims

Assets = Other People’s Claims + My Claims

Assets = Liabilities + My Claims Assets = Liabilities + My Equity

Assets = Liabilities + Owner’s Equity

Simple Equation to Remember

There are two types of claims: other people’s claims and my claims.

Assets = Other People’s Claims + My Claims

Claims are also referred to as equities.

Assets = Other People’s Equities + My Equity.

Accountants have a fancy word for other people’s equities. These are known as liabilities.

Assets = Liabilities + My Equity

Because I am the owner, we will call My Equity Owner’s Equity.

Assets = Liabilities + Owner’s Equity

This is the formal equation of accounting. The structure of accounting is based on this one perspective. Accounting students memorize it. And try to decipher it. You are way ahead of the game because you understand that what = who!

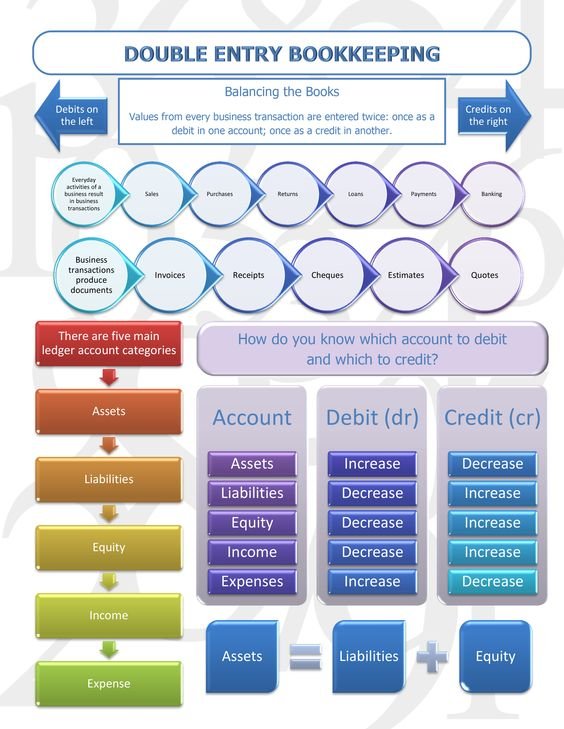

WHAT ARE ASSETS AND LIABILITIES

Assets are on the left of the Big T. Asset accounts increase with debits. Liabilities and Owner’s Equity are on the right of the Big T. They increase with credits. Income ultimately increases owner’s equity so it behaves like owner’s equity: it increases with a credit. Expenses increase with debits. The best way to improve your expertise in accounting procedure is to practice; in due course your hand movement and thought process start synchronizing.

Examples of Asset accounts – Vehicles, Furniture, Cash Examples of Liabilities accounts- Accounts payable, Owner’s equity

ASSETS (what) = LIABILITIES + OWNER’S EQUITY (who)

Say if you invest Rs.5,000 as down payment from your end and take a loan of Rs.20,000 from the bank to purchase the product.

Now, the bank has a claim on your asset to the extent of Rs.20,000 and your claim is Rs.5000.

Here liability is Rs.20,000 and Owner’s equity is Rs.5,000.

On the asset side we have a TV worth Rs.25,000

You can see that the value of the asset is equal to the value of liabilities, i.e., what = who.

ASSETS = LIABILITIES + OWNER’S EQUITY

25,000 = 20,000 + 5,000

Just how you see a hand with five fingered palm on one side and five fingered nails on the other side, this accounting equation has two different perspectives to strike a balance between assets and liabilities.

The Big Balancing ‘T’ BIG “T” FOR PRODUCT PURCHASE

WHAT (ASSET) VEHICLES (Rs.25,000) = WHO (LIABILITIES) ACCOUNTS PAYABLE (Rs.20,000) + PAID IN CAPITAL (Rs.5,000)

Big Balancing ‘T’

When we receive cash for completing a consulting job we know that cash has increased so we debit cash.

The corresponding account must then be credited. In this case we credit Consulting Revenue.

When we write a check for our utility bill, cash is credited: it goes down.

The corresponding account must then be debited. We debit Utilities Expenses.

The best way to understand debit or credit is to understand what effect it has on the cash account. If the cash increases – we debit; if it goes down we credit.

Example of debit and credit

Dr. VEHICLES Cr. Dr. OWNER’S EQUITY Cr.

2,000│ │10,000

CASH

10,000│2,000

———————–

8,000- Balance in cash a/c + 2,000 in vehicles a/c = 10,000 in owner’s

Equity.

In the example above, a sum total of Rs. 10,000 is invested in a new business venture. A two wheeler is purchased for Rs.2,000 (Who gives you two wheeler for two thousand rupees!) Just to explain the point.

Basic thing you have to catch hold of strongly is “LEFT SIDE MEANS DEBIT-DR” and “RIGHT SIDE MEANS CREDIT-CR”.

I HAVE SHOWN ‘T’s for both debit and credit accounts for your better understanding. If the cash goes down, you have to enter it in the right side of the T of cash account since asset account increases only with debit and goes down with credit.

The initial investment of Rs.10,000 increases the cash account by Rs.10,000 and hence the entry is made in the left side of the cash account and also it increases the Owner’s Equity account by Rs.10,000 and hence entered in the right side of the owner’s equity account. Liabilities account increases with credit.

© Copyright 2022, Managementguru.net. All Rights Reserved.