Posted in Accounting, Financial Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

Ratio Analysis – An Introduction

What is Ratio?

The relationship between two variables expressed mathematically is called a ratio.

It refers to the systematic use of ratios to interpret the financial statements in terms of operating performance and financial position of a firm.

Some important definitions:

- “The relation of one amount, a to another b, expressed as the ratio of a to b”– Kohler

- “Ratio is the relationship or proportion that one amount bears to another, the first number being the numerator and the later denominator” – H.G.Guthmann

Significance of ratio analysis:

- It consolidates and simplifies the accounting information or data

- It is a clear indicator of an organisation’s efficiency

- It helps in the evaluation of a firm’s performance by comparing the past and present ratio

- It aids the management in formulating poilicies, preparing budgets etc.,

- It points out the liquidity position thereby assisting in assessing the short-term obligations and long-term solvency

- It facilitates inter-firm and intra-firm comparison, the former to understand the position of firm in the market and latter to gauge the performance of different divisions of the firm.

- Since ratios have the power to speak, they are considered as effective means of communication

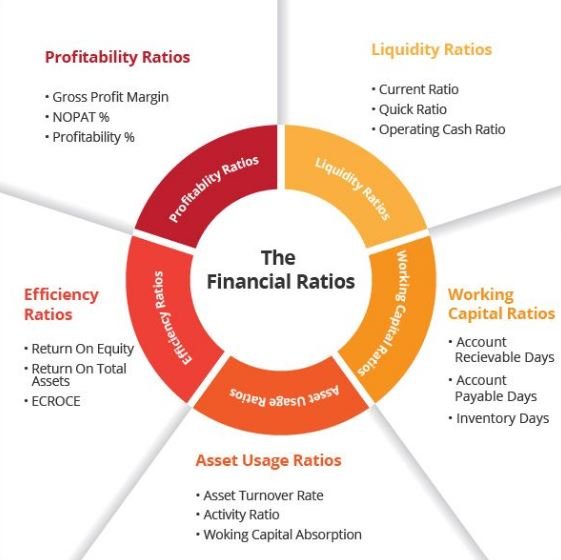

A broad classification of ratios:

Pic Courtesy : Financial Ratios

CLASSIFICATION BY FUNCTION

1. Solvency

Short-term Long-term

Current ratio Proprietory ratio

Liquid ratio Debt-Equity ratio

2. Profitability

- Gross profit ratio

- Net profit ratio

- Operating profit ratio

- Return on Investment ratio

3. Activity ratio

- Fixed assets turnover ratio

- Debitors turnover ratio

- Creditors turnover ratio

- Stock turnover ratio

4. Leverage

- Financial leverage ratio

- Operating leverage ratio

- Capital gearing ratio

CLASSIFICATION BY STATEMENTS

1. Balance sheet ratios

- Current ratio

- Liquid ratio

- Proprietory ratio

- Debt-Equity ratio

- Capital Gearing ratio

2. Profit and Loss Account ratios or Profitability ratios

- Gross profit ratio

- Net profit ratio

- Operating profit ratio

- Return on Investment ratio

3. Inter-Statement ratios or Turn-over ratios

- Fixed assets turnover ratio

- Debitors turnover ratio

- Creditors turnover ratio

- Stock turnover ratio