Posted by Managementguru in Financial Management, Principles of Management

on Feb 28th, 2014 | 0 comments

What forms the Basis for your Investment Decisions? Profit seeking is the ultimate aim of corporate management and the finance manager acts as the anchor point of the management structure. He has to provide specific inputs into the decision-making process, with respect to profitability. Corporate Investment Decisions Cost control What are the Cost Centres? It is the finance manager’s responsibility to have an eagle’s eye on rising costs by continuously monitoring the cost centers of his organization. Production department where there is always a need for additional resources or inflow of funds, should be his first target of contol. Costs are incurred by each and every department of an organization, namely, the production, marketing, personnel and of course finance and accounting. It is a difficult task to control the rising costs. That is the reason why, big corporate companies go for annual budget formulation at the start of the year and reformulates the finance plan by comparing actual with the projected figures. This kind of evaluation helps the firm to fix responsibilities for various centers of operation. Resource Allocation A finance manager is the first person to recognize rising costs for supplies or production, and he can make immediate recommendations to the management to bring back costs under control. While cost control talks about allocating resources to different responsibility centers in the desired proportion, cost reduction focuses on conserving the resources. Cost reduction can be achieved through modifying product and process designs, cutting down throughput time, doubling labor productivity, mass customization, standardistion etc., Pricing Price Fixation It is always a joint venture between marketing and finance departments when it comes to price fixation of products, product lines and services. Pricing decisions are important in that, they affect market demand and the company’s competitive stand in the market. Pricing strategies have to be evolved in the wake of existing competitor strategies and market preference. The demand forecast is the prerequisite factor of the production process and in-depth market analysis and understanding is inevitable on the part of the executives. Future Levels of Profit The finance manager is also responsible for charting out the future levels of profit, based on the relevant data available. He has to consider the current costs, likely increase in costs and likely changes in the ability of the firm to sell its products at the established selling prices. So, it becomes clear that, such market evaluation cannot be periodical, as the market is highly dynamic and has to be done in a day-to-day basis. Before a firm commences a project, its discounted future fund flow and expected profits must be ascertained which will serve as a basis for comparison. Risk versus Return: Investment decisions always are risky as the gestation period of invested funds is very long and not to return immediately. Further, the firm has to calculate the time period in which its initial investment can be recovered and the feasibility of the rate of return on its investment. Fund Management The finance manager is engaged in activities like, mobilization of funds, deployment of funds, and control over the use of funds and also he is to evaluate the risk return trade-off. Profit maximization is the fundamental objective of any organization and the finance manager plays a key role in restructuring the financial philosophy of a firm to take it to greater...

Posted by Managementguru in Accounting

on Feb 21st, 2014 | 0 comments

Functions of Accounting: a. Recording: Accounting records business transactions in terms of money. It is essentially concerned with ensuring that all business transactions of financial nature are properly recorded. Recording is done in journal, which is further subdivided into subsidiary books from the point of view of convenience. b. Classifying: Accounting also facilitates classification of all business transactions recorded in journal. Items of similar nature are classified under appropriate heads. The work of classification is done in a book called the ledger. c. Summarizing: Accounting summarizes the classified information. It is done in a manner, which is useful to the internal and external users. Internal users interested in these informations are the persons who manage the business. External users of information are the investors, creditors, tax authorities, labor unions, trade associations, shareholders, etc. d. Interpreting: It implies analyzing and interpreting the financial data embodied in final accounts. Interpretation of the data helps the management, outsiders and shareholders in decision making. Limitations of Accounting: Accounting information is expressed in terms of money. Non monetary events or transactions, however important, are completely omitted. Fixed assets are recorded in the accounting records at the original cost, that is, the actual amount spent on them plus all incidental charges. In this way the effect of inflation (or deflation) is not taken into consideration. The direct result of this practice is that balance sheet does not represent the true financial position of the business. Accounting information is sometimes based on estimates; estimates are often inaccurate. Accounting information cannot be used as the only test of managerial performance on the basis of more profits. Profit for a period of one year can readily be manipulated by omitting such costs as advertisement, research and development, depreciation and so on. Accounting information is not neutral or unbiased. Accountants calculate income as excess of revenues over expenses. But they consider only selected revenues and expenses. They do not, for example, include, cost of such items as water or air pollution, employee’s injuries, etc. Accounting Made Easy Accounting like any other discipline has to follow certain principles, which in certain cases are contradictory. For example current assets (e.g., stock of goods) are valued on the basis of cost or market price whichever is less following the principle of conservatism. Accordingly the current assets may be valued on cost basis in some year and at market price in another year. In this manner, the rule of consistency is not followed...

Posted by Managementguru in Accounting, Financial Accounting, Financial Management

on Feb 13th, 2014 | 0 comments

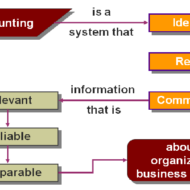

The purpose of accounting is to provide the information that is needed for sound economic decision making. The main purpose of financial accounting is to prepare financial reports that provide information about a firm’s performance to external parties such as investors, creditors, and tax authorities.

Posted by Admin in Accounting, Management Accounting

on Jan 29th, 2014 | 0 comments

Management accounting combines accounting, finance and management with the leading edge techniques needed to drive successful businesses. The process of preparing management reports and accounts that provide accurate and timely financial and statistical information required by managers to make day-to-day and short-term decisions