Posted in Accounting, Financial Accounting, Management Accounting

on Jun 25th, 2014 | 0 comments

Ledger is a register with pages numbered consecutively. Each account is allotted one or more pages in the Ledger.

If one page is completed, the account will be continued in the next page. An index of various accounts opened in the Ledger is given at the beginning of the Ledger for the purpose of easy reference.

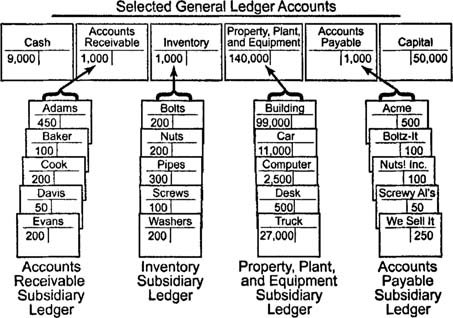

A general ledger is a complete record of financial transactions that holds account information needed to prepare financial statements, and includes accounts for assets, liabilities, owners’ equity, revenues and expenses.

Ledger Account

What is meant by Posting?

Transactions recorded in the Journal and Subsidiary journal are transferred to the concerned accounts in the Ledger in a summarized and classified form. This process is called posting.

“Interesting Statistics on Accounting

- The first book on double-entry accounting was written in 1494 by Italian mathematician and Franciscan friar Luca Bartolomeo de Pacioli.

- Although double-entry bookkeeping had been around for centuries, Pacioli’s 27-page treatise on the subject has earned him the title “The Father of Modern Accounting.

- Accounting plays a major role in law enforcement. The FBI counts more than 1,400 accountants among its special agents.

- The state of New York gave its first certified public accountant (CPA) exam in 1896.

Rules for posting:

- Separate account should be opened in the Ledger for posting transactions relating to separate persons, assets, expenses or losses as shown in the journal.

- The account concerned which has been debited in the journal should also be debited in the Ledger. However, a reference must be made of the other account which is to be credited in the journal. In other words, in the account to be debited, the name of the other account to be credited is entered in the debit side for giving a meaning to this posting. The debit posting is prefixed by the word ‘To’.

- Similarly, the account concerned which has been credited in the journal has to be credited in the Ledger, but a reference should be made to the other account which has been debited in the journal. This posting is prefixed by the word ‘By’.

Advantages of keeping a Ledger:

- Ledger provides information regarding all transactions of a particular account whether it is personal a/c, Real a/c or nominal a/c.

- The final effect, of a series of transactions of a certain customer or a certain property or a certain expense is known at a glance.

- Ledger provides immediately the totality of certain dealings. E.g., total purchases, Total sales, total expenditure, on a specified head.

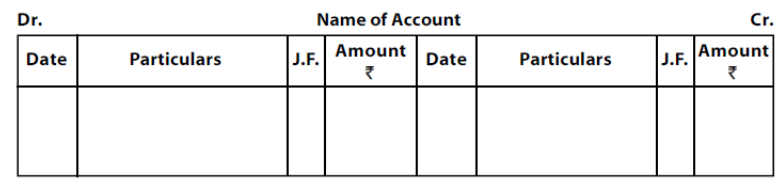

What is a Ledger account? Give a Proforma of a Ledger account.

A Ledger account is nothing but a summary statement of all transactions relating to a person, asset, expense or income, which have taken place during a given period of time showing their net effect.

Proforma of a Ledger account:

What are the methods of balancing the Ledger account?

At the end of the each month or year or any specific day it is essential to determine the balance in an account. To do that, add the totals of both sides (Debit and credit sides) and find out the difference in both the sides.

The difference in both the sides is ‘Balance’. If the Debit is greater than the credit side, it is a Debit balance or vice-versa.

There are two methods:

- The bigger total is taken first and is written on both sides of the account. On the smaller side, the balance is Witten above the total next to the last entry on that side. This method is more commonly used.

- In another method, the totals are written on both sides, one side showing smaller amount and the other showing bigger amount. The difference is written on the smaller side below the smaller total. After doing so, grand totaling is made on both sides. Obviously they will be equal. This method is used only in certain concerns like Electricity companies.