(i) Recording of business transactions in the books of prime entry,

(ii) Posting into respective ledger accounts,

(iii) Striking balance, and

(iv) Preparing the performance statement (profit and loss statement) and position statement (balance sheet).

Financial Accounting is concerned with the collection, recording, classification and presentation of financial data to serve the purposes of the management, shareholders and stakeholders, such as, creditors, bankers, Government, etc.

Let’s have a small recap on the objectives and classification of accounting in general.

Various classifications of Accounting

Financial: The main purpose is to record the business transactions in the books of accounts enabling businessmen to know the results. In general, the term accounting refers to financial accounting only.

Cost Accounting: ICMA London refers to cost accounting as “an application of accounting and costing principles, methods and techniques in the ascertainment of cost and analysis of savings as compared with past or with established standards.

Management Accounting: Both financial and cost accounting methods and results contribute to management accounting where the data is interpreted mainly for arriving at optimal managerial decisions.

Two methods of Accounting

Cash System

In this method, entries are made only when cash is received or paid and no entry being recorded when there is a payment or receipt due.

Mercantile System

Here, entries are made on the basis of amount having become due for payment or receipt.

SCORE KEEPING – The score keeping function is one of the primary purposes of accounting information. It basically deals with the financial health of the enterprise.

In other words, it answers: How are we doing? Good, bad, or indifferent? Though it appears to be a simple question, a moment’s reflection will show that it is not that simple.

It involves answering questions such as: What is doing good? What is doing bad? Is profit earned good? If so, how much? Is it that profit alone is not sufficient?

ATTENTION DIRECTING – Attention-directing is nothing but the process of giving a signal to the user of accounting information about the need to take a decision.

As such the accounting information supplied arouses the user’s attention to take a decision. For example, a report from an accountant comparing the actual performance data against budget data is a score- keeping record.

In the hands of a decision-maker it is attention-directing information. This would enable him to immediately focus his attention on the deviations or variances from the budgets or the plans.

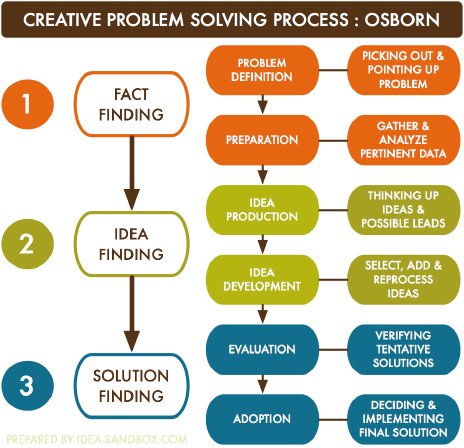

PROBLEM SOLVING – The problem-solving function of accounting information involves provision of such information which enables the manager to find solutions to the problems.

Pic Courtesy : Creative Problem-Solving Process

There are many problems which accounting information could highlight and provide for their possible solutions, such as make or buy decision with respect to component, parts or products, continue or drop decisions with respect to product lines leasing or acquisition decisions with respect to assets etc.

Profit and cash balance distinguished how do we evaluate the results of a firm? The answers could be many depending on what your interests are.

But there is no difference of opinion regarding two important aspects. 1. What is the worth of the business? 2. How much does it earn? The results of-these two inquiries usually become the basis for several decision of the management and their action plans.

The initiatives the management takes in connection with improving the profitability of the enterprise and its worth will, in a large measure, be a reflection of managerial effectiveness.

SUMMARY – Accounting, in its score card role, accumulates data and enables interested persons, both internal and external, to understand and take stock of the organization’s performance.

In its attention-directing role accounting information, by reporting and analyzing the data focuses a manager’s attention on operational deficiencies, weaknesses, threats -and opportunities.

In this role accounting complements day to day operational planning and control activities. In its problem-solving role, accounting enables quantification of the different alternative solutions, their relative merits and demerits.

Since shareholders have invested in the company so they are interested in the financial statements.

Creditors:

Creditors may be short-term or long-term. The main apprehension of the creditors is focused on the credit worthiness of the firm and its ability to meet its financial obligations. Say, for example- the liquidity of the firm, its profitability and financial soundness.

Management:

Management expects accounting information for planning, organizing, and control purposes. The emphasis on efficient & effective management of organizations has considerably extended the demand for accounting information.

Employees:

The significance of agreeable industrial relations between management & employees cannot be over-looked. The employees have a stake in the outcomes of several managerial decisions.

Greater emphasis on industrial democracy through employee participation in management decisions has important implication for the supply information to employees. Matters like settlement of wages, bonus, & profit sharing rest on adequate disclosure of relevant facts.

Government:

Government uses financial information for compiling statistics concerning calculation of profitability, taxes, computation of national income, and determination of the industrial growth.

Stock Exchanges:

Several stock exchanges also require accounting information for listing of securities.

Consumers & Others:

Consumer organizations, media, welfare organizations and public at large are also interested in condensed accounting information in order to appraise the efficiency and social role of the enterprises in different sectors of the economy.

© Copyright 2022, Managementguru.net. All Rights Reserved.