It means reduction in the value of a fixed asset used in the business due to #wear and tear and effluxion of time.

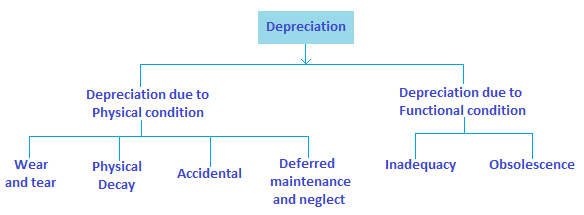

i. Wear and tear: Caused mainly due to constant use, erosion, rust etc.

ii. Efflux of time: Mere passage of time will cause a fall in the value of an asset, even if it is not used.

iii. Obsolescence: A new invention or change in fashion or a permanent change in demand may render the asset useless.

iv. Depletion: When raw materials or natural resources like mines, quarries and oil wells are extracted continuously, they deplete.

v. Accident: An asset may reduce in value because of meeting with an accident, like fire accidents.

vi. Fall in the market price.

Watch this video on What Is Depreciation – How It Affects Profit And Cash Flow

According to International Accounting Standard Committee (IASC) “Depreciation is the allocation of the depreciable amount of an asset over its estimated useful life.

Depreciation for the accounting period is charged to income either directly or indirectly.”

The need for depreciation arises because of the following reasons:

Factors to be considered while determining the amount of depreciation:

I. The total cost of the asset including all freight, insurance and installation charges

II. The estimated residual or scrap value at the end of its life

III. Estimated number of years of its usefulness

It is concerned with charging the cost of fixed assets to operations. But the term depletion refers to the cost allocation for natural resources, whereas the term amortization relates cost allocation for intangible assets.

© Copyright 2022, Managementguru.net. All Rights Reserved.