Currently Browsing: Financial Management

Posted by Managementguru in Business Management, Entrepreneurship, Financial Management, How To, Startups

on Oct 28th, 2020 | 0 comments

As a first-time entrepreneur, learning the ins and outs of your market, the business, and determining an effective strategy are all important keys to success. One aspect that is often overlooked by many first-time entrepreneurs, however, is a successful wealth management strategy. In order to remain competitive in the market that you are entering, you need to be financially ready. The preparations a business makes in its financial management strategy in the early stages can often be the reason why some businesses succeed while others fail. Proper wealth management is crucial to your success, so take the time now to become familiar with the concept and how you can apply best practices to your own business venture. Get to Know Your Financials The first step in proper wealth management is becoming familiar and comfortable with your current personal and business financials. Working with a financial adviser can be an important strategic step to take to make sure that you have everything in place in order to effectively start and operate a business. They can also work with you to understand your credit score, future wealth projections, and strategies for overcoming unforeseen expenses. When entrepreneurs go into business blindly without preparation, it can be difficult to overcome the debt that this forces individuals to incur. Setting your sights on the future and preparing for them now will help you tackle emergencies and challenges as you are faced with them. Read On: Brave New Life: How to Start an Agency After a Freelancing Career A resourceful article from TimeClockWizard that operates an extremely popular employee time management tool for small businesses. Be Agile With Your Costs A successful entrepreneur should possess the ability to remain agile in any situation. Adapting to changes in the market and being flexible with consumer demands are favorable traits that will help increase profits in the long run. In the presence of a situation, however, a business owner may be required to come up with cash quickly. Finding solutions to meet the demands of the market and your customers often requires strategic thought processes around ways to better manage your current costs. Read On: How To Start A Business In The UK? An exceptionally valuable guide, which provides secrets from industry experts to starting a successful business in the UK . Because costs are often unavoidable and may come during the most unexpected of times, it’s important that during these times you utilize the resources around you. Making the right decision for your business could mean taking out a loan, seeking out an investor, or restructuring personal expenditures such as refinancing your home. Whichever decision you decide is right for you, know that there are many options to help you access the cash you need. For your commercial insurance needs, Krywolt Insurance has the right answers. Set Goals for Your Business Every entrepreneur has their own reasons for choosing to start a business. Likely reflective of their desire to do more with their personal passions and talents, becoming an entrepreneur is a goal that many hope to achieve. Once you have successfully completed your goal of starting a business, it’s important to set goals for your business as well. Setting egocentric goals of “becoming a millionaire” or “becoming the best at …” won’t help drive your business forward. Many entrepreneurs fall into the trap of thinking they will become rich or successful simply by starting their own venture. This can cause any business to fail as the most valuable stakeholders in a business venture often get forgotten. Your investors, employees, and customers are all important to helping your business achieve its goals. Working together with a cohesive...

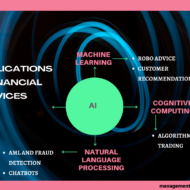

Posted by Managementguru in Artificial Intelligence, Financial Management, Technology

on Sep 8th, 2020 | 0 comments

Artificial Intelligence (AI) is transforming industries across the board, and financial companies and institutions are moving fast to keep pace. AI is changing the way we apply for loans, file insurance claims, invest our money, and interact with our banks. Here are some of the most prominent AI trends that are making inroads in the finance industry. Fraud Detection and Management As e-commerce is rising in popularity, so is online fraud. To prevent frauds, many e-commerce platforms and card issuers have been forced to decline transactions too aggressively. According to a study by Javelin Strategy, retailers lost almost $118 billion in 2015 due to false declines. Moreover, more than a third of cardholders abandoned their card because it was falsely declined. To detect fraud and prevent loss of revenue, many financial institutions have turned to AI. Machine learning algorithms can reduce false declines and improve the accuracy of real-time approvals because they can identify fraudulent activities that would go unnoticed by humans. Recently, Mastercard has launched its own AI-based fraud prevention system. Mastercard’s technology gleans patterns from the historical spending habits of shoppers. It uses this data to set a behavior baseline that allows it to score and compare new transactions. It is not limited to predetermined rules. Traditional fraud detection systems, on the other hand, use a one-size-fits-all approach when evaluating transactions. Since Mastercard processes countless interactions each year, they have plenty of quality data they can use to hone and train its AI fraud prevention system. Thanks to machine learning, AI fraud detection systems learn on their own and improve themselves over time. AI systems can also automate AML (Anti-Money Laundering) and KYC (Know Your Customer) compliance. Virtual Assistants and Chatbots Thanks to machine learning and natural language processing (NLP), chatbots and virtual assistants can deliver human-like interactions. There are more and more virtual assistants that are designed for various niches within the finance industry. Banks and other institutions use virtual assistants and chatbots to offer personalized conversational experiences to their clients. Unlike human agents, virtual assistants can juggle multiple accounts at once, and they are always available. They allow customers to get assistance outside of office hours. Banks, brokerage firms, and insurance companies can use chatbots to reduce the workload of their call centers. By offerings comprehensive self-help solutions, clients can successfully apply for loans, get personalized financial tips, or file claims much faster. For instance, the AI Insurance Claims Assistant can help and re-engage with customers throughout the complete claims process. It can gather the required information for processing and update the customers on the status of their claims. They also have digital workers that can automate the onboarding journey, help customers figure out their coverage needs, update their information, or make policy adjustments. Banking bots, on the other hand, can help customers optimize their financial plan by intelligently tracking their income, spending habits, and essential recurring expenses. They can also help customers open an account and remind them to pay their bills. Risk Assessments As mentioned, one of the strongest features of AI is its ability to learn from past data. Since records and bookkeeping are an essential part of financial services, AI and finance go hand in hand. Credit cards are a perfect example. To determine if someone is eligible for a credit card, card issuers use credit score. But, business-wise, it doesn’t always make sense to group customers into “haves” and “have-nots.” Instead, financial institutions can use each customer’s data, such as the number of credit cards they have, the number of loans currently active, and information on loan repayment habits, to customize the interest rate on the card they have issued...

Posted by Managementguru in Business Management, Decision Making, Entrepreneurship, Financial Management, How To

on Jun 19th, 2020 | 0 comments

Starting a Business: You’ve probably read countless articles about it and believe you’re finally ready to take that big step. A word of caution though: once you step into the entrepreneurial waters, you’ll quickly realize that nothing has really prepared you for it. There’s so much more to it than just a good idea. It takes a lot of research and planning to prepare for starting a business. In this article, we help you save that precious time by bringing you 4 things you need to know before starting a business. Understand the Laws and Regulations One of the most important things when starting a business is to familiarize yourself with the laws and regulations that affect you. What kind of business permit or license will you have to obtain? What are the legal requirements for starting your business? How much will you need to pay in taxes? Compliance with the law is essential because you don’t want a technicality holding you back once you embark on this journey. There is a lot to consider from filing tax returns and paying your staff to protecting your business with insurance. If you can’t figure out all of these things on your own, seek help from a reputable accounting firm. A professional can guide you through these laws and regulations and help you figure out if you’re ready to start a business. Additionally, a skilled accountant will be a great ally later on in helping you manage your finances and not over-paying on taxes, etc. Experts at Bankrate have created a resourceful guide that explores seven ways to manage financial stress. It includes tips such as prioritizing what you can control, earning extra money, paying essential bills, and more.Here is the link for the guide : 7 ways to manage financial stress during trying times Is There a Demand for Your Product? Before you spend all your money on developing a product, have you researched the market? Is there a demand for such a product or service? What about the competitors? This might be hard to hear but there is a chance your product isn’t so great or needed so your first step should be to find out whether there is a market for it. Countless new ideas and products are introduced every week, month, year. But how many businesses actually succeed in surviving the first few years? About 80% of businesses survive the first year while only half of all businesses make it to the fifth year. You’ll need all the information you can gather so that you can make small adjustments to your product/service accordingly. Thorough market research will provide answers to the above-mentioned questions and give you an insight into whether it’s worth spending more time on your idea or not. Research your competition carefully. But don’t get discouraged if you discover that there are many other businesses with similar ideas. This doesn’t mean that you can’t be in the same business too. If the market is thriving, surely there is a place for one more great product. Planning Your Business A comprehensive guide from MyMove – for parents to help provide their kids with a baseline of financial literacy so they have the information they need to make smart educated decisions. You can check it out below:Financial Literacy: Teaching Kids How To Buy A Home Don’t Spend More Than You Need When starting a new business, most people give up a lot to finance the idea. Many get into debt, spend too much too soon and showcasing poor money management skills. This matter also requires good research. You need to know what to spend on and what can...

Posted by Managementguru in Business Management, How To, How to make money online, Marketing, Sales, SEO, Strategy

on May 9th, 2020 | 0 comments

The success of your eCommerce website is usually pegged on whether customers can buy the products they need quickly and efficiently. If there are any hiccups in this process, customers are likely to leave and you will lose a sale. To ensure this does not happen, it pays to improve your customer experience. This has the add-on effect of increasing sales and profits. Below, we will look at a few things you can do to improve your e-commerce website. Use Clear, Legible Fonts Even though most e-commerce websites are not text-heavy, people still need to read descriptions, directions, and texts like on your privacy page. Improvements in this area come from selecting the right font. You want a font that is not too thin or bold, one that is not too fancy, and one that is easy on the eyes if you have a lot of text on your website. Also, ensure that the font is at least 16 pixels in size as this has been showing to be the best baseline font size. Make Your Website Responsive Mobile visitors have overtaken desktop visitors on most websites, and this might be true for your e-commerce website. If your website is not responsive, these users will have a hard time navigating the website. A simple test is to visit your website on your phone and see how easy it is to navigate. If it is not for you, it might also not be for your visitors. There are also lots of online tools that can help you know if your website is responsive and easy for mobile users to navigate. If it is not, use the reports generated by these tools to make the necessary changes. Make the Checkout Process Easy No one wants to jump through hoops when they are trying to buy something from your website. If you want customers to have a good experience when checking out, make the process as simple as possible. Collect just the amount of data you need to complete the sale and no more as people hate filling forms. You should also ask your web developer to make sure any errors that occur as the user fills the checkout forms are displayed immediately and not after a reload. Diversify Your Payment Options Everyone has a preferred way of paying. Some like paying using their credit cards, some their bank accounts, and others using platforms like Stripe and PayPal. To accommodate everyone, try to use as many payment options as possible. Users who might want to pay using a method you do not support will usually leave without making a purchase. If you do not want to add all these options, at least accept credit cards and PayPal. Reduce Banners and Popups Banners and popups are a big inconvenience for a lot of people. This is because they slow customers down when a business is running a flash sale or other promotion and make them feel like they are losing out on the deals they came for. Although these banners can help alert users to promotions and sales you are running, using too many of them can ruin customer experience. Try to use as few of them as possible. Business owners who want to increase sales on their e-commerce websites should start by improving the customer experience on their website. If you make things as simple as possible for customers, they are much more likely to purchase from you and even become repeat...

Posted by Managementguru in Business Management, Entrepreneurship, Financial Management, Startups

on Apr 12th, 2020 | 0 comments

Money is essential to run a successful company. Often the capital invested may not be adequate for the company. A corporate loan is the most reliable possible option for a company owner in such situations. We define business loans as the money obtained for business investment. Getting a business loan is a simple process. While it is collectible from all institutions, an owner of the business must apply with a specific provider to obtain a business loan. Loan seekers must also follow the minimum requirements of this particular lender when submitting the form. The loan documents will only be accepted once the application gets organized and completed. A business loan could be a significant income source; however, the variety of loan options to small business people can be challenging to manage. The forms to which small businesses are entitled are SBA loans, traditional bank loans, and digital cash flow loans. Happily, to keep things simple for loan applicants, there has been a range of reasons to check to ensure that the applicant gets the appropriate type of loan. A business loan is hard to obtain with poor credit history. However, it is not impossible to apply for a small business loan with bad credit as many substitute creditors provide financing options for people with poor credit background. In the following write-up, we will give you things to remember when applying for a business loan. DIFFERENT THINGS TO KEEP IN MIND WHILE APPLYING FOR A BUSINESS LOAN The concept of a business loan is appealing; it requires more than you could imagine at first. It is quite crucial to understand your need for cash so that it may appear vividly in the application of a loan. Furthermore, knowing where to spend enhances the capability of how efficiently you spend the acquired amount. TIME OF APPLICATION AND APPROVAL PROCESS Many businesses regard SBA loans as the right choice. Clients who have prior experience of using this loan are entirely satisfied with the terms and conditions implied, i.e., the seamless application process. Having said that, while trying to apply for a business loan, we must understand what is offered out of the procedure. Once you apply, lenders will still need to handle it in its entirety. At least one month will be consumed to prepare for the paperwork. This is the fundamental step if you are thinking about your company’s future. For the moment, you might be very eager to get the money and invest in your estimated plan. But, rushing can cost you your precious opportunity. Calm and composed behavior allows you to see those possible mistakes which you may ignore unintentionally. Read On: The costs of opening a restaurantBankrate’s recent resource gives advice on the cost of opening a restaurant, ways to finance it and valuable guidance on the necessary permits and licenses as well as other start-up expenses. VALID AMOUNT TO APPLY It is necessary to be optimistic about the amount of cash your company requires if your request is to succeed. Do not expect far too much, and often do not ignore the taxes and fees. In other words, when you want a loan to buy new facilities for your company, see precisely the actual cost of the equipment, sales tax implied, delivery charges, storage, installation, or any necessary permits for its use. Lending institutions choose to cooperate with practical, accountable borrowers who have accurately calculated the amount needed to attain their objectives and expand their business. CONSIDER THE EARLY PAYMENT CHARGES Concerning the subject of expense, advance payments may be a risk for a careless borrower. It may seem like a tempting idea for paying the loan back before time. But there...