Posted by Managementguru in Accounting, Financial Accounting

on Feb 21st, 2014 | 0 comments

Characteristics and Objectives of Accounting What is Accounting: According to American Institute of Certified Public Accountants (AICPA), “Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money transactions and events which are, in part at least, of a financial character and interpreting the results thereof.” American Accounting Association (AAA) has defined accounting as “the process of identifying, measuring and communicating economic information to permit informed judgements and decisions by users of the information.” Characteristics of Accounting: i. Accounting is the art of recording and classifying different business transactions. ii. The business transactions may be completely or partially of financial nature. iii. Generally the business transactions are described in monetary terms. iv. In accounting process, the business transactions are summarized and analyzed so as to arrive at a meaningful interpretation. v. The analysis and interpretations thus obtained are communicated to those who are responsible to take certain decisions to determine the future course of business. The Small Biz Doers’ Guide to Small Biz Accounting Objectives of accounting: a. To record the business transactions in a systematic manner. b. To determine the gross profit and net profit earned by a firm during a specific period. c. To know the financial position of a firm at the close of the financial year by way of preparing the balance sheet d. To facilitate management control. e. To assess the taxable income and the sales tax liability. f. To provide requisite information to different parties, i.e., owners, creditors, employees, management, Government, investors, financial institutions, banks etc. ...

Posted by Managementguru in Business Management, Financial Management, Principles of Management

on Feb 21st, 2014 | 0 comments

Every business organisation’s aim is to make profit and more profit. Does it end there? What should be the real motive behind running an organization? Profit maximization alone does not help the organization to firmly plant its feet in the business environment, as the success of an organization in the long run is decided by many critical factors like, market share, value of the company shares, market stand, image etc. So, shall we say, let wealth maximization be the goal of any organization, which focuses on increasing the “earnings per share” of the share holders. What is Profit Maximization? Profit maximization does not take into consideration, the interest of share holders or stake holders, who ought to be the ultimate beneficiaries. Concentrating on short term profits confines a firm and limits its scope and growth whereas; value creation is something that the management should aim for, as it helps to increase the “net worth” of a company. Mere price versus output calculations make firms to operate in a profitable manner, but it should never be the only objective of a firm, as it has the moral and social responsibility to patronize its shareholders by increasing the net worth of the company. Underlying Logic While maximizing profit, a firm either produces maximum output for a given amount of input, or uses minimum input for producing a given output. Thus the underlying logic for profit maximization is efficiency. Under perfect competitive market conditions, profit serves as a perfect measure for the performance of a firm. If profit is the motive of a firm, it fails to consider the time value of money which is an important criterion that decides the success of a firm, and also it values benefits received today and after a period as the same. Moreover the uncertainty factor is there to be considered too. Firms always prefer to have smaller but surer profits rather than larger benefits but less certain. Impact of Taxes When we talk about profits, the next indispensable factor will be the taxes that demand a portion of your profit. Maximizing profits after the payment of taxes facilitates the firm to increase the net profit ratio to serve the best interests of the owners. But, this also fails to maximize the economic welfare of the owners, as it does not take into account, the timing and uncertainty of the benefits. Wealth maximization is the ideal alternative that is consistent with the survival goal and also with the personal objectives of managers such as recognition, power, status and personal wealth. The Right Balance between Risk and Return Mangers while deciding on investment options, seek to achieve a right balance between risk and return. If the firm borrows heavily to finance its operations, care should be taken to ensure that, the rate of return on investment should be sufficient enough to support the payment of interests on borrowings and also to repay the principal. If the firm is not able to “service the debt” there is a danger of the firm becoming bankrupt or insolvent. The firm’s investment and financing decisions are unavoidable and continuous. In order to make rational decisions, the firm must have a goal, which is nothing but the “shareholder’s wealth maximization” which is theoretically logical and operationally...

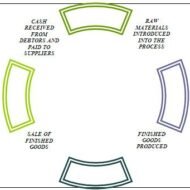

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 21st, 2014 | 0 comments

Applications of fund Purchase of fixed assets – leads to outflow of funds, but at the same time adding assets to your organization always improves the financial position of your firm. You can also use these assets as “collaterals” for availing loans in banks. Redemption of preference shares – you have to apportion your operating profit in order to satisfy the preference share holders with interest. This will give you a clear idea of the earnings available for the equity share holders. Fund that is lost during business operations – Due to wrong investments and credit policies, sometimes your funds get sticky and recovery becomes next to impossible. Repayment of loans – although the fund goes out, you free yourself from further interest burden and reduce your credit limit with the bank. Remember,it is better to repay the loans from your profit. Redemption of debentures – It is easy to raise money from debentures, because people are rest assured of their payment at a fixed date. But the cost of servicing the debt might sometime exceed the concessional advantages on raising such securities. https://gumroad.com/l/wqbu A systematic study of fund flow facilitates in ascertaining the soundness of your firm’s financial condition and it also helps to formulate the right kind of dividend policies. Net working capital is the life line of a firm’s day-to-day operations and we can surely say that a company is prosperous if it has a surplus of net working capital at any given point of time. The financial manager of your company should have the vision to predict changes in the stock market and play the cards accordingly. It needs an in-depth understanding and analysis of the market conditions with a wider...

Posted by Managementguru in Human Resource, Organisational behaviour, Principles of Management, Training & Development

on Feb 20th, 2014 | 0 comments

Role of Training Some Definitions of Training: According to Flippo, “Training is the act of increasing the knowledge and skills of an employee for doing a particular job”. Training can also be defined as as “any planned or structured activity or approach designed to help an individual or a group of people to learn as to do things differently or to do different things leading to more effective performance and results”. Role of Training: Training is the best way to reach the enterprise goals in minimum time period with maximum efficiency. 1. Training unlike experience can reduce the time required to reach maximum efficiency. 2. Cost of training in much less than the cost of adding experience . 3. The results of experience sometimes can be accidental. 4. The expected results are very much assured in a well conceived and well conducted training program. 5. Its purpose is to achieve a change in the behaviour of those trained and to enable them to do their jobs better. 6. Training makes newly appointed employees fully productive in lesser time. Identifying Training Needs: There are three elements of training – purpose, place and time. Training without a purpose is useless because nothing would be achieved out of it. The purpose must be identified carefully and now there are a large number of techniques available for establishing training needs. Having identified the purpose of a training programme, its place must be determined i.e. whether it has to be on the job or off the job. Place would decide the choice of training method and also affect its effectiveness. The next element is the time. Training must be provided at the right time. A late training would provide obsolete knowledge, which would be useless for the employees. 1. Organizational Analysis: – Comprehensive analysis of organizational structure, objectives, culture, processes of decision – making, future objectives and so on. Analysis begins with an understating of short term & long-term goals of the organization. Is there adequate manpower to fulfill organizational objectives? Whether the work-force possess required skill & knowledge? Are the employees willing to learn? 2. Task analysis: Thorough analysis of various components of jobs and how they are performed has to be done. Task analysis would indicate whether tasks have changed over period of time & whether employees have adequate skill in performs their tasks. 3. Man Analysis: The focus is on individual, his skill, abilities, knowledge & attitude. Key Indicators are Meeting Deadlines Quality of performance Work behavior...

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

What is fund ? Cash, total current assets, net current assets and net working capital are also interpreted as fund. So, it is necessary to clearly define the meaning of fund and demarcate its scope and function. To put it precisely, fund is nothing but, net working capital of a firm. The flow of fund occurs when a business transaction takes place that leads to an increase or decrease in the amount of fund. Firms prepare fund flow statement to explain the sources and applications of fund, which also serves as a technical tool to ascertain the financial condition of a business enterprise. Balance Sheet In a business firm, everyday numerous financial transactions take place. These are summarized into a balance sheet that gives an idea about the assets and liabilities at a specific point of time. When two balance sheets of consecutive periods are compared, we come to know about the inflow and outflow of funds and thereby the net working capital available is ascertained. This is step one. Profit and Loss Statement The next step would be to prepare an adjusted profit and loss account to determine fund inflow or fund lost from business operations. Accounts have to be prepared to ascertain hidden information (for all non-current items of assets and liabilities). Finally fund lost or gained from operations is arrived at and presented in a statement form. It is not that, only accountants could understand these operations and adjustments. Any person with logical reasoning and business acumen can understand the nuances of accounting, of course with some guidance. Few points that highlight the ways in which funds flow outside and inside a business enterprise will give you a better idea on the nature of fund flow: Sources of fund: Sale of fixed assets – sale of land, building, machinery, furniture etc. But you have to take into consideration a factor called “depreciation“. It is nothing but the wear and tear of the assets due to continuous usage, reduction in market value over a period of time, obsolescence, accidents etc. Remember, land is a non-depreciable asset in developing countries like India, whereas it may not be so in certain developed countries where the real estate values are nose diving. Issue of Equity shares – To raise capital free of interest, many big corporate firms go for equity capital from the general public. But the firms should make it a point to declare dividends if it happens to reap enormous profit to retain their market share. Their main aim should be to protect the interests of the equity share holders who are also the owners. Fund that comes into the firm through business operations – through sale of goods and services. Here the firm has to factorise its cost of production and economy of scale in order to make it cost-effective and fix a feasible profit margin. Borrowing of loans from banks and other financial institutions – Although it is a quick way of raising fund, care should be exercised in that, you should be in a comfortable position to “service the debt“. If not, there lurks the danger of bankruptcy where the firm might become insolvent, if it is unable to repay the interest and principal over a period of time. Issue of debentures – Debentures are also a form of equity but it comes with a price. The firm has to pay a percentage as interest on debentures and repayment period is also fixed in advance. The only solace for the firms would be the tax rebate that can be availed on loans and...