Currently Browsing: Accounting

Posted by Managementguru in Accounting

on Feb 21st, 2014 | 0 comments

Functions of Accounting: a. Recording: Accounting records business transactions in terms of money. It is essentially concerned with ensuring that all business transactions of financial nature are properly recorded. Recording is done in journal, which is further subdivided into subsidiary books from the point of view of convenience. b. Classifying: Accounting also facilitates classification of all business transactions recorded in journal. Items of similar nature are classified under appropriate heads. The work of classification is done in a book called the ledger. c. Summarizing: Accounting summarizes the classified information. It is done in a manner, which is useful to the internal and external users. Internal users interested in these informations are the persons who manage the business. External users of information are the investors, creditors, tax authorities, labor unions, trade associations, shareholders, etc. d. Interpreting: It implies analyzing and interpreting the financial data embodied in final accounts. Interpretation of the data helps the management, outsiders and shareholders in decision making. Limitations of Accounting: Accounting information is expressed in terms of money. Non monetary events or transactions, however important, are completely omitted. Fixed assets are recorded in the accounting records at the original cost, that is, the actual amount spent on them plus all incidental charges. In this way the effect of inflation (or deflation) is not taken into consideration. The direct result of this practice is that balance sheet does not represent the true financial position of the business. Accounting information is sometimes based on estimates; estimates are often inaccurate. Accounting information cannot be used as the only test of managerial performance on the basis of more profits. Profit for a period of one year can readily be manipulated by omitting such costs as advertisement, research and development, depreciation and so on. Accounting information is not neutral or unbiased. Accountants calculate income as excess of revenues over expenses. But they consider only selected revenues and expenses. They do not, for example, include, cost of such items as water or air pollution, employee’s injuries, etc. Accounting Made Easy Accounting like any other discipline has to follow certain principles, which in certain cases are contradictory. For example current assets (e.g., stock of goods) are valued on the basis of cost or market price whichever is less following the principle of conservatism. Accordingly the current assets may be valued on cost basis in some year and at market price in another year. In this manner, the rule of consistency is not followed...

Posted by Managementguru in Accounting, Financial Accounting

on Feb 21st, 2014 | 0 comments

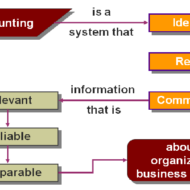

Characteristics and Objectives of Accounting What is Accounting: According to American Institute of Certified Public Accountants (AICPA), “Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money transactions and events which are, in part at least, of a financial character and interpreting the results thereof.” American Accounting Association (AAA) has defined accounting as “the process of identifying, measuring and communicating economic information to permit informed judgements and decisions by users of the information.” Characteristics of Accounting: i. Accounting is the art of recording and classifying different business transactions. ii. The business transactions may be completely or partially of financial nature. iii. Generally the business transactions are described in monetary terms. iv. In accounting process, the business transactions are summarized and analyzed so as to arrive at a meaningful interpretation. v. The analysis and interpretations thus obtained are communicated to those who are responsible to take certain decisions to determine the future course of business. The Small Biz Doers’ Guide to Small Biz Accounting Objectives of accounting: a. To record the business transactions in a systematic manner. b. To determine the gross profit and net profit earned by a firm during a specific period. c. To know the financial position of a firm at the close of the financial year by way of preparing the balance sheet d. To facilitate management control. e. To assess the taxable income and the sales tax liability. f. To provide requisite information to different parties, i.e., owners, creditors, employees, management, Government, investors, financial institutions, banks etc. ...

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 21st, 2014 | 0 comments

Applications of fund Purchase of fixed assets – leads to outflow of funds, but at the same time adding assets to your organization always improves the financial position of your firm. You can also use these assets as “collaterals” for availing loans in banks. Redemption of preference shares – you have to apportion your operating profit in order to satisfy the preference share holders with interest. This will give you a clear idea of the earnings available for the equity share holders. Fund that is lost during business operations – Due to wrong investments and credit policies, sometimes your funds get sticky and recovery becomes next to impossible. Repayment of loans – although the fund goes out, you free yourself from further interest burden and reduce your credit limit with the bank. Remember,it is better to repay the loans from your profit. Redemption of debentures – It is easy to raise money from debentures, because people are rest assured of their payment at a fixed date. But the cost of servicing the debt might sometime exceed the concessional advantages on raising such securities. https://gumroad.com/l/wqbu A systematic study of fund flow facilitates in ascertaining the soundness of your firm’s financial condition and it also helps to formulate the right kind of dividend policies. Net working capital is the life line of a firm’s day-to-day operations and we can surely say that a company is prosperous if it has a surplus of net working capital at any given point of time. The financial manager of your company should have the vision to predict changes in the stock market and play the cards accordingly. It needs an in-depth understanding and analysis of the market conditions with a wider...

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

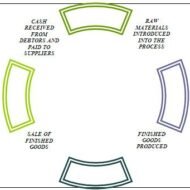

What is fund ? Cash, total current assets, net current assets and net working capital are also interpreted as fund. So, it is necessary to clearly define the meaning of fund and demarcate its scope and function. To put it precisely, fund is nothing but, net working capital of a firm. The flow of fund occurs when a business transaction takes place that leads to an increase or decrease in the amount of fund. Firms prepare fund flow statement to explain the sources and applications of fund, which also serves as a technical tool to ascertain the financial condition of a business enterprise. Balance Sheet In a business firm, everyday numerous financial transactions take place. These are summarized into a balance sheet that gives an idea about the assets and liabilities at a specific point of time. When two balance sheets of consecutive periods are compared, we come to know about the inflow and outflow of funds and thereby the net working capital available is ascertained. This is step one. Profit and Loss Statement The next step would be to prepare an adjusted profit and loss account to determine fund inflow or fund lost from business operations. Accounts have to be prepared to ascertain hidden information (for all non-current items of assets and liabilities). Finally fund lost or gained from operations is arrived at and presented in a statement form. It is not that, only accountants could understand these operations and adjustments. Any person with logical reasoning and business acumen can understand the nuances of accounting, of course with some guidance. Few points that highlight the ways in which funds flow outside and inside a business enterprise will give you a better idea on the nature of fund flow: Sources of fund: Sale of fixed assets – sale of land, building, machinery, furniture etc. But you have to take into consideration a factor called “depreciation“. It is nothing but the wear and tear of the assets due to continuous usage, reduction in market value over a period of time, obsolescence, accidents etc. Remember, land is a non-depreciable asset in developing countries like India, whereas it may not be so in certain developed countries where the real estate values are nose diving. Issue of Equity shares – To raise capital free of interest, many big corporate firms go for equity capital from the general public. But the firms should make it a point to declare dividends if it happens to reap enormous profit to retain their market share. Their main aim should be to protect the interests of the equity share holders who are also the owners. Fund that comes into the firm through business operations – through sale of goods and services. Here the firm has to factorise its cost of production and economy of scale in order to make it cost-effective and fix a feasible profit margin. Borrowing of loans from banks and other financial institutions – Although it is a quick way of raising fund, care should be exercised in that, you should be in a comfortable position to “service the debt“. If not, there lurks the danger of bankruptcy where the firm might become insolvent, if it is unable to repay the interest and principal over a period of time. Issue of debentures – Debentures are also a form of equity but it comes with a price. The firm has to pay a percentage as interest on debentures and repayment period is also fixed in advance. The only solace for the firms would be the tax rebate that can be availed on loans and...

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

Debtor Management or Receivables Management Profit is directly proportional to the volume of sales, provided all your business transactions are cash based. Is it possible for a manufacturer, wholesaler or retailer to carry on his business without offering credit in this competitive business environment? The answer is a definite “no”, because extension of credit improves your sales and thus your profit. Problems arise only when a firm is not able to recover the debt within the stipulated period of time from the customers. What is receivables management or debtors’ management? It covers two aspects- one, the kind of money that is being invested in debt rotation; second, the risk factor which includes loss of money or the opportunity cost foregone by the organisation. Had these funds not been tied in receivables, the firm would have invested the same elsewhere and earned income thereon. A transaction entirely through cash is definitely a possible option, but whether it is lucrative in the long run must be subject to consideration. When customers are not offered credit, they choose concerns that extend credit facilities and thus you may lose your earlier customers and also exposed to the risk of declining sales proportions. Credit Sales In credit sales, the supplier offers credit for a specific time period, which is an investment from the angle of supplier and largest single source of short term financing from the angle of the customer. The supplier should be able to recover the amount of interest on the credit investment he has made. How? Recovery of debt within the stipulated credit period Taking interest from the customer for the period of delay Volume sales Surplus capital to offset these negative impacts on rotation of funds Proper formulation and execution of credit policies by the finance manager Discipline in collection policy and its execution. Discounts Cash discounts, quantity discounts and trade discounts are offered by many firms to the customers to encourage credit sales, favoring bulk purchases. A firm cannot be expected to survive long by pursuing the policy of cash sales while similar firms can overtake it by adapting to liberal credit policies. The main aspects of receivables management decisions are as follows: Time period of credit Credibility of the customer Cash discounts Trade discounts Learn the basics of the Income Statement, Balance Sheet and Cash Flow Statement and understand how they fit together. Credit Policy Credit policy on one hand stimulates sales and so also its gross earnings, but on the other may be accompanied by added costs, such as: 1) Clerical expenses involved in investigating additional accounts and servicing added volume of receivables, 2) increased bad-debt losses due to credit extension to less credit worthy customers, 3) higher cost of capital. Incremental earnings from increased sales should be matched with incremental costs that arise due to credit terms, to avoid funds being tied up in receivables. In course of time it would deprive you of your profits. The pivotal consideration of your credit policy would be the selection of credit worthy customers or debtors. If your funds become sticky, recovery becomes next to impossible and you need to proceed legally to claim your rights. Properly maintained accounting records and vouchers will stand as a testimony in your favor, in the court of...