Posted by Managementguru in Business Management, Organisational behaviour, Principles of Management

on Mar 2nd, 2014 | 0 comments

Principles of Planning and Forecasting The guidelines of principles of planning are as follows: 1. Principle of primacy of planning: As discussed earlier planning is the prime function of management and precedes all the other functions. 2. Principle of verifiable objectives: The objectives set must be clear, achievable and verifiable in order to attain a feasible management model. 3. Principle of planning premises: The contributing factors in the external environment are government policies, economic factors, market standing, and consumer preferences etc. that decide the success of planning. Planning is done based on these assumptions but nevertheless, all the factors external to the business have to be thoroughly analyzed to ensure concrete planning. 4. Principle of limiting factor: Cost is one of the major limiting factor; production cost has to be factorized to ensure economy of scale and potential resources needed for a business in the likes of men, material and other physical resources have to be taken into consideration. 5. The commitment principle: Planning and decisions whether short term or long term is valid only for a particular period. The long term plan is nothing but the future impact of today’s decisions. Decisions concerning new product development by a company aims at creating an impact for the next 15 years or so while decisions concerning sales target has to be accomplished on a periodic basis- monthly or quarterly. 6. Principle of flexibility: A plan should be flexible and give room for contingencies like losses incurred through unexpected events. 7. Principle of navigational change: Plans while suggested to have built-in flexibility are also subjected to periodical review in the light of environmental fluctuations. A business can not stick to a long term plan devised originally since it is equally important to check on events and expectations periodically. FORECASTING AND PLANNING: Forecasting is a management technique that relies on both past experiences and present assumptions to predict the future. Again this serves as an important premise for the planning process. The conditions of the external environment though out of one’s control, if properly estimated, can lead an organization to produce wonderful results. TYPES OF FORECSATS: Economic forecast: To gauge the general economic scenario and its effect on sales. Technological forecast: To predict what new technologies can be developed, when and how to bring feasibility to the operations involved. Competition forecast: To look into the competitor strength and tactics and know where one stands. Social forecast: To predict the attitude of people and social conditions. Supplier’s forecast: Reveals the response of suppliers. FORECASTING TECHNIQUES: 1. Quantitative time series analysis: Monthly sales data is plotted in a chart and the past data helps in consolidating the sales volume and fluctuations in sales. Sales trend is determined and the assumption is that, the future will reflect the past and present trend and hence can be projected. If there is a lull in sales, reasons for the decline can be known by taking feedback from various quarters like, suppliers, consumers and employees. 2. Derived forecast: The forecast done for a specific purpose may be reused for another purpose. For example a census data can help you to determine the demography of a particular geographical area that might help you to reach your target customers. 3. Casual methods: If the underlying cause for the variable can be determined, the forecast can be arrived mathematically and produce quite accurate results. Social media marketing is very popular now a days and instantly you know how many hits are received for a particular product and the ratio of conversion into sales. 4. Brain storming: People with knowledge and expertise assemble in order to discuss the pros and cons of a particular idea, be it the launch of a new product, product promotion or withdrawal of a product line. 5. Delphi method: In this method, each and very expert is contacted independently and opinions are drawn...

Posted by Managementguru in Business Management, Organisational behaviour, Principles of Management

on Mar 2nd, 2014 | 0 comments

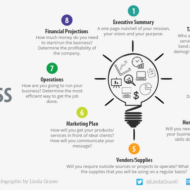

Your business structure will affect a lot of factors – You can start with an initial business structure and change it as your business thrives. But first and foremost you need a solid business plan that details your mission, vision and purpose. These 7 steps in planning will guide you through and give your project a headstart. The business plan cheatsheet is given in a pictorial form for your benefit. ☝️ A. Opportunity Analysis: SWOT analysis– the analysis of strength and weaknesses, opportunities and threats in the external environment is the first and foremost step in planning. The target market, competitor strength, internal weaknesses, customer’s preferences are some of the key areas to be focused. B. Setting objectives: Where we want to be, and what we want to accomplish and when are answered in this step. Each and every employee of the organization has to be apprised about the enterprise objectives in order to achieve the expected or desired result. Management by objectives is one of the proven methods where-in the objectives are set by the subordinates themselves under the guidance of their superior and periodical reviews are conducted to check whether the set objectives are accomplished within the stipulated time. C. Developing Premises: The critical factors that affect the planning process are analyzed thoroughly. Say, government policies, business cycle trends, economic indicators, inflation, tax rates etc are analyzed and the plans are developed based on these premises. D. Identifying Alternatives: It is better to have an alternate plan or plans which helps in deciding the alternate course of action. Alternatives identification is a technique used for identifying different methods or ways of accomplishing the work of the project. For example, brainstorming might be used to discover alternative ways of achieving one of the project objectives. E. Evaluating Alternatives and selecting the suitable plan: The limiting factors can be set as a criterion for evaluating the alternatives. The limiting factors may be cost, time, manpower and other resources. Operations research helps in the assessment of alternatives and selecting the best. Think about this, if plan A fetches you more profit but proves to be expensive and plan B fetches you consistent profit and less expensive, what will be your choice? Even banks look into the fund flows of different projects submitted by clients and select the ones that proves to fetch consistent returns on the long run. F. Formulating Supportive plans: Download this Business Planner Printable which comes in handy when you want to weigh your choices👇 Business-Journal-Planner-1Download Derived plans are those that stem from the main ones that support the basic plan. Recruiting and inducting may be the basic plan of a HR department but training and development is the supporting plan that gives shape to the basic plan. G. Developing Budgets: Budget is referred in financial terms and they are required to control plans. There is always a constraint for resources and hence it is the responsibility of a manager to decide on the investment in a particular plan that will tide away the risk of the...

Posted by Managementguru in Business Management, Organisational behaviour, Principles of Management

on Mar 2nd, 2014 | 0 comments

Nature of Organizational Planning What is Planning? “Planning is an intellectual process, the conscious determination of courses of action, and is a continuous process of decision making with built in flexibility.”- Herold Koonz and Weirich Planning is the most basic and primary of all management functions on the premise of which other functions evolve. It would be appropriate to compare planning to the basement or foundation of a building upon which the entire system rests. Planning bridges the gap from where we are to where we want to go. Planning involves selecting the best objectives and deciding on the suitable course of action. When we talk about planning, control is another entity that tags along like inseparable two-sides of a coin. Without planning there is no control and without control planning becomes meaningless. NATURE OF PLANNING: Prime function of management: Planning is the key to all other functions of management like organizing, leading, staffing and controlling. Is a continuous process: Plans need periodic review in the wake of external environment and internal resource potential and thus is a continuous process. Is an intellectual process: What is to be done, when, who and how are the very important questions that loom before a manager before making every decision. He has to use his intellect in order to make the right plans before acting. Is all pervasive: It penetrates right from the top to the bottom level of management, but it is the responsibility of the managers or executives at the top level to make the right moves at the right time. Is flexible: One has to understand that flexibility is restricted when it comes to irretrievable costs already incurred in fixed assets, training, advertising etc. Is goal oriented: Planning starts with setting up of objectives and completely goal oriented. TYPES OF PLANS: Purpose or Missions: Basic task of an organization. For example, teaching and research can be attributed as the basic function of an educational institution; the purpose of business is to produce, distribute goods and make a surplus. Objectives: These are the goals that have to be accomplished by the organization. Corporate companies chart out their production plan well in advance to meet the requirements on time. For this they break the objectives into short term goals i.e., for a quarter based on the sales forecast. This kind of planning gives clarity and direction for the production team to achieve the goals. Strategies: These are the set of action plans designed in order to achieve the future objectives backed up by long term perspective in the wake of environmental analysis and give direction in which the resources have to be channelized. Policies: These are basically the guideline books that direct the course of the organization’s function as what to do and what not to-do. They see to that the decisions made fall well within certain boundaries in order to ensure fair and equitable treatment to all the employees. HR policies govern all the functions related to pay, promotion and other disciplinary mechanisms related to the work force. Procedures: They are programmes designed to carry out the activities of the organization in a specified manner. The procedures for placing a purchase order, payment collection etc., Programmes: A programme is the sum total of goals, policies, procedures, rules, task etc., For example, new product development may be cited as a major programme while promotional campaign may be cited as a supporting programme. Budget: No plan is feasible without a budget allocated to it. A budget is a numberised programme and more of a control device. Revenue budgets, expense budgets, production budgets to name a few. Zero base budget: This kind of budget does not take into account the previous year’s performance record or budget but treats every progarmme afresh and starts working from ground up. Each programme is treated as a separate...

Posted by Managementguru in Entrepreneurship, Human Resource

on Mar 1st, 2014 | 0 comments

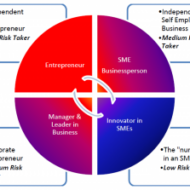

The Spirit of Entrepreneurship In the modern competitive business environment, not all graduates of various disciplines like engineering, management and the like can aspire for white collar jobs. The recent global recession has made the prospective job seekers think twice about working in foreign countries. Self employment has become the order of the day. Being your own boss is truly inspiring and motivating at least in theory. When it comes to reality, we need to know exactly what does it take to become an entrepreneur by starting a small business or taking over the business run by your predecessors. Why we need more entrepreneurs? Various avenues have been opened up thanks to communication and transportation that has brought the world under a single huge umbrella. Also small industries face minimum risk as the investments are marginal and they have the liberty to try a number of innovations like combination of new products new materials new methods of production new markets new sources of materials and even New forms of organization. Being a competitor in an open market, minimum profit and constant revenue inflow are assured and also they can enjoy the benefit of minimum fluctuation in the product price as it is determined by the market and not by individuals. Want to know 10 Daily Habits of Most Successful Entrepreneurs? Scope of entrepreneurial activity: Either you can be a subsidiary to large scale business or you can engage yourself in supply of repair services with small engineering establishments or you can go for small cottage industry businesses like cutlery, furniture, jewelry, fruit canning, soap making etc., Being fairly labor intensive, you can provide economic solution by creating employment and income opportunities in urban and rural areas with relatively low cost of capital investment. Business process outsourcing has been in recent times the magic happening in countries like India, China etc., where the foreign investors take advantage of cheap labor, time and efficient communication skills of the population. Knowledge process outsourcing has also become popular and it stands as a testimony of the rising power of Asian countries over the west. “Small is beautiful” and you can make it big in the small scale business industry if you are Innovative and productive Provide personalized services to the customers Identify and target the right markets This ensures “WINNING THE GAME OF BUSINESS“. An economy grows only when it has large number of enterprises accelerating the economic growth prospects of that particular country. The export policies of all nations have become more flexible owing to globalization, liberalization and...

Posted by Managementguru in Financial Management, Principles of Management

on Feb 28th, 2014 | 0 comments

There is no Business Success Without Risk What is the Risk of Taking a Chance in a Business Activity? Business is often viewed as a game or a gamble in which success is always at risk. Think about it, risk is present in every sphere and aspect of our lives and even when you are not running a business. So why the fuss? A thorough knowledge and research of the business activity you are about to perform will give you the needed confidence to go about it. A true business man is an entrepreneur who treats risk as an opportunity rather than a challenge. Business organizations are started with a single purpose, to make profit and then more profit. Only when the organizations grow, there comes the awareness and necessity to think about stakeholders’ interest and working towards a social cause. Initial stages definitely pose threats for the very survival of the organization. Risk is an inherent part of a business as you are not sure about the outcome of your business activity. What are the Chances or Probability? We talk more about probability and chance outcomes when you deal with a particular product. Retail segment is one area where the risk of duplication is high and people have to be cautious and careful in order to protect their copyrights and symbols from being replicated. Mild inflations can benefit the market but recessions put you in doldrums especially if you are dependent on a wholesaler or a manufacturer. Risk can aspect itself in the following ways: Economically- Attrition and effects of global economy Legally- Labor laws and enactments Socially- Expectations from the public in general Government rules and regulations- Government policies and export duties Stakeholder expectations- Wealth maximization and assured profits Environmental – Need to comply with changing standards like waste affluent treatment plants Political scenario- Effects due to changing governments Risk and Uncertainty Risk and uncertainty go hand in hand and you need a risk management template or a model for your reference to solve or manage risks. The first and foremost step would be to identify the risks in your sphere of business activity. Risk documentation or creating a risk profile is an inevitable move for a new organization. This prepares the organization mentally to face challenges in a structured manner and reduces disorientation. It is very important to keep in mind the organisation’s objectives while documenting the risk profile to keep your focus unaltered. Risks evolve continuously and it is the responsibility of the top management to be in line with the market economy to manage the adverse conditions that come in the way. How to Manage Risks? Risk management is an ongoing and continuous process and it cannot be looked upon as a distinct area to be managed by a set of individuals. In a small and upcoming organization the responsibility lies on the shoulders of each and every individual to self assess, evaluate and manage risks and find the right kind of solution that will not be detrimental to the core objectives of the organization. Bigger organizations can afford to have expert opinion by commissioning PROFESSIONALS to identify, assess and manage risks. An overall and broad perspective of risk is what has been analysed here. There are numerous possibilities of risks, whether big or small in magnitude, affecting an organization. A thorough study of the field you are about to venture into, the pros and cons of the business activity, time of launch are few things that will help you to analyse what the market niche warrants for and act accordingly. In further segments, let us look into the factors of risk, identifying and...