Posted by Managementguru in Financial Management, Principles of Management

on Feb 28th, 2014 | 0 comments

There is no Business Success Without Risk What is the Risk of Taking a Chance in a Business Activity? Business is often viewed as a game or a gamble in which success is always at risk. Think about it, risk is present in every sphere and aspect of our lives and even when you are not running a business. So why the fuss? A thorough knowledge and research of the business activity you are about to perform will give you the needed confidence to go about it. A true business man is an entrepreneur who treats risk as an opportunity rather than a challenge. Business organizations are started with a single purpose, to make profit and then more profit. Only when the organizations grow, there comes the awareness and necessity to think about stakeholders’ interest and working towards a social cause. Initial stages definitely pose threats for the very survival of the organization. Risk is an inherent part of a business as you are not sure about the outcome of your business activity. What are the Chances or Probability? We talk more about probability and chance outcomes when you deal with a particular product. Retail segment is one area where the risk of duplication is high and people have to be cautious and careful in order to protect their copyrights and symbols from being replicated. Mild inflations can benefit the market but recessions put you in doldrums especially if you are dependent on a wholesaler or a manufacturer. Risk can aspect itself in the following ways: Economically- Attrition and effects of global economy Legally- Labor laws and enactments Socially- Expectations from the public in general Government rules and regulations- Government policies and export duties Stakeholder expectations- Wealth maximization and assured profits Environmental – Need to comply with changing standards like waste affluent treatment plants Political scenario- Effects due to changing governments Risk and Uncertainty Risk and uncertainty go hand in hand and you need a risk management template or a model for your reference to solve or manage risks. The first and foremost step would be to identify the risks in your sphere of business activity. Risk documentation or creating a risk profile is an inevitable move for a new organization. This prepares the organization mentally to face challenges in a structured manner and reduces disorientation. It is very important to keep in mind the organisation’s objectives while documenting the risk profile to keep your focus unaltered. Risks evolve continuously and it is the responsibility of the top management to be in line with the market economy to manage the adverse conditions that come in the way. How to Manage Risks? Risk management is an ongoing and continuous process and it cannot be looked upon as a distinct area to be managed by a set of individuals. In a small and upcoming organization the responsibility lies on the shoulders of each and every individual to self assess, evaluate and manage risks and find the right kind of solution that will not be detrimental to the core objectives of the organization. Bigger organizations can afford to have expert opinion by commissioning PROFESSIONALS to identify, assess and manage risks. An overall and broad perspective of risk is what has been analysed here. There are numerous possibilities of risks, whether big or small in magnitude, affecting an organization. A thorough study of the field you are about to venture into, the pros and cons of the business activity, time of launch are few things that will help you to analyse what the market niche warrants for and act accordingly. In further segments, let us look into the factors of risk, identifying and...

Posted by Managementguru in Business Management, Financial Management, Principles of Management, Project Management

on Feb 28th, 2014 | 0 comments

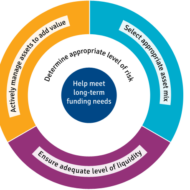

What is Business Risk? It is a term that explains the difference between the expectation of return on investment and actual realization. In CAPITAL BUDGETING, several alternatives of investments are examined before taking an investment decision and only then the Managing Director of the firm along with financial executives gear up for investing in a project that is sound and feasible. Even then the project may not become viable owing to the fluctuations in the economic environment. Money Manipulation So, the million dollar question arises, whether to invest and if invested, will it fetch me profit? See, you cannot have the cake and eat it too. Risk factor prevails in all kinds of environment and we try to over react in a business arena since it involves huge investments. But remember, MONEY WILL MULTIPLY IF YOU MANIPULATE IT WITH CARE. Business firms commit large sums of money each year for capital expenditure. It is therefore essential that a careful FINANCIAL APPRAISAL of each and every project which involves large investments is carried out before acceptance or execution of the project. These capital budgeting decisions generally fall under the consideration of highest level of management. Factors of risk to be considered before investing: Time value of money Pay back period Rate of return on investment(ROI) Uncertainties in the market Cost of debt Cost of equity Cost of retained earnings Factors to be monitored after investing: Maximising profit after taxes Maximizing earnings per share Maintaining the share prices Issue of dividends Ensuring management control Financial structuring Cost of capital refers to the opportunity cost of the funds to the firm I. e., the return on investment to the firm had it invested these funds elsewhere. Servicing the debt and Danger of Insolvency While making the decisions regarding investment and financing, the Finance Manager seeks to achieve the right balance between risk and return. If the firm borrows heavily to finance its operations, then the surplus generated out of operations should be sufficient to “SERVICE THE DEBT” in the form of interest and principal payments. The surplus would be greatly reduced to the owners as there would be heavy Debt Servicing. If things do not work out as planned, the situation becomes worse, as the firm will not be in a position to meet its obligations and is even exposed to the “DANGER OF INSOLVENCY“. Working Capital Management Considering all these factors, we have to come to the conclusion that FINANCIAL MANAGEMENT is like the BACKBONE of a business firm and WORKING CAPITAL MANAGEMENT will be the blood flow infused into the body. Risks are inherent in a business environment whose management is quite possible with the right kind of farsightedness and planning. Luck does not favor anybody who is poor in planning and lack hard...

Posted by Managementguru in Human Resource, Training & Development

on Feb 28th, 2014 | 0 comments

Definitions of Human Resource Management: 1. “A series of integrated decisions that govern employer-employee relations. Their quality contributes to the ability of organisations and employees to achieve their objectives.” (Milkovich & Boudreau, 1997). 2. “Concerned with the people dimension to management. Since every organisation comprises people, acquiring their services, developing their skills, motivating them to higher levels of performance and ensuring that they continue at the same level of commitment to the organisation are essential to achieving organisational goal. This is true, regardless of the type of organisation: viz. government, business, education, health, recreation, or social action.” (Decenzo & Robbins, 1989). 3.”The planning, organising directing and controlling of the procurement, development, compensation, integration, and maintenance of human resource to the end those individual, organisational, and social objectives are accomplished.” (Flippo, 1984). 4. “The organisation function that focuses on the effective management, direction, and utilisation of people; both the people who manage produce and market and sell the products and services of an organisation and those who support organisational activities. It deals with the human element in the organisation, people as individuals and groups, their recruitment, selection, assignment, motivation, empowerment, compensation, utilisation, services, training, development, promotion, termination and retirement.”(Tracey,1994 ) Knowledge Workers Human resource management is therefore understood as the all significant art and science of managing people in an organisation. Increasing research output in behavioral sciences, new trends in managing ‘knowledge workers’ and advances in training methodology and practices have led to substantial expansion of the scope of human resource management function in recent years. HRM is not just an arena of personnel administration anymore but rather a central and pervasive general management function involving specialised staff as assistants to main line managers. Managing employee relationships is the role of the Human Resource department Human Resource Management is a process of valuing and developing people at work, this includes: Recruitment and selection Employee communication and engagement (participation) to increase employee retention Training and development Leadership WHAT IS YOUR GREATEST WEAKNESS Labour turnover & staff retention Labour turnover refers to the proportion of a workforce that leave during a period of time (usually one year) Labour turnover = number of staff leaving during the period x 100 average number of staff Staff retention refers to the ability of a firm to keep its workers. The disadvantages of having a large proportion of staff leaving each year include: The cost of recruiting replacement workers The cost of training the new workers Loss of productivity whilst replacements are found Loss of experienced workers Negative impact on reputation WHAT IS YOUR GREATEST STRENGTH Methods to control turnover: 1. Financial methods of motivation Bonuses Profit share Fringe benefits 2. Non financial methods of motivation Employee engagement and empowerment Training and development Promotion opportunities 3. Improved Human Resource Management procedures Four Fundamental Principles of HRM: Human Resource is the organisation’s most important asset; Personnel policies should be directed towards achievement of ENTERPRISE goals and strategic plans; Corporate culture exerts a major influence on achievement of excellence and must therefore be strengthened with consideration of employee welfare. Whilst integration of corporate resources is an important aim of HRM, it must also be recognised that all organisations are ‘pluralist societies’ in which people have differing interests and concerns, which they defend and at the same time function collectively as a cohesive group. →Evolution of...

Posted by Managementguru in Business Management, Decision Making, Principles of Management

on Feb 26th, 2014 | 0 comments

METHODS OF DECISION MAKING A. Marginal income or Cost analysis: This method is used to compare additional revenues arising from additional costs. Break even point is that point in which the cost equals revenue and it can be defined as a no loss, no gain situation. Profit can be enjoyed by a firm only when the revenue exceeds cost that is after crossing the break even point. A manager must have all the necessary data pertaining to total cost and its various components in order to arrive at a decision. B. Cost-effective analysis: This tries to find out the cheapest way in reaching the objective or shall we say the greatest value for expenditure. Mass production facilitates in factorizing the economies of scale where the objective is oriented towards output and sustained availability of the product year round. C. Experience: The mistakes committed become great lessons in due course of time generally and this holds good for managers involved in making crucial decisions. It ensures right decisions to be taken in similar situations. But one has to remember that decisions are inclined to make an impact on future events. So, it is up to the manager to take the right kind of decisions using his intuitions as well as experience. The late chairman of SIMPSONS GROUP, Anantharamakrishnan was very intuitive and under his leadership the organization touched new heights and diversified its activities like never before. Note: Anantharamakrishnan is remembered for his successful business practices, efficient management of the labour unions and for triggering the growth of the automobile industry of Chennai which has earned the city the epithet “Detroit of India”. As a result he himself came to be remembered as the “Henry Ford of South India.” Courtesy: Wikipedia D. Experimentation: Why people go for test-marketing? Because when the factors are intangible, you have to try out every alternative only through experiments or trail and error. Market surveys and questionnaires are useful tools when it comes to launching of a new product in the target market. E. Research and analysis: This involves the application of tools and techniques of operations research to the process of decision making based on mathematical functions. Risk-analysis and Decision-trees are the other methods used that illustrate decision points, chance events, and probability of each course of action. TYPES OF DECISIONS: · Routine and Strategic: Routine- regular decisions involving day to day affairs of the firm- leave procedures, work atmosphere. Strategic decisions are central to the firm’s operations- price fixing, product elimination etc. · Individual and Group decisions: Managers at the top level are inclined to take individual decisions and some important inter-departmental decisions may be taken up by members of the respective groups. · Programmed and Non-programmed decisions: Decision taken by the low-level personnel which are regular and repetitive in nature are programmed-late attendance, medical compensation etc., Non-repetitive and unusual decisions like mergers and acquisitions, collaboration agreements belong to the non-programmed category. · Simple and Complex decisions: Where the problem is simple but the outcome has a high degree of certainty are called mechanistic or routine decisions. Where the problem is simple but the outcome has a low degree of certainty are judgmental in nature. Where the problem is complex and the outcome has a high degree of certainty are analytical and where the problem is complex but the outcome has low degree of certainty are adaptive decisions. MAKING EFFECTIVE DECISIONS: · Timing of decisions: A new product only if introduced into the market at the right time will be a success for which the manager should select the appropriate time for taking the decisions. · Effective communication: The decisions taken should be communicated down the line for effective implementation. · Top management support: The support of top management is indispensable for effective decision-making since it...

Posted by Managementguru in Business Management, Decision Making, Principles of Management, Productivity

on Feb 26th, 2014 | 0 comments

The Process of Decision Making There is a need to broaden our understanding about decision-making process. Decision making is not an independent entity and relies upon many other factors like precedence, social processes and random eventualities. It has three components; identification of the issue, the possible course of action and choosing the best amongst the choices of action available. The decision-making process is continuous since the business environment is dynamic and constantly poses challenges to the decision makers. Organizations are viewed as “Garbage can models” of decision making, in which actions, decisions and outcome are randomly mixed in the flow of events. With this introduction let us proceed to know more about the nature and types of decision making. NATURE OF DECISION-MAKING: 1. It is closely related to solving problems and issues 2. It is associated with all the important management functions like planning, organizing and controlling 3. Fayol and Urwick feels that decision-making is concerned only to the extent that it affects delegation and authority 4. Chester I Bernard in his “Functions of the Executive” says that the process is nothing but narrowing down of choice 5. Herbert A Simon considers decision-making as a process of intelligence, design and choice activities 6. According to Peter Drucker, it is a central part of the management process THE DECISION-MAKING PROCESS: The following steps are involved in the process of decision-making Recognizing the problem: Think about this; if there is a decline in the sales volume of your company or say if the value of your stock decreases, you are forced to make decisions to manage the contingency. In such situations, the first step would be to recognize or identify the problem area. A problem identified is half done. In this instance, the reason might be competitor strength or lack of necessary investment in the key strategic business units. Deciding priorities among the problems: A manager need not and cannot look after all the problems prevailing in the organization. He should know how to delegate authority and the responsibility that goes along with it. Subordinates can be entrusted with the handling of small and trivial problems while the manager can handle very important ones that might affect the functioning of the firm. He should ask the following questions to diagnose the situation. 1. What is the real problem? 2. What are the causes and effects of the problem? 3. Is this problem very important? 4. Can sub-ordinates handle this problem? 5. Which is the most pressing problem to be solved? Diagnosing the problem: Now the manager must start diagnosing the problem. Each and every individual has a different perspective and perceive the problem from a different angle. This depends upon the background orientations and training. The right way of approach for any manager would be to systematically analyze the problem for identifying the alternative courses of action. Developing alternative courses of action: This step involves creativity and innovative capabilities as the manager has to think from all possible angles and directions. Managers holding senior corporate positions are exposed to more of this kind of atmosphere where they are forced to make quick decisions in accordance with what the situation demands. Outside expert consultants are also put into use by some companies for developing choice alternatives. The following are the five PSYCHOLOGICAL STEPS for developing alternatives: 1. Saturation– A manager must be thoroughly familiar with the problem 2. Deliberation– Analyzing the problem from several points of view 3. Incubation– Temporarily switching off the conscious search to relax for the purpose of clear thinking 4. Illumination– A flash of light may occur after sometime giving him the right insights and ideas. 5. Accommodation– The ideas are made into a concrete proposal Evaluating the alternatives: The pros and cons of each and every choice is thoroughly subjected to scrutiny in terms of cost, time, risk, results expected, deviations anticipated...