Posted by Managementguru in Financial Management

on Dec 19th, 2014 | 0 comments

Meaning and Definition of Finance Meaning of Finance The science that describes the management, creation and study of money, banking, credit, investments, assets and liabilities. The financial systems include the public, private and government spaces, and the study of finance and financial instruments, which can relate to countless assets and liabilities. Finance is divided into three distinct categories: public finance, corporate finance and personal finance, all three consisting of many sub-categories. The one word which can easily substitute finance is “exchange.” Finance is nothing but an exchange of available resources. Finance is not restricted only to the exchange and/or management of money. A barter trading system is also a type of finance. Thus, we can say, Finance is an art of managing various available resources like money, assets, investments, securities, etc. Some Definitions of Finance The concept of finance includes capital, funds, money, and amount. But each word has its unique meaning. Studying and understanding the concept of finance becomes an important part of the business concern. Definition of Business Finance According to the Wheeler, “Business finance is that business activity which concerns with the acquisition and conversation of capital funds in meeting financial needs and overall objectives of a business enterprise”. According to the Guthumann and Dougall, “Business finance can broadly be defined as the activity concerned with planning, raising, controlling, administering of the funds used in the business”. In the words of Parhter and Wert, “Business finance deals primarily with raising, administering and disbursing funds by privately owned business units operating in non-financial fields of industry”. The term finance comes from the Latin “finis” which means end or finish . It is a term whose implications affect both individuals and businesses, organizations and states it has to do with obtaining and using or money management – Ivan Thompson According to Bodie and Merton, finance is the “study how scarce resources are allocated over time”. Corporate Finance Corporate finance is concerned with budgeting, financial forecasting, cash management, credit administration, investment analysis and fund procurement of the business concern and the business concern needs to adopt modern technology and application suitable to the global environment. Corporate finance is the area of finance dealing with the sources of funding and the capital structure of corporations and the actions that managers take to increase the value of the firm to the shareholders, as well as the tools and analysis used to allocate financial resources. The financial activities related to running a corporation. A division or department that oversees the financial activities of a company. Corporate finance is primarily concerned with maximizing shareholder value through long-term and short-term financial planning and the implementation of various strategies. Everything from capital investment decisions to investment banking falls under the domain of corporate finance. According to the Encyclopedia of Social Sciences, “Corporation finance deals with the financial problems of corporate enterprises. These problems include the financial aspects of the promotion of new enterprises and their administration during early development, the accounting problems connected with the distinction between capital and income, the administrative questions created by growth and expansion, and finally, the financial adjustments required for the bolstering up or rehabilitation of a corporation which has come into financial difficulties”. The core corporate finance principles can be stated as follows: The Investment Principle: It is better to invest in assets and projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects and should reflect the financing mix used—owners funds (equity) or borrowed money (debt). Returns on projects should be evaluated based on cash flows generated and the timing of these cash flows; they should...

Posted by Managementguru in Financial Accounting, Financial Management, Management Accounting

on Apr 3rd, 2014 | 0 comments

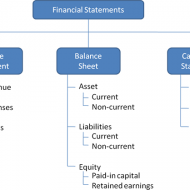

Ratio Calculation From Financial Statement Profit and Loss a/c of Beta Manufacturing Company for the year ended 31st March 2010. Exercise Problem1 Kindly download this link to view the exercise. Given in pdf format. You are required to find out: a) #Gross Profit Ratio b) #Net Profit Ratio c) #Operating Ratio d) Operating #Net Profit to Net Sales Ratio a. GROSS FORFIT RATIO = Gross profit ÷ #Sales × 100 = 50,000 ÷ 1,60,000 × 100 = 31.25 % b. #NET PROFIT RATIO = Net profit ÷ Sales × 100 = 28,000 ÷ 1,60,000 × 100 = 17.5 % c. OPERATING RATIO = #Cost of goods sold + Operating expenses ÷ Sales × 100 Cost of goos sold = Sales – Gross profit = 1,60,000 – 50,000 = Rs. 1,10,000 Operating expenses = 4,000 + 22,800 + 1,200 = Rs. 28,000 Operating ratio = 1,10,000 + 28,000 ÷ 1,60,000 × 100 = 86.25 % d. OPERATING NET PROFIT TO NET SALES RATIO = Operating Profit ÷ Sales × 100 Operating profit = Net profit + Non-Operating expenses – Non operating income = 28,000 + 800 – 4,800 = Rs. 32,000 Operating Net Profit to Net Sales Ratio = 32,000 ÷ 1,60,000 × 100 = 20 % What is a Financial statement? It is an organised collection of data according to logical and consistent #accounting procedure. It combines statements of balance sheet, income and retained earnings. These are prepared for the purpose of presenting a periodical report on the program of investment status and the results achieved i.e., the balance sheet and P& L a/c. Objectives of Financial Statement Analysis: To help in constructing future plans To gauge the earning capacity of the firm To assess the financial position and performance of the company To know the #solvency status of the firm To determine the #progress of the firm As a basis for #taxation and fiscal policy To ensure the legality of #dividends Financial Statement Analysis Tools Comparative Statements Common Size Statements #Trend Analysis #Ratio Analysis Fund Flow Statement Cash Flow Statement Types of Financial Analysis Intra-Firm Comparison Inter-firm Comparison Industry Average or Standard Analysis Horizontal Analysis Vertical Analysis Limitations Lack of Precision Lack of Exactness Incomplete Information Interim Reports Hiding of Real Position or Window Dressing Lack of Comparability Historical...

Posted by Managementguru in Accounting, Financial Management, Management Accounting, Principles of Management

on Mar 28th, 2014 | 0 comments

ROI – Return on Investment Ratios PROFITABILITY IN RELATION TO INVESTMENTS Return on gross investment or gross capital employed Return on net investment or net capital employed Return on shareholder’s investment or shareholder’s capital employed. Return on equity shareholder investment or equity shareholder capital employed. 1. RETURN ON GROSS CAPITAL EMPLOYED This ratio establishes the relationship between net profit and the gross capital employed. The term gross capital employed refers to the total investment made in business. The conventional approach is to divide Earnings After Tax (EAT) by gross capital employed. Return on gross capital employed = Earnings After Tax (EAT) X 100 / Gross capital employed 2. RETURN ON NET CAPITAL EMPLOYED It is calculated by dividing Earnings Before Interest & Tax (EBIT) by the net capital employed. The term net capital employed in the gross capital in the business minus current liabilities. Thus it represents the long-term funds supplied by creditors and owners of the firm. Return on net capital employed = Earnings Before Interest & Tax (EBIT) X 100 / Net capital employed 3. RETURN ON SHARE CAPITAL EMPLOYED This ratio establishes the relationship between earnings after taxes and the shareholder investment in the business. This ratio reveals how profitability the owners’ funds have been utilized by the firm. It is calculated by dividing Earnings after tax (EAT) by shareholder capital employed. Return on share capital employed = Earnings after tax (EAT) X 100 / Shareholder capital employed 4. RETURN ON EQUITY SHARE CAPITAL EMPLOYED Equity shareholders are entitled to all the profits remaining after the all outside claims including dividends on preference share capital are paid in full. The earnings may be distributed to them or retained in the business. Return on equity share capital investments or capital employed establishes the relationship between earnings after tax and preference dividend and equity shareholder investment or capital employed or net worth. It is calculated by dividing earnings after tax and preference dividend by equity shareholder’s capital employed. Return on equity share capital employed = Earnings after tax (EAT), preference dividends X 100 / Equity share capital employed. The following are some of the important and basic concepts to be understood in management accounting: EARNINGS PER SHARE IT measures the profit available to the equity shareholders on a per share basis. It is computed by dividing earnings available to the equity shareholders by the total number of equity share outstanding. Earnings per share = Earnings after tax – Preferred dividends (if any) / Equity shares outstanding DIVIDEND PER SHARE The dividends paid to the shareholders on a per share basis in dividend per share. Thus dividend per share is the earnings distributed to the ordinary shareholders divided by the number of ordinary shares outstanding. Dividend per share = Earnings paid to the ordinary shareholders / Number of ordinary shares outstanding DIVIDENDS PAY OUT RATIO (PAY OUT RATIO) It measures the relationship between the earnings belonging to the equity shareholders and the dividends paid to them. It shows what percentage shares of the earnings are available for the ordinary shareholders are paid out as dividend to the ordinary shareholders. It can be calculated by dividing the total dividend paid to the equity shareholders by the total earnings available to them or alternatively by dividing dividend per share by earnings per share. Dividend pay our ratio (Pay our ratio) = Total dividend paid to equity share holders / Total earnings available to equity share holders Or Dividend per share / Earnings per share DIVIDEND AND EARNINGS YIELD While the earnings per share and dividend per share are based on the book value per share, the yield is expressed in terms...