Posted by Managementguru in Financial Accounting, Financial Management, Management Accounting

on Apr 3rd, 2014 | 0 comments

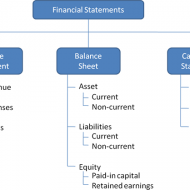

Ratio Calculation From Financial Statement Profit and Loss a/c of Beta Manufacturing Company for the year ended 31st March 2010. Exercise Problem1 Kindly download this link to view the exercise. Given in pdf format. You are required to find out: a) #Gross Profit Ratio b) #Net Profit Ratio c) #Operating Ratio d) Operating #Net Profit to Net Sales Ratio a. GROSS FORFIT RATIO = Gross profit ÷ #Sales × 100 = 50,000 ÷ 1,60,000 × 100 = 31.25 % b. #NET PROFIT RATIO = Net profit ÷ Sales × 100 = 28,000 ÷ 1,60,000 × 100 = 17.5 % c. OPERATING RATIO = #Cost of goods sold + Operating expenses ÷ Sales × 100 Cost of goos sold = Sales – Gross profit = 1,60,000 – 50,000 = Rs. 1,10,000 Operating expenses = 4,000 + 22,800 + 1,200 = Rs. 28,000 Operating ratio = 1,10,000 + 28,000 ÷ 1,60,000 × 100 = 86.25 % d. OPERATING NET PROFIT TO NET SALES RATIO = Operating Profit ÷ Sales × 100 Operating profit = Net profit + Non-Operating expenses – Non operating income = 28,000 + 800 – 4,800 = Rs. 32,000 Operating Net Profit to Net Sales Ratio = 32,000 ÷ 1,60,000 × 100 = 20 % What is a Financial statement? It is an organised collection of data according to logical and consistent #accounting procedure. It combines statements of balance sheet, income and retained earnings. These are prepared for the purpose of presenting a periodical report on the program of investment status and the results achieved i.e., the balance sheet and P& L a/c. Objectives of Financial Statement Analysis: To help in constructing future plans To gauge the earning capacity of the firm To assess the financial position and performance of the company To know the #solvency status of the firm To determine the #progress of the firm As a basis for #taxation and fiscal policy To ensure the legality of #dividends Financial Statement Analysis Tools Comparative Statements Common Size Statements #Trend Analysis #Ratio Analysis Fund Flow Statement Cash Flow Statement Types of Financial Analysis Intra-Firm Comparison Inter-firm Comparison Industry Average or Standard Analysis Horizontal Analysis Vertical Analysis Limitations Lack of Precision Lack of Exactness Incomplete Information Interim Reports Hiding of Real Position or Window Dressing Lack of Comparability Historical...

Posted by Managementguru in Accounting, Financial Accounting, Financial Management, Principles of Management

on Mar 27th, 2014 | 0 comments

An Analysis to Understand the Art of Accounting Objectives of an Accountant: The pure objective of an accountant would be to record all business transactions that are monetary in nature, in order to ascertain if the company has earned profit or suffered loss during a financial year. The financial position of the company as on a particular date can thus be understood from the accounting journals and ledgers. We are talking about the conventional purpose of accounting. But with the lapse of time, more and more is being expected from accounting, in that, it has to meet the demands and requirements of tax authorities for the purpose of income tax and sales tax returns, government regulations, investors, owners and the management. Thus it can be aptly defined as the art of recording, classifying and summarizing events in a significant manner, that involve money transactions and/ or events that are of financial character, for interpretation. Systematic records for future reference: Book keeping is an accounting practice that tells us how to keep a record of financial transactions. A firm deals with its customers and suppliers, where numerous business transactions take place every day. It is not possible for us to remember every transaction, which we might need it for our reference at a future date. Especially, if it happens to be a credit sale, definitely the necessity of systematic book keeping arises. The owner would like to know, what amount is due from whom, from time to time. To know the financial position of the firm: Every merchant is in business to earn profits. So systematic recording of factual and financial information will facilitate the owner to understand where he stands financially at the end of a financial year, what is his net profit and to pull the ropes tight if credit margin is wide. Further more, he can also understand the nature of his business growth by comparing the accounting records of two consecutive years. Taxation purposes: Some people evade tax, but no one can avoid tax. The main source of revenue generation for government is tax payments from business merchants and corporate companies. You need to pay a percentage as tax, in accordance with profit arising from sales. The accounting records that you maintain contain facts that are taken into account by the taxation authorities as a basis for assessment. https://amzn.to/2sl5aL7 Good evidence in the court of law: To prove your genuinity, in case of some disputes between yourself and the customer or supplier, your records and vouchers, if authentic and valid, are going to speak for you in the court of law as solid evidence. Accounting also answers some of these questions: How well the different departments of business have performed all along? What is the most profitable product line? What are the products whose production has to be increase and what is to be stopped in order to avoid losses? Is the cost of production reasonable or excessive? Is there a need to revise policy decisions to improve the profitability? What will be the future plans of business in the wake of existing results presented to the management? Overall, is the firm proceeding towards the right direction in terms of productivity, profitability and growth? Accounting is not only about recording and classifying, the interesting features being analysis and interpretation, which are the key factors for the development of the organization as a whole. Note: The Comptroller and Auditor General of India (CAG),is the head of the Supreme Audit Institution of India (SAI) CAG is the sole auditor of the accounts of the Central (Union) Government and the State Governments. CAG is also responsible for the audit...

Posted by Managementguru in Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

The main aim of management accounting is to help an organization in its functions of planning, directing, controlling and areas of specialization included within the admit of management accounting. The main concern of management accounting is to provide necessary quantitative and qualitative information to the management for planning and control. For this purpose it draws out information from accounting as well as non-accounting sources. Hence, its scope is quite vast and it includes within its fold almost all aspects of business operations.