Posted by Managementguru in Accounting, Economics

on Feb 17th, 2014 | 0 comments

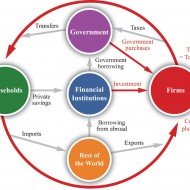

National Accounting Concepts Why knowing about national accounting concepts is important? National income data are of great importance for the economy of a country. In modern days they are regarded as the accounts of an economy, which are known as social accounts. Social accounts tell us how the aggregate of a nation’s revenue, output and product result from the income of different individuals, products of industries and transactions of international trade. National policy formulations: The computation of national income forms a basis for a nation to develop its policies for important spheres of action such as employment policies, monetary policies and fiscal policies that determine the growth of an economy. These figures enable us to know the direction which the industrial output, investment, saving etc. take and proper measures can be adopted to bring the economy on the right path. Facilitates Planning: Gross Domestic Product Gross National Product Net Domestic Product Net National Product Per Capita Income Disposable Personal Income All these factors comprise the national income and indicate the money value of the flow of goods and services available annually in an economy. Also this statistics helps a nation for proper economic planning. The per capita income refers to the earning capacity of individuals in an economy and more the per capita income, higher is the economic welfare of a country. Uncontrolled population growth and unemployment are major reasons for low per capita income. The wealth cannot be evenly distributed owing to high birth rates and low mortality rates and making the ends meet with the available scant resources becomes a major problem for developing countries. Distribution of income From the data pertaining to wages, rent, interest and profits, we learn of the disparities in the incomes of different sections of the society. Similarly the regional distribution of income is revealed. It is only on the basis of these that the government adopts measures to remove inequalities in income distribution and attempts at regional equilibrium. There have been differences of opinion regarding ‘nation’ in the concept of national income. In the calculation process, the term ‘nation’ has to be defined exactly as to whether it is the geographical entity of the country to be taken up for computing national income or the incomes earned by the nationals including those residing abroad. Further, since everything has to be equated to the money value, services produced in the economy out of love for humanity cannot be brought under the term national income. Besides, there is an overlapping of occupations, especially in the rural sector of certain countries, which makes it difficult to know about incomes from various...

Posted by Managementguru in Economics, Financial Management, Management Accounting

on Feb 14th, 2014 | Comments Off on Concept of Cost

The concept of cost along with demand and supply constitute three of the basic areas of managerial economics. Analysis of cost is essential when it comes to large-scale production, where the firm is in a position to factorize the economies of scale. For a profit-maximizing firm, the decision to add a new product is done by comparing additional revenues to additional costs associated with that project. Aids in Decision Making Decisions on capital investment are made by comparing rate of return on investment with the opportunity cost of the funds used to make capital acquisition. Costs are equally important in non-profit sector. For example, to obtain funding for a new dam, a government agency has to demonstrate that the value of the benefits of the dam like flood control and water supply, will exceed the cost of the project. It is necessary that we define the term ‘cost’ for better understanding. The traditional definition tends to focus on the explicit and historical dimensions of cost. In contrast, the economic approach to cost emphasizes opportunity cost rather than historical and includes both explicit and implicit costs. Opportunity Cost Opportunity costs are fundamental costs in economics, and are used in computing cost benefit analysis of a project. Such costs, however, are not recorded in the account books but are recognized in decision making by computing the cash outlays and their resulting profit or loss. Opportunity cost is the minimum price that would be necessary to retain a factor-service in it’s given use. It is also defined as the cost of sacrificed alternatives. For instance, a person chooses to forgo his present lucrative job which offers him Rs.50000 per month, and organizes his own business. The opportunity lost (earning Rs. 50,000) will be the opportunity cost of running his own business. Fixed and Variable Cost: A company’s total cost is composed of its total fixed costs and its total variable costs combined. Variable costs vary with the amount produced. Fixed costs remain the same, no matter how much output a company produces. Semi-variable is the type of costs, which have the characteristics of both fixed costs and variable costs. Fixed costs and variable costs comprise total cost. Total cost is a determinant of a company’s profits which is calculated as: Profits = Sales – Total Costs. The cost which remains same, regardless of the volume produced, is known as fixed cost. A variable cost is a corporate expense that changes in proportion with production output. Variable costs increase or decrease depending on a company’s production volume; they rise as production increases and fall as production...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

Liquidity Ratio or Working Capital Ratio Liquidity ratio indicates that the firm has sufficient liquid resources to meet its short-term liabilities. It measures the ability of the firm to meet its short-term obligations, i.e., capacity of the firm to pay its current liabilities as and when they fall due. Also known as “short-term solvency ratio” or “working-capital ratio”. Thus these ratios reflect the short-term financial solvency of a firm. The various ratios that explains about the liquidity of the firm are Current Ratio Acid Test Ratio / quick ratio Absolute liquid ration / cash ratio 1. CURRENT RATIO The current ratio measures the short-term solvency of the firm. It establishes the relationship between current assets and current liabilities. It is calculated by dividing current assets by current liabilities. An ideal ratio would be 2:1 which provides margin of safety to the creditors and financial stability. Current Ratio = Current Assets Current Liabilities Current assets cover cash and bank balances marketable securities inventory, and debtors, excluding provisions for bad debts and doubtful debtors Bills receivables and prepaid expenses. Current liabilities include sundry creditors bills payable short- term loans income-tax liability Accrued expenses and dividends payable. 2. ACID TEST RATIO / QUICK RATIO/LIQUID RATIO It has been an important indicator of the firm’s liquidity position and is used as a complementary ratio to the current ratio. It establishes the relationship between quick assets and current liabilities. It is calculated by dividing quick assets by the current liabilities. Acid Test Ratio = Liquid Assets Current liabilities Liquid ratio is the true test of business solvency. The ideal ratio is 1:1 which indicates sound financial position. 3. ABSOLUTE LIQUID RATION / CASH RATIO It shows the relationship between absolute liquid or super quick current assets and liabilities. Absolute liquid assets include cash, bank balances, and marketable securities. Absolute liquid ratio = Absolute liquid assets Current...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

Ratio Analysis – An Introduction What is Ratio? The relationship between two variables expressed mathematically is called a ratio. It refers to the systematic use of ratios to interpret the financial statements in terms of operating performance and financial position of a firm. Some important definitions: “The relation of one amount, a to another b, expressed as the ratio of a to b”– Kohler “Ratio is the relationship or proportion that one amount bears to another, the first number being the numerator and the later denominator” – H.G.Guthmann Significance of ratio analysis: It consolidates and simplifies the accounting information or data It is a clear indicator of an organisation’s efficiency It helps in the evaluation of a firm’s performance by comparing the past and present ratio It aids the management in formulating poilicies, preparing budgets etc., It points out the liquidity position thereby assisting in assessing the short-term obligations and long-term solvency It facilitates inter-firm and intra-firm comparison, the former to understand the position of firm in the market and latter to gauge the performance of different divisions of the firm. Since ratios have the power to speak, they are considered as effective means of communication A broad classification of ratios: Pic Courtesy : Financial Ratios CLASSIFICATION BY FUNCTION 1. Solvency Short-term Long-term Current ratio Proprietory ratio Liquid ratio Debt-Equity ratio 2. Profitability Gross profit ratio Net profit ratio Operating profit ratio Return on Investment ratio 3. Activity ratio Fixed assets turnover ratio Debitors turnover ratio Creditors turnover ratio Stock turnover ratio 4. Leverage Financial leverage ratio Operating leverage ratio Capital gearing ratio CLASSIFICATION BY STATEMENTS 1. Balance sheet ratios Current ratio Liquid ratio Proprietory ratio Debt-Equity ratio Capital Gearing ratio 2. Profit and Loss Account ratios or Profitability ratios Gross profit ratio Net profit ratio Operating profit ratio Return on Investment ratio 3. Inter-Statement ratios or Turn-over ratios Fixed assets turnover ratio Debitors turnover ratio Creditors turnover ratio Stock turnover...

Posted by Managementguru in Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

Advantages of Management Accounting It helps to increase the efficiency of all functions of management.It helps in target-fixing, decision-making, price-fixing, selection of product-mix and so onForecasting and Budgeting help the concern to plan the future and financial activities.Various tools and techniques provide reliability and authenticity to carry out the business functions.It is useful in controlling wastage and defects.It helps in complete communication between all levels of management.It helps in controlling the cost of production thus increasing the profit percentage.It is proactive-analyses the governmental policies and socio-economic scenario which helps to assess the external environmental impacts on the organization. Limitations of Management Accounting It is concerned with financial and cost accounting. If these records are not reliable, it will affect the effectiveness of management accounting.Decisions taken by the management accountant may or may not be executed by the management..It is very expensive. Only big concerns can adopt this method of accounting.New rules and regulations are to be framed, hence there is a possibility of opposition from the employees.It is only in the developing stage.It provides only data and not decisions.It is a tool to the management and not an alternative of management. These are the advantages and limitations of management accounting. Characteristics of management accounting Following are the characteristic features of management accounting: First and foremost characteristic is that it provides the necessary information to the management. It might be any data- numbers, gross profit, net profit, comaparitive financial statements, profit and loss account etc.,It is purely analytical.The interpretations help the management in timely decision-making.It adopts a selective technique to arrive at the results.Helps to chart-out the future course of action.Also helps to know the present financial condition of the firm and the respective implications on the stake holders. Various tools of management accounting: MARGINAL COSTINGSTANDARD COSTINGBUDGETARY CONTROLRATIO ANALYSISFUND FLOW ANALYSISCASH FLOW ANALYSIS...