Posted by Managementguru in Accounting, Business Management, Financial Accounting

on Jul 2nd, 2014 | 0 comments

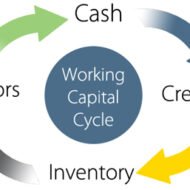

Understanding Working Capital: It is the life blood of business. Funds needed for the purchase of raw materials, payment of wages and other day-to-day expenses are known as working capital. It is part of the firm’s capital, which is being used for financing short-term operations. Hence, it may also be termed as Circulating Capital or Short-Term capital. “Working capital means current assets” –Mead, Malott and Field. “Any acquisition of funds which the current asset increases working capital, for, they are one and the same.” – J.S.mill Financial troubles and issues arise only when this entity called ‘working capital’ is not properly managed. Every successful company will hire a financial manager to deal with issues relating to finance while the CEO can look into matters relating to promotion of the product or service and the position of the company in the market. The ‘Sales Turnover or Sales Volume’ is the key issue you have to look into to gauge whether you have sufficient working capital to manage that big a volume for that particular period. You have to rotate your funds wisely keeping in mind the credit policies your company offers and the credits you may enjoy with your supplier, bank interest for the short-term loans etc. Concept of WC: Working capital implies excess of current assets over current liabilities. Funds invested in current assets is known as “Gross Working Capital.” The difference between current assets and current liabilities is known as “Net Working Capital.” What are the two types? Permanent or fixed: It is the minimum amount of current assets required for conducting the business operation. This capital will remain permanent in current assets and should be financed out of long-term funds. The amount varies from year to year, depending upon the growth of a company. Temporary or Variable: It is the amount of additional current assets required for a short period. It is needed to meet the seasonal demands at different times during a year. The capital can be temporary and should be financed out of short-term funds. The working capital starts decreasing when the peak season is over. Various Factors Influencing WC: Nature of business: Service oriented concerns like electricity; water supplies need limited working capital while a manufacturing concern requires sufficient working capital, since they have to maintain stock and debtors. Credit Policies: A company which allows credit to its customers shall need more amount while a company enjoying credit facilities from its suppliers will need lower amount of working capital. Manufacturing Process: Conversion of raw materials into finished goods is called manufacturing or production. Longer the process, higher the requirement of working capital. Rapidity of turnover: High rate of turnover requires low amount and lower and slow moving stocks need a larger amount of working capital. Say, jewelry shops have to maintain different types of designs calling for high working capital. Fast moving goods like grocery requires low working capital. Business cycle: Changes in economy has a say over the requirement of working capital. When a business is prosperous, it requires huge amount of capital; also during depression huge amount is needed for unsold stock and uncollected debts. Seasonal variation: Industries which are manufacturing and selling goods seasonally require large amount of working capital. Fluctuation of supply: Firms have to maintain large reserves of raw material in stores, to avoid uninterrupted production which needs large amount of working capital. Dividend policy: If a conservative dividend policy is followed by the management, the need for working capital can be met with the retained earnings, it consequently drains off large amounts from working capital pool. ...

Posted by Managementguru in Business Management, Change management, Human Resource

on Jun 25th, 2014 | 0 comments

Smith et al. describe management as “Making Organizations perform”. Management is concerned with Individuals who are delegated authority to manage others – Let me call them ‘People with Power’. Activities for achieving goals – ‘Real Action Plans’. A body of knowledge represented by theories and frameworks about people and organizations – ‘Policy Framework’. What do managers do? As we all know they are involved in general management functions like Forecasting Planning Organizing Motivating Co-ordinating Controlling Are you aware of the ‘hidden’ dimensions of a manager’s job? Modern management theories, although highlighting the complexity of the role, have yet to provide sufficient empirical research and advice into key areas that enable both managers and organizations to increase their effectiveness. For example Dealing competently with organizational politics (“You can ignore it, but it won’t go away” – This is how surveyed employees said they viewed office politics) Successfully managing change (Adaptability is about the powerful difference between adapting to cope and adapting to win) Controlling ethical issues and demands (It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.) Developing the role of women managers (Women can be better managers than men because they tend to be more conservative and do their homework. Men tend to take more risk without the research) Ensuring personal ‘survival’ and career success in organizations (A successful man is who lays a firm foundation with the bricks others throw at him.) Safeguarding personal health in a stressful environment (Manage stress before it manages you). How to achieve a more comprehensive view of development? Frameworks for setting, linking, and balancing individual and organizational objectives. Systems for identifying and selecting managers Structures to support, motivate and reward Plans to enable career progression Mechanisms to measure and evaluate performance. HRM and Management Development Human resource management as the name suggests is about the effective management of people in organizations. HRM involves the integration of people with business goals and strategies HRM views people as assets to be developed and utilized in a productive way rather than costs to be minimized or eliminated. The philosophies, ideologies, values and beliefs of management that operate and dominate within the organization have an impact on people management. The practices, policies and management styles that managers employ in their managerial role also align people’s behavior towards organizational goals. Senior managers determine the extent to which people are integrated into the organization’s strategic plans. They set the agenda and create the culture climate of prevailing values, attitudes and behavior. Middle and junior managers translate and ‘operationalize’ broader human resource strategies and policies. They give HRM its meaning and reality. It is their perfect management style and actual behavior that decided how the human resources is deployed and managed and thus what people experience as human resource management. The way managers themselves are managed and developed is a significant influencing factor in the way people are subsequently...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Jun 25th, 2014 | 0 comments

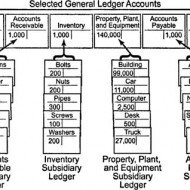

Ledger is a register with pages numbered consecutively. Each account is allotted one or more pages in the Ledger. If one page is completed, the account will be continued in the next page. An index of various accounts opened in the Ledger is given at the beginning of the Ledger for the purpose of easy reference. A general ledger is a complete record of financial transactions that holds account information needed to prepare financial statements, and includes accounts for assets, liabilities, owners’ equity, revenues and expenses. What is meant by Posting? Transactions recorded in the Journal and Subsidiary journal are transferred to the concerned accounts in the Ledger in a summarized and classified form. This process is called posting. Interesting Statistics on Accounting The first book on double-entry accounting was written in 1494 by Italian mathematician and Franciscan friar Luca Bartolomeo de Pacioli. Although double-entry bookkeeping had been around for centuries, Pacioli’s 27-page treatise on the subject has earned him the title “The Father of Modern Accounting. Accounting plays a major role in law enforcement. The FBI counts more than 1,400 accountants among its special agents. The state of New York gave its first certified public accountant (CPA) exam in 1896. Rules for posting: 1. Separate account should be opened in the Ledger for posting transactions relating to separate persons, assets, expenses or losses as shown in the journal. 2. The account concerned which has been debited in the journal should also be debited in the Ledger. However, a reference must be made of the other account which is to be credited in the journal. In other words, in the account to be debited, the name of the other account to be credited is entered in the debit side for giving a meaning to this posting. The debit posting is prefixed by the word ‘To’. 3. Similarly, the account concerned which has been credited in the journal has to be credited in the Ledger, but a reference should be made to the other account which has been debited in the journal. This posting is prefixed by the word ‘By’. Advantages of keeping a Ledger: Ledger provides information regarding all transactions of a particular account whether it is personal a/c, Real a/c or nominal a/c. The final effect, of a series of transactions of a certain customer or a certain property or a certain expense is known at a glance. Ledger provides immediately the totality of certain dealings. E.g., total purchases, Total sales, total expenditure, on a specified head. What is a Ledger account? Give a Proforma of a Ledger account. A Ledger account is nothing but a summary statement of all transactions relating to a person, asset, expense or income, which have taken place during a given period of time showing their net effect. Proforma of a Ledger account: What are the methods of balancing the Ledger account? At the end of the each month or year or any specific day it is essential to determine the balance in an account. To do that, add the totals of both sides (Debit and credit sides) and find out the difference in both the sides. The difference in both the sides is ‘Balance’. If the Debit is greater than the credit side, it is a Debit balance or vice-versa. There are two methods: The bigger total is taken first and is written on both sides of the account. On the smaller side, the balance is Witten above the total next to the last entry on that side. This method is more commonly used. In another method, the totals are written on both sides, one side showing smaller amount and the other showing bigger amount. The...

Posted by Managementguru in How To, Human Resource, Interview Questions, Organisational behaviour, Stress Management

on Jun 21st, 2014 | 0 comments

A job interview can be viewed as a mutual “exchange of information” because it provides the candidate with an opportunity to both gain information about the department and position, and to discuss his/her own skills, and career goals in relation to the job. Interviewing helps managers determine three things before they make a hiring decision. 1. Can you do the job? 2. Are you motivated to do the job? 3. Are you a good fit in the organization? Acing yourself is an important part of the interview process. The time you spend gearing up before the interview will be time well spent in your job search process. The following are some tip-offs on what you can do to prepare yourself before, during, and after a job interview. Before the Interview Assess the Job Specification and Position Description Review your résumé and be prepared to discuss your appropriate skills. Decide who your references are. A current or past manager, coworker, teacher/professor or associate may come in handy to vouch for your skills/accomplishments. Be ready with extra copies of your résumé Dress for Success -Appearance should display maturity and self-confidence. Be neat, clean, and dress in good taste. Find out where the interview will be, obtain clear directions, and confirm the time. Plan to arrive 10- 15 minutes early. During the Interview Relax! Think of the interview as a conversation, not a cross-examination Be whole-hearted, self-assured, polite, and open. Listen to the questions carefully and give clear, crisp, and precise answers. Convey interest in the organization and knowledge of the position. Ask relevant questions about the job or department. Present a list of your references and any letters of recommendation or reference that you may have to offer. End the interview with a firm handshake and thank the interview panel for their time and consideration. After the Interview Send a crisp thank-you letter within 24 to 48 hours of the interview. Reiterate your interest in the position; mention the key skills you know that strengthen your place in the organization, and your contact information. If you are not chosen for the job, it is OK to graciously accept your defeat and ask the interviewer which area(s) you could improve on in the future!...

Posted by Managementguru in Business Management, Marketing, Operations Management, Technology

on Jun 18th, 2014 | 0 comments

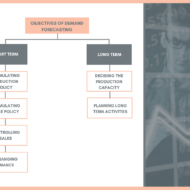

Objectives of Forecasting The objective of this post is to impart some light on the uses and importance of forecasting and to get you acquainted with various forecasting techniques. What is Forecasting? Forecasting is a technique that uses historical data as inputs to make informed estimates that are predictive in determining the direction of future trends. And also to know how these techniques are used in an organization’s decision making process. Nature of Forecast A forecast is an estimate of an event which will happen in future – be it, demand of a product, rainfall at a particular place, population of a country, or growth of a technology.It is estimated based on the past data related to a particular event and hence it is not a deterministic quantity.In any industrial enterprise, forecasting is the first level decision activity before consolidating other decision problems like, materials planning, scheduling, type of production system.Forecasting provides a basis for co-ordination of plans for activities in various units of a company.All the functional managers in any organization will base their decision on the forecast value. So, it provides vital information for that organization. Classification of Forecasts Technology forecastsEconomic forecastsDemand forecasts 1. Technology Forecast Technology is a combination of hardware and software. Hardware is any physical product while software is the know-how, technique or procedure. Technology forecast deals with certain characteristics like level of technical performance, rate of technological advances. It is a prediction of the future characteristics of useful machines, products, process, procedures or techniques. TIFAC – Technology Information Forecasting and Assessment Council is an autonomous organization set up in 1988 under the Department of Science & Technology. In 1993, TIFAC embarked upon the major task of formulating a Technology Vision for the country in various emerging technology areas. 2. Economic Forecast Government agencies and other organizations involve in collecting data and prediction of estimate on the general business environment. Economic forecast This involves the application of statistical models utilizing variables sometimes called indicators. Some of the most well-known economic indicators include inflation and interest rates, GDP growth/decline, retail sales and unemployment rates. This is used to predict future tax revenues, level of business growth, level of employment, level of inflation etc. Also, these will be useful to business circles to plan their future activities based on the level of business growth. 3. Demand Forecast This gives the expected level of demand for goods or services. This is the basic input for business planning and control. Hence, the decisions for all the functions of any corporate house are influenced by demand forecast. Factors Affecting Demand Forecast Business cycleRandom variationCustomer’s planProduct’s life cycleCompetitor’s efforts and pricesCustomer’s confidence and attitudeQualityCredit policyDesign of goods or servicesReputation for serviceSales...