Posted by Managementguru in Business Management, Decision Making, Financial Management, Human Resource, Principles of Management, Strategy

on Mar 30th, 2014 | 0 comments

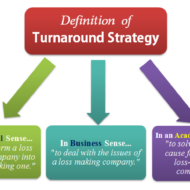

What is Turnaround Strategy Distress signals start flying around when a particular company, whether multinational, corporate or medium sized, is subjected to financial pressure and is at the brink of bankruptcy. What was happening all along? No body knows and nobody wants to be held responsible. The CEO has to bear the brunt and alas, extermination! Aim of Turn-around Strategy: The overall aim of a turn around strategy is to bring back a firm to normalcy which has been under distress in terms of acceptable levels of profitability, solvency, liquidity and cash flow. Turn around strategies should be very carefully formulated so as to stabilize the firm in distress, i.e., to bring the company out of the hole and then go for long term planning. Turn around can be in the form of operational efficiency management, financial restructuring, marketing management or savings in the form of cost reduction or liquidity in the form of asset reduction. Facebook Marketing: A Step-by-Step to Your First 1000 Fans! Turn around to see what is around: We have seen so many such occurrences at the global level and micro level. Some companies rejuvenate like a phoenix bird from the ashes, some go haywire, and some dissolve into thin air. It all depends how well you handle the situation with either the help of an external expert consultant or you might want to go for joint venture or collaboration in order to save you skin from mounting interest payments or you right royally sell the company if somebody is ready to takeover. Either way you have to do something! “Turn around to see what is around”. Don’t see what you want to see See what has to be seen Change the CEO (He is the Ideal Victim!) Resurrect your employees’ confidence Cut down costs Look for Alternatives Lie low for Sometime(till the situation favors) Slowly capture the market by innovative Campaigns and ads Paint a new picture about your company Review your Mission and Vision statements Work on targets Bang on the right target customers and clients Strengthen your Channel of Distributors Go smooth with the bankers (You need them always!) Have confidence in yourself Crisis management is necessary Stress busters like yoga and meditation mandatory Evolve Strategies One step at a time (Slow and steady) Fear and Panic grips the organization in situations of crisis. So the first step would be to stay cool to assess the situation by calmly reviewing the damage with all the concerned people. The next step would be to stop the bleeding by cutting all unwanted costs, unnecessary overheads, and the final stage would be renaissance, recovery, renewal or by whatever name you want to call it, even if it means negative investment or profit. Proper Planning, Inventory Control, Strategic prepositions, Renewal of old strategies in accordance with the situation, Tightening finance controls, Defining the credit management limits, all these are precautionary measures which will hold you from falling into the danger of handling a crisis situation, as” recovery of damaged integrity is going to cost you more than ploughing back your profits....

Posted by Managementguru in Business Management, Human Resource, Organisational behaviour, Principles of Management, Training & Development

on Mar 30th, 2014 | 0 comments

Organizational Assessment – Motive and Means Organizational assessment involves creating a picture of “what it is”. The snapshot should provide a clear view of the present position of the company and it should indicate whether there is a need to go for a change process. The data provides a baseline which can be used as a reference point to measure change in the future. Employee opinion surveys and climate surveys form a critical part of this measurement process. The key to an effective assessment is being clear about the goal of the process and being specific about the questions the intended exercise must answer. Cultural assessment: This provides information about core dimensions of organizational culture which includes satisfaction with the work itself, satisfaction with pay and benefits, opportunities for advancement, satisfaction with leadership and supervision, motivation, common values and performance commitment. If the leader proves to be aggressive, committed, value driven, so will be the employees who obviously take after their leader to fulfill his vision. The purpose behind analyzing the culture of an organization is to determine its efficiency level and to generate recommendations for continuous improvement. This exercise should not be a one-time affair as periodical inputs and feedback are excellent ways to align culture with the vision. In this way, management is better able to anticipate and prevent any potential problem, and to assess employee attitudes regularly. Survey administration: Surveys are administered to large groups of employees at one time and it is emphasized to be anonymous to erase any apprehensions in their minds. Open-ended questions allow employees to express their opinions about areas that need improvement and also the problem areas or bottlenecks that hinder their development. Report generation: The statistics collected is summarized and presented for each and every dimension covered in the survey. The report compares the organization’s current culture with previous administrations of the survey. Such open ended discussions bring out the problem areas which the management had not been previously aware of. Feedback to management and employees: The managers discuss the outcome of the survey in order to gain a better understanding of the various issues facing the organization, and decide on a plan to give feedback to their employees. This is a kind of human resource strategy which helps the management to bridge the gap between various levels of the organization and its members. Recommendations to the management: A final report submission by managers of the respective departments along with their recommendations for management’s perusal is the final step in organizational diagnosis and with the approval of “the big boss” action plans are executed that aid in improving the organizational effectiveness. The notion of this entire exercise is to provide insight into the current skill levels of the work force and to design an effective plan for performance improvement based on the assessment of total development needs....

Posted by Managementguru in Business Management, Change management, Human Resource, Organisational behaviour, Principles of Management, Project Management

on Mar 30th, 2014 | 0 comments

Effective people are preferred to rather than efficient people as the former does the right thing and the latter does things right. Redesigning your workplace not only refers to the infrastructure but also the internal factors that might affect the productivity of your firm. Big corporate firms generally face challenges in the form of Lack of co-operation between subunitsIncreasing complaints from the customersRising Operating costsDip in the moraleMajor changes in technology All these signs are indications of a not so enterprising organizational climate. And it calls for quick decision making regarding introducing some changes that bring some positive development in terms of improved efficiency and increase in productivity. Redesigning Workplace in Response to Exogenous Factors Growth of Organizations The challenges mentioned above may make an organization’s existing structure, management practice or its culture obsolete for the new situation. Growth of an organization should be a result of collaborative effort of all the units of an organization and it is objective and not subjective. An organization is comprised of different elements which interact in deciding the organizational effectiveness. The task or goal, technology, structure, people and the internal and external environment of the firm; all these coexist and hold the firm together. Be it a school, a hospital, a union, a club or a business enterprise the interactive nature of these elements make the process of managing very difficult. Medical tourism and business travel are becoming more popular in Asian countries as it increases the scope of collaboration of industries that can coexist to enjoy a win-win situation. Who is an Effective Manager ? An effective manager anticipates these challenges and proactively initializes a planned change. He strategically prepares the organization to be subject to planned change by manipulating the structure, technology and behavior. Understanding the dimensions of change helps him to manage change better as people are always resistant to change. Modern enterprises right from the start have to install and implement “systems” that are technologically most modern and hire suitable people who are techno-savvy; Because technology rules the world and the development of new software programmes and hardware components feed on themselves every day. Developing an Organization as a Whole Behavior of people is unpredictable but controllable. Individually oriented training and development programmes does not prove much to the benefit of the organization as it creates apprehensions in the minds of the individual that are related to the culture and attitude of his superior and subordinates. The idea of developing the organization as a whole through team building is a better perspective as it renews the enthusiasm of people working for you and as a team they feel more cohesive and adhered. Synergy plays its role in improving the interpersonal relationship amongst the team members. Firms are becoming more modern in their outlook. For instance, a showroom whose purpose is to showcase your products also provides entertainment by its aesthetic value. Only if the customer is impressed by the artistic way of your exhibit, will he enter your showroom. Change is inevitable and it improves the health of an organization. The focus should be on “total system change” and the orientation is towards achieving desired results as a consequence of planned activities. Flat Organizational Structure You would have come across the latest buzz word “flat organizational structure”. This is designed in order to bridge the gap between front line employees and the executive level. If there is only few levels of management, the process of communication is more effective, the art of delegation becomes mandatory and need for participation in the decision making process involves all the employees which in turn reduces bureaucracy. There is no set pattern...

Posted by Managementguru in Financial Management, Management Accounting, Marketing, Principles of Management

on Mar 27th, 2014 | 0 comments

Costing and Profitability Analysis Relationship between Cost of Production and Sales Volume: The cost of production and volume of sales are the inter-dependent determinants of profit. The analysis of cost behavior in relation to the changing volume of sales and its impact on profit is very important to determine the break even level of a firm. The level at which total revenue equals total costs, is said to be the break even level where there is no-profit or no-loss. Sales beyond break-even volume bring in profits. Generally production is preceded by the process of demand forecasting, to decide on the volume of production, the produce of which will be absorbed by the market. Pricing and promotions come at a later stage. Costing is done to predict the costs of production and resultant profits at various levels of activity. Download this comprehensive power-point presentation on Break-Even Analysis. Cost Volume Profit or CVP Analysis: CVP analysis or Cost-Volume-Profit analysis helps a firm to study the interrelationship between these three factors and their effect on clean profit. The process also includes an analysis about the external factors that affect the volume of production, such as market demand, competitor threat and internal factors such as availability of infrastructure, capital and labor force. This CVP analysis is a boon to the managers to locate the bottlenecks that hinder the productivity and find a way out, by adjusting either the levels of activity or controlling the cost. Picture Courtesy : The Power of Break-Even Analysis Pricing: Pricing is the most important factor that makes your product competitive. The costs of production can be classified into fixed costs, variable costs and semi variable costs. Fixed costs remain constant and tend to be unaffected by the changes in volume of output; whereas variable costs vary directly with the volume of output and semi-variable as the name implies are partly fixed and partly variable. Cost accountants of the modern era fully support variable costing for the purpose of cost accounting, listing its merits as follows: Variable costing talks about contribution margin, which is the excess of sales over variable costs. If this is going to be high, sufficient enough to cover the fixed costs, then profit is assured for the firm. It is a key factor to determine the percentage of profit. Variable costing assigns only those costs to a product that varies directly with the changing levels of production, which is helpful in making a distinction of profit made from sales and those resulting from changes in production and inventory. Segregating the costs into fixed and variable is done for the purpose of providing information to reflect cost-volume-profit relationships and to facilitate management decision-making and control. Some applications of variable costing that facilitates management decision making: Profit planning: By increasing the volume of sales or decreasing the selling price of the product. Performance evaluation of profit centres:Like, sales division, marketing department, product line etc., Decide on product priorities: In view of market potential and profit potential Make or Buy Decisions: Depending on the production capacity and sales demand. Budgeting: Flexible budgeting and cost control are possible by variable costing technique and the striking feature is the treatment given to fixed costs, where it is treated as a period cost and not apportioned among all the departments and products that enable the firm to understand the movement of profits in the same direction as that of the sales. Although considered to be a controversial technique and weighed against the conventional methods of costing such as absorption costing, it is believed that it is to stay and exist as the next step in the evolutionary method of cost accounting....

Posted by Managementguru in Accounting, Financial Accounting, Financial Management, Principles of Management

on Mar 27th, 2014 | 0 comments

An Analysis to Understand the Art of Accounting Objectives of an Accountant: The pure objective of an accountant would be to record all business transactions that are monetary in nature, in order to ascertain if the company has earned profit or suffered loss during a financial year. The financial position of the company as on a particular date can thus be understood from the accounting journals and ledgers. We are talking about the conventional purpose of accounting. But with the lapse of time, more and more is being expected from accounting, in that, it has to meet the demands and requirements of tax authorities for the purpose of income tax and sales tax returns, government regulations, investors, owners and the management. Thus it can be aptly defined as the art of recording, classifying and summarizing events in a significant manner, that involve money transactions and/ or events that are of financial character, for interpretation. Systematic records for future reference: Book keeping is an accounting practice that tells us how to keep a record of financial transactions. A firm deals with its customers and suppliers, where numerous business transactions take place every day. It is not possible for us to remember every transaction, which we might need it for our reference at a future date. Especially, if it happens to be a credit sale, definitely the necessity of systematic book keeping arises. The owner would like to know, what amount is due from whom, from time to time. To know the financial position of the firm: Every merchant is in business to earn profits. So systematic recording of factual and financial information will facilitate the owner to understand where he stands financially at the end of a financial year, what is his net profit and to pull the ropes tight if credit margin is wide. Further more, he can also understand the nature of his business growth by comparing the accounting records of two consecutive years. Taxation purposes: Some people evade tax, but no one can avoid tax. The main source of revenue generation for government is tax payments from business merchants and corporate companies. You need to pay a percentage as tax, in accordance with profit arising from sales. The accounting records that you maintain contain facts that are taken into account by the taxation authorities as a basis for assessment. https://amzn.to/2sl5aL7 Good evidence in the court of law: To prove your genuinity, in case of some disputes between yourself and the customer or supplier, your records and vouchers, if authentic and valid, are going to speak for you in the court of law as solid evidence. Accounting also answers some of these questions: How well the different departments of business have performed all along? What is the most profitable product line? What are the products whose production has to be increase and what is to be stopped in order to avoid losses? Is the cost of production reasonable or excessive? Is there a need to revise policy decisions to improve the profitability? What will be the future plans of business in the wake of existing results presented to the management? Overall, is the firm proceeding towards the right direction in terms of productivity, profitability and growth? Accounting is not only about recording and classifying, the interesting features being analysis and interpretation, which are the key factors for the development of the organization as a whole. Note: The Comptroller and Auditor General of India (CAG),is the head of the Supreme Audit Institution of India (SAI) CAG is the sole auditor of the accounts of the Central (Union) Government and the State Governments. CAG is also responsible for the audit...