Posted by Managementguru in Management Accounting

on Oct 23rd, 2014 | 0 comments

Capital Budgeting and Capital Accounting Systems These internal accounting systems facilitate and support decision-makers in assessing potential investments with respect to cost effectiveness. The purpose of capital accounting systems support decision-makers in monitoring and planning liquidity. What is Capital Budgeting? Capital budgeting is the planning process used to determine whether an organization’s long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth the funding of cash through the firm’s capitalization structure. Capital budgeting systems is a framework that support management in making decisions in the context of capital investment decisions. In particular, capital budgeting systems help to determine whether or not a capital investment will earn back the original expenditure and in addition provide a reasonable return. This type of decisions usually entails large amounts of organizational resources at risk and, at the same time, affects the future development of the organization . Capital budgeting systems usually focus on capital investment decisions that cover many years. This discriminates capital budgeting systems from income determination and planning which usually focus on the current period. Capital investment decisions usually encompass cash inflows and outflows that accrue at different points in time which are usually answered by adding accrued interest of discounting of cash-flows. Capital budgeting process consists of six steps: Project Generation Estimation Of Cash-Flows Progress Through The Organization Analysis And Selection Of Projects Authorization Of Expenditures And Post-Audit Investigations. In the step of (1) project generation, potential investments are chosen for which in step (2) potential cash-flows are estimated. In step (3), i.e., progress through the organization, certain projects require approval of top-management. In step (4), analysis and selection of projects, the selected projects are assessed with respect to the fact that cash inflows and outflows usually realize at different points in time. In Step (5), authorization of expenditures, captures the final decision (usually made by top management) on whether or not to invest into the selected project. Finally, in step (6) captures a post-audit investigation, i.e., after a certain period of time actual results might be gained which potentially provide input for control purposes. Capital budgeting systems particularly support management in step (4), i.e., the analysis and selection of projects. Capital accounting systems support management in planning and controlling liquidity. Courtesy: S. Leitner, Information Quality and Management Accounting, Lecture Notes in Economics and Mathematical...

Posted by Managementguru in Accounting, Financial Accounting

on Aug 24th, 2014 | 0 comments

What is meant by Depreciation? It means reduction in the value of a fixed asset used in the business due to #wear and tear and effluxion of time. What is depreciation? Internal and External Causes of depreciation: i. Wear and tear: Caused mainly due to constant use, erosion, rust etc. ii. Efflux of time: Mere passage of time will cause a fall in the value of an asset, even if it is not used. iii. Obsolescence: A new invention or change in fashion or a permanent change in demand may render the asset useless. iv. Depletion: When raw materials or natural resources like mines, quarries and oil wells are extracted continuously, they deplete. v. Accident: An asset may reduce in value because of meeting with an accident, like fire accidents. vi. Fall in the market price. Watch this video on What Is Depreciation – How It Affects Profit And Cash Flow What is the necessity for providing depreciation? According to International Accounting Standard Committee (IASC) “Depreciation is the allocation of the depreciable amount of an asset over its estimated useful life. Depreciation for the accounting period is charged to income either directly or indirectly.” The need for depreciation arises because of the following reasons: To ascertain the true profit of the business for a particular periodTo show the asset at its true value in the balance sheetTo provide funds for replacement of the old asset with a new one Objectives of providing depreciation: To recover the cost incurred on fixed assets over its lifeTo facilitate the purchase of new asset, when the old asset is disposedTo find out the correct profit or loss for the particular periodTo find out correct financial position through balance sheet Factors to be considered while determining the amount of depreciation: I. The total cost of the asset including all freight, insurance and installation charges II. The estimated residual or scrap value at the end of its life III. Estimated number of years of its usefulness It is concerned with charging the cost of fixed assets to operations. But the term depletion refers to the cost allocation for natural resources, whereas the term amortization relates cost allocation for intangible assets. What are the various methods for depreciation? Fixed installment or Straight line or Original cost method.Diminishing Balance Method or Written down value method or Reducing Installment method.Annuity Method.Depreciation fund method or Sinking fund amortization fund method.Insurance policy method.Revaluation method.Sum of the year’s digits method (SYD).Double declining balance method.Depletion method. Related Posts : How to Manage Working Capital?Short Term...

Posted by Managementguru in Accounting, Business Management, Financial Accounting

on Jul 2nd, 2014 | 0 comments

Understanding Working Capital: It is the life blood of business. Funds needed for the purchase of raw materials, payment of wages and other day-to-day expenses are known as working capital. It is part of the firm’s capital, which is being used for financing short-term operations. Hence, it may also be termed as Circulating Capital or Short-Term capital. “Working capital means current assets” –Mead, Malott and Field. “Any acquisition of funds which the current asset increases working capital, for, they are one and the same.” – J.S.mill Financial troubles and issues arise only when this entity called ‘working capital’ is not properly managed. Every successful company will hire a financial manager to deal with issues relating to finance while the CEO can look into matters relating to promotion of the product or service and the position of the company in the market. The ‘Sales Turnover or Sales Volume’ is the key issue you have to look into to gauge whether you have sufficient working capital to manage that big a volume for that particular period. You have to rotate your funds wisely keeping in mind the credit policies your company offers and the credits you may enjoy with your supplier, bank interest for the short-term loans etc. Concept of WC: Working capital implies excess of current assets over current liabilities. Funds invested in current assets is known as “Gross Working Capital.” The difference between current assets and current liabilities is known as “Net Working Capital.” What are the two types? Permanent or fixed: It is the minimum amount of current assets required for conducting the business operation. This capital will remain permanent in current assets and should be financed out of long-term funds. The amount varies from year to year, depending upon the growth of a company. Temporary or Variable: It is the amount of additional current assets required for a short period. It is needed to meet the seasonal demands at different times during a year. The capital can be temporary and should be financed out of short-term funds. The working capital starts decreasing when the peak season is over. Various Factors Influencing WC: Nature of business: Service oriented concerns like electricity; water supplies need limited working capital while a manufacturing concern requires sufficient working capital, since they have to maintain stock and debtors. Credit Policies: A company which allows credit to its customers shall need more amount while a company enjoying credit facilities from its suppliers will need lower amount of working capital. Manufacturing Process: Conversion of raw materials into finished goods is called manufacturing or production. Longer the process, higher the requirement of working capital. Rapidity of turnover: High rate of turnover requires low amount and lower and slow moving stocks need a larger amount of working capital. Say, jewelry shops have to maintain different types of designs calling for high working capital. Fast moving goods like grocery requires low working capital. Business cycle: Changes in economy has a say over the requirement of working capital. When a business is prosperous, it requires huge amount of capital; also during depression huge amount is needed for unsold stock and uncollected debts. Seasonal variation: Industries which are manufacturing and selling goods seasonally require large amount of working capital. Fluctuation of supply: Firms have to maintain large reserves of raw material in stores, to avoid uninterrupted production which needs large amount of working capital. Dividend policy: If a conservative dividend policy is followed by the management, the need for working capital can be met with the retained earnings, it consequently drains off large amounts from working capital pool. ...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Jun 25th, 2014 | 0 comments

Ledger is a register with pages numbered consecutively. Each account is allotted one or more pages in the Ledger. If one page is completed, the account will be continued in the next page. An index of various accounts opened in the Ledger is given at the beginning of the Ledger for the purpose of easy reference. A general ledger is a complete record of financial transactions that holds account information needed to prepare financial statements, and includes accounts for assets, liabilities, owners’ equity, revenues and expenses. What is meant by Posting? Transactions recorded in the Journal and Subsidiary journal are transferred to the concerned accounts in the Ledger in a summarized and classified form. This process is called posting. “Interesting Statistics on Accounting The first book on double-entry accounting was written in 1494 by Italian mathematician and Franciscan friar Luca Bartolomeo de Pacioli. Although double-entry bookkeeping had been around for centuries, Pacioli’s 27-page treatise on the subject has earned him the title “The Father of Modern Accounting. Accounting plays a major role in law enforcement. The FBI counts more than 1,400 accountants among its special agents. The state of New York gave its first certified public accountant (CPA) exam in 1896. Rules for posting: Separate account should be opened in the Ledger for posting transactions relating to separate persons, assets, expenses or losses as shown in the journal. The account concerned which has been debited in the journal should also be debited in the Ledger. However, a reference must be made of the other account which is to be credited in the journal. In other words, in the account to be debited, the name of the other account to be credited is entered in the debit side for giving a meaning to this posting. The debit posting is prefixed by the word ‘To’. Similarly, the account concerned which has been credited in the journal has to be credited in the Ledger, but a reference should be made to the other account which has been debited in the journal. This posting is prefixed by the word ‘By’. Advantages of keeping a Ledger: Ledger provides information regarding all transactions of a particular account whether it is personal a/c, Real a/c or nominal a/c. The final effect, of a series of transactions of a certain customer or a certain property or a certain expense is known at a glance. Ledger provides immediately the totality of certain dealings. E.g., total purchases, Total sales, total expenditure, on a specified head. What is a Ledger account? Give a Proforma of a Ledger account. A Ledger account is nothing but a summary statement of all transactions relating to a person, asset, expense or income, which have taken place during a given period of time showing their net effect. Proforma of a Ledger account: What are the methods of balancing the Ledger account? At the end of the each month or year or any specific day it is essential to determine the balance in an account. To do that, add the totals of both sides (Debit and credit sides) and find out the difference in both the sides. The difference in both the sides is ‘Balance’. If the Debit is greater than the credit side, it is a Debit balance or vice-versa. There are two methods: The bigger total is taken first and is written on both sides of the account. On the smaller side, the balance is Witten above the total next to the last entry on that side. This method is more commonly used. In another method, the totals are written on both sides, one side showing smaller amount and the other showing bigger amount. The difference is...

Posted by Managementguru in Business Management, Financial Accounting, Management Accounting

on Apr 21st, 2014 | 0 comments

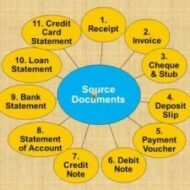

What are the Various Source Documents in Accounting? What is meant by source document? A source document is one used to record the transactions in the books of account. These documents stand as evidence for business transactions. These include Cash Memo Invoice Receipt Debit Note Credit Note Voucher Pay in Slip Cheque etc. 1. Cash Memo: When goods are sold or purchased for cash, the firm gives or receives cash memos with details regarding cash transactions. These documents become the basis for recording these transactions in the books of accounts. 2. Invoice: Invoice is prepared when goods are sold or purchased on credit. It contains the name of the party, quantity, price per unit and the total amount payable. The original copy is sent to the buyer and the duplicate copy is kept as proof of sale and for future reference. Types of Invoice: Inland Invoice – An invoice which is used in internal trade transaction is called as an Inland Invoice. When the goods are sold within a country, the invoice relating to such a transaction is called as an Inland Invoice. Foreign Invoice – An invoice which is prepared for covering an international trade transaction is called as a Foreign Invoice. A number of copies are prepared, maybe even 10 to 12, because a number of authorities require it. Inward Invoice – Inward invoice is received by the buyer from the seller, on receipt of invoice; the buyer stamps it with date of receipt. The inward invoice number is entered in the purchase journal. Outward Invoice – Outward Invoice is a seller’s bill. An invoice which is inward to the buyer is an outward for a seller. It is called outward invoice, because it is sent to the buyer. At least one copy of the invoice is retained by the seller for necessary action and reference. Proforma Invoice – Proforma Invoice is not a real invoice. It is prepared to give a clear idea regarding the amount that would be paid by the buyer if he places an order. This is prepared at the request of the buyer. 3. Receipt: When a firm receives cash from a customer it issues a receipt as a proof of receiving cash. The original copy is handed over to the party making payment and the duplicate is kept for future reference. This document contains date, amount, name of the party and the nature of payment. 5 Kinds of Receipts Small Businesses Should Take Extra Care to Keep Meal & Entertainment Receipts Receipts from Out of Town Business Travels Vehicle Related Receipts Receipts for Gifts Home Office Receipts 4 & 5. Debit and Credit Notes: These are prepared when goods are returned to supplier or when an additional amount is recoverable from a customer. When the purchaser returns the goods to the seller the Purchaser sends a Debit Note to the seller (i.e. the purchaser debits the seller in his books. Purchasers Books) and the Seller sends a Credit Note to the purchaser (i.e. the seller credits the Purchaser in his Books. Sellers Books). Following are the JVs to be passed:- Sales Return inward A/c Dr. To Debtor A/c (Being goods returned by the customer) Creditor A/c Dr. To Goods Return A/c (Being goods sent back to the seller) 6. Voucher: It is a written document in support of a transaction. It is a proof of a particular transaction taking place for the value stated in the voucher. This is necessary to audit the account. In book keeping, voucher is the first document to record an entry. Normally three types of vouchers are used. Receipt voucher Payment voucher Journal voucher RECEIPT VOUCHER Receipt voucher...