Posted by Managementguru in Business Management, Financial Management, Principles of Management, Project Management

on Feb 28th, 2014 | 0 comments

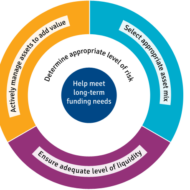

What is Business Risk? It is a term that explains the difference between the expectation of return on investment and actual realization. In CAPITAL BUDGETING, several alternatives of investments are examined before taking an investment decision and only then the Managing Director of the firm along with financial executives gear up for investing in a project that is sound and feasible. Even then the project may not become viable owing to the fluctuations in the economic environment. Money Manipulation So, the million dollar question arises, whether to invest and if invested, will it fetch me profit? See, you cannot have the cake and eat it too. Risk factor prevails in all kinds of environment and we try to over react in a business arena since it involves huge investments. But remember, MONEY WILL MULTIPLY IF YOU MANIPULATE IT WITH CARE. Business firms commit large sums of money each year for capital expenditure. It is therefore essential that a careful FINANCIAL APPRAISAL of each and every project which involves large investments is carried out before acceptance or execution of the project. These capital budgeting decisions generally fall under the consideration of highest level of management. Factors of risk to be considered before investing: Time value of money Pay back period Rate of return on investment(ROI) Uncertainties in the market Cost of debt Cost of equity Cost of retained earnings Factors to be monitored after investing: Maximising profit after taxes Maximizing earnings per share Maintaining the share prices Issue of dividends Ensuring management control Financial structuring Cost of capital refers to the opportunity cost of the funds to the firm I. e., the return on investment to the firm had it invested these funds elsewhere. Servicing the debt and Danger of Insolvency While making the decisions regarding investment and financing, the Finance Manager seeks to achieve the right balance between risk and return. If the firm borrows heavily to finance its operations, then the surplus generated out of operations should be sufficient to “SERVICE THE DEBT” in the form of interest and principal payments. The surplus would be greatly reduced to the owners as there would be heavy Debt Servicing. If things do not work out as planned, the situation becomes worse, as the firm will not be in a position to meet its obligations and is even exposed to the “DANGER OF INSOLVENCY“. Working Capital Management Considering all these factors, we have to come to the conclusion that FINANCIAL MANAGEMENT is like the BACKBONE of a business firm and WORKING CAPITAL MANAGEMENT will be the blood flow infused into the body. Risks are inherent in a business environment whose management is quite possible with the right kind of farsightedness and planning. Luck does not favor anybody who is poor in planning and lack hard...

Posted by Managementguru in Financial Management, Principles of Management

on Feb 28th, 2014 | 0 comments

What forms the Basis for your Investment Decisions? Profit seeking is the ultimate aim of corporate management and the finance manager acts as the anchor point of the management structure. He has to provide specific inputs into the decision-making process, with respect to profitability. Corporate Investment Decisions Cost control What are the Cost Centres? It is the finance manager’s responsibility to have an eagle’s eye on rising costs by continuously monitoring the cost centers of his organization. Production department where there is always a need for additional resources or inflow of funds, should be his first target of contol. Costs are incurred by each and every department of an organization, namely, the production, marketing, personnel and of course finance and accounting. It is a difficult task to control the rising costs. That is the reason why, big corporate companies go for annual budget formulation at the start of the year and reformulates the finance plan by comparing actual with the projected figures. This kind of evaluation helps the firm to fix responsibilities for various centers of operation. Resource Allocation A finance manager is the first person to recognize rising costs for supplies or production, and he can make immediate recommendations to the management to bring back costs under control. While cost control talks about allocating resources to different responsibility centers in the desired proportion, cost reduction focuses on conserving the resources. Cost reduction can be achieved through modifying product and process designs, cutting down throughput time, doubling labor productivity, mass customization, standardistion etc., Pricing Price Fixation It is always a joint venture between marketing and finance departments when it comes to price fixation of products, product lines and services. Pricing decisions are important in that, they affect market demand and the company’s competitive stand in the market. Pricing strategies have to be evolved in the wake of existing competitor strategies and market preference. The demand forecast is the prerequisite factor of the production process and in-depth market analysis and understanding is inevitable on the part of the executives. Future Levels of Profit The finance manager is also responsible for charting out the future levels of profit, based on the relevant data available. He has to consider the current costs, likely increase in costs and likely changes in the ability of the firm to sell its products at the established selling prices. So, it becomes clear that, such market evaluation cannot be periodical, as the market is highly dynamic and has to be done in a day-to-day basis. Before a firm commences a project, its discounted future fund flow and expected profits must be ascertained which will serve as a basis for comparison. Risk versus Return: Investment decisions always are risky as the gestation period of invested funds is very long and not to return immediately. Further, the firm has to calculate the time period in which its initial investment can be recovered and the feasibility of the rate of return on its investment. Fund Management The finance manager is engaged in activities like, mobilization of funds, deployment of funds, and control over the use of funds and also he is to evaluate the risk return trade-off. Profit maximization is the fundamental objective of any organization and the finance manager plays a key role in restructuring the financial philosophy of a firm to take it to greater...

Posted by Managementguru in Financial Management, Principles of Management

on Feb 20th, 2014 | 0 comments

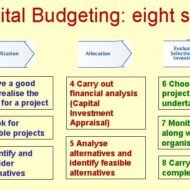

Capital Budgeting- Long Term Resource Planning What is Capital Budgeting? Capital Budgeting refers to the process of planning expenditures that give rise to revenues or returns over a number of years. The process of investment analysis is essential to have a sustainable advantage in the competitive market and to stabilize the profits through resourceful strategic business units. The firm’s management must be on the alert to explore the opportunities present in the market. Obsolete product lines and changes in consumer tastes may present additional problems to a business enterprise affecting the profitability and growth. When a firm decides to venture into projects that demand huge investments, the management has to scrutinize the economic feasibility of such projects. The process of capital investment is also crucial because the projects are for the most part irreversible. Say, for example, if a business firm purchases a special type of machinery, and after installation, if the firm reverses its decision to sell the merchandise due to some technical reasons, it will have only a very small second hand value. Business firms based on the cash flow of the project and the capital recovery period do long-term investment. Why do firms opt for capital budgeting. The reasons may be: To replace worn out equipments that will affect the production efficiency To replace obsolete equipments to install new and more efficient ones To expand production facilities in lieu of increasing demand for the firm’s products and to capture new markets To divest the surplus funds from other business units and to rotate the funds, as idle funds will not generate any revenue To develop new products Research and development Investments made to comply with government regulations, such as projects undertaken to meet government’s health and safety regulations, pollution control and to satisfy other legal requirements. People Involved The proposals for new projects come from the internal environment, such as department heads, executives, employees and of course the management. Experts in product development, marketing research, industrial engineering examine the investment proposals and they may regularly meet with the heads of other divisions in brainstorming sessions to zero in on the proposals. This free course from Udemy is Ideal for people interested in entrepreneurship, fintech, big data, startups, finance, private equity, VCs, & investing. https://www.udemy.com/crowdfund-investing-101-the-basics-of-equity-crowdfunding/ Departments Involved While the firm’s top management makes the final say or decision to undertake or not a major investment project, the process is likely to involve most of the firm’s divisions. Each department has to present its view on the feasibility and viability of the project. The marketing department- on the demand for the new or modified products that the firm plans to sell The production, engineering, personnel and purchasing departments- on the estimation and cost of the investment projects The financing department on- how the required investments funds have to be raised. Thus, the process of expenditure analysis can truly be said to integrate the operation of all the major divisions of the...

Posted by Managementguru in Economics, Financial Management, Management Accounting

on Feb 14th, 2014 | Comments Off on Concept of Cost

Cost-A Key Concept in Economics for Managerial Decision Making The concept of cost along with demand and supply constitute three of the basic areas of managerial economics. Analysis of cost is essential when it comes to large-scale production, where the firm is in a position to factorize the economies of scale. For a profit-maximizing firm, the decision to add a new product is done by comparing additional revenues to additional costs associated with that project. Aids in Decision Making Decisions on capital investment are made by comparing rate of return on investment with the opportunity cost of the funds used to make capital acquisition. Costs are equally important in non-profit sector. For example, to obtain funding for a new dam, a government agency has to demonstrate that the value of the benefits of the dam like flood control and water supply, will exceed the cost of the project. It is necessary that we define the term ‘cost’ for better understanding. The traditional definition tends to focus on the explicit and historical dimensions of cost. In contrast, the economic approach to cost emphasizes opportunity cost rather than historical and includes both explicit and implicit costs. Opportunity Cost: Opportunity costs are fundamental costs in economics, and are used in computing cost benefit analysis of a project. Such costs, however, are not recorded in the account books but are recognized in decision making by computing the cash outlays and their resulting profit or loss. Opportunity cost is the minimum price that would be necessary to retain a factor-service in it’s given use. It is also defined as the cost of sacrificed alternatives. For instance, a person chooses to forgo his present lucrative job which offers him Rs.50000 per month, and organizes his own business. The opportunity lost (earning Rs. 50,000) will be the opportunity cost of running his own business. Fixed and Variable Cost: A company’s total cost is composed of its total fixed costs and its total variable costs combined. Variable costs vary with the amount produced. Fixed costs remain the same, no matter how much output a company produces. Semi-variable is the type of costs, which have the characteristics of both fixed costs and variable costs. Fixed costs and variable costs comprise total cost. Total cost is a determinant of a company’s profits which is calculated as: Profits = Sales – Total Costs. The cost which remains same, regardless of the volume produced, is known as fixed cost. A variable cost is a corporate expense that changes in proportion with production output. Variable costs increase or decrease depending on a company’s production volume; they rise as production increases and fall as production decreases. Feel free to share this infographic on “Concept of Costs” Cost Reduction: Cut Costs and Maximise Profits: Be flooded with ideas on how to cut your...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Feb 13th, 2014 | 0 comments

Bookkeeping involves organizing and managing all business transactions in a company.

Bookkeeping is the recording, on a day-today basis of the financial transactions and information pertaining to a business. Bookkeeping provides the information from which accounts are prepared but is a distinct process, preliminary to accounting.