Posted by Managementguru in Business Management, Decision Making, Organisational behaviour, Principles of Management, Strategy

on Mar 23rd, 2014 | 0 comments

Strategic Evaluation: concerns mainly the analysis and judgment of interventions at the level of strategic goals. One of the noteworthy aspects of strategic evaluation consists of the verification of the adopted strategy with respect to the current and likely social and economic situation. How a firm has performed over time and relatively to its competitors, can be determined with the help of the following quantitative measures. Market price of the sharesMarket shareEarnings on capital employedDividend ratesReturn on equityGrowth in sales volumeProduction costs and efficiencyDistribution costs and efficiencyEmployee turnover, absenteeism, and satisfaction indices. Since there is a high correlation between progress and these indicators, we can say that a firm is successful if majority of the factors show a positive signal. But in reality, one cannot expect a business firm to satisfy all the above mentioned criteria, as performance is also affected by unexpected variations in the external environment. One has to trade-off between the positive and negative indicators and find suitable ways to enhance the performance levels. Effectiveness of a Strategy: The strategic importance of any particular criterion may not remain the same at different points of time. The short run and long run effectiveness of strategy cannot be evaluated using the same criteria. There may be difficulties in computation and different methods of computation that may be encountered in measurement. These factors serve as the bases for firms to identify the elements of success. Yet another way of performance evaluation is to identify critical factors that may be regarded as symptoms of decline and can be treated as early warning signals during the implementation of strategy. If they indicate the necessity of a turnaround or retrenchment strategy, the firm should definitely go for a suitable action without further delay. Such factors may be: Declining profit marginDeclining market shareRapidly increasing debtDeclining working capitalIncreasing managerial turnover What is the Need for Strategic Evaluation? You might be curious to know, what is the need for a strategic evaluation at all in the first instance? See, business firms and corporate companies are always in a position to execute their action plans in the wake of severe competition and retention of market share. A plan without a strategy is like life without a soul and decision making is solely dependent upon strategic inputs. Turnaround Strategy The need for feedback, appraisal and reward, check on the validity of strategic choice congruence between decisions and intended strategy all these help in successful culmination of strategic management process and create inputs for new strategic planning. What’s the difference between Strategy and Tactic? The evaluation need not be based only on quantitative terms, but also on qualitative aspects such as: internal consistency, consistency with the environment, appropriateness of the strategy in the light of available resources, acceptability of the degree of risk involved in the strategy, appropriateness of the time horizon of the strategy...

Posted by Managementguru in Powerpoint Slides

on Mar 10th, 2014 | 0 comments

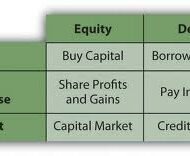

Capital Structure – Debt vs Equity Financial Markets – Instruments and Securities

Posted by Managementguru in Powerpoint Slides

on Mar 2nd, 2014 | 0 comments

Basics of Accounting Purpose of Accounting Break Even Analysis Financial Accounting...

Posted by Managementguru in Accounting, Financial Accounting, Financial Management, Principles of Management

on Feb 28th, 2014 | 0 comments

What is your Capital Structure Make up A company in course of charting out its financial schema has to take into account two things. 1) The amount of capital to be raised. 2) Make-up of the capital. Decisions regarding the composition or capitalization are reflected in capital structure. Capital structure of a firm is a combination of debt and equity, which supports long term financing of the firm. The pattern of capital structure has to be planned very carefully by the finance manager in such a way that it minimizes the cost of capital and maximizes value of stocks, thus protecting the interest of the share holders. What is the right capital mix? There needs to be a right mix of different securities in total cpaitalisation that facilitates control, flexibility and maneuverability. From a broad perspective, following are the three fundamental ways in which the schema of capital structure is finalized: Financing purely or exclusively by equity Financing by equity and preferred stock Financing by equity, preferred stocks and bonds. Which of the above most suits a firm depends on multifarious internal and external factors within which a firm operates. Equity: A firm can raise substantially large amount of fund by issuing different types of shares. The money thus raised is a permanent source of resource and without any obligation to refund to the respective owners. Small and growing companies go for equity fund raising as no banks or other financial institutions are prepared to fund these firms in lieu of poor credit worthiness. Even big corporate firms opt for issuing equities when there is a need to raise large sums. But smaller firms, whose major share of capital comprises of common stock, have to be careful, in that, some large concerns might become interested in controlling these stocks. Picture Courtesy : GrowthFunders The one big advantage of equity shareholders is that they are free to trade the shares in the market. They can sell the shares to anybody at any time and if the market warrants, at a higher price. One has really nothing to lose, if he is planning to invest in equities. On the other hand, if the company goes bankrupt, the share holders stand a chance to receive only the residual amount, after the creditors’ claims are cleared and satisfied. What’s in it for Investors? Debt: Debt has a maturity date upon which the stipulated sum of principal is repaid. It places the burden of obligation on the shoulders of the company in the form of periodical interest settlements and principal repayments. Creditors can go for legal action if the company defaults in payment of the assured sum on the specific date. That’s why companies think twice before they go for issuing debentures and other bonds. One good thing for the company is that, it can avail tax rebate on the securities of debt, but at the other end it has to satisfy the interest payments and factorise the cost of capital. Cost and Control Principles Cost principle supports induction of additional doses of debt, but it might prove risky, if the company is not able to service the additional debt. Control principle supports the issue of bonds in order to tighten the rein of ownership, but maneuverability principle discounts this and favors issue of common stock to reduce the interest burden. Four factors are important in the purview of the finance manager, cost, risk, control and timing. He should be able to evolve a pattern that satisfactorily brings a compromise among these conflicting factors, which are then assigned weights in the wake of economic and industrial...

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

Debtor Management or Receivables Management Profit is directly proportional to the volume of sales, provided all your business transactions are cash based. Is it possible for a manufacturer, wholesaler or retailer to carry on his business without offering credit in this competitive business environment? The answer is a definite “no”, because extension of credit improves your sales and thus your profit. Problems arise only when a firm is not able to recover the debt within the stipulated period of time from the customers. What is receivables management or debtors’ management? It covers two aspects- one, the kind of money that is being invested in debt rotation; second, the risk factor which includes loss of money or the opportunity cost foregone by the organisation. Had these funds not been tied in receivables, the firm would have invested the same elsewhere and earned income thereon. A transaction entirely through cash is definitely a possible option, but whether it is lucrative in the long run must be subject to consideration. When customers are not offered credit, they choose concerns that extend credit facilities and thus you may lose your earlier customers and also exposed to the risk of declining sales proportions. Credit Sales In credit sales, the supplier offers credit for a specific time period, which is an investment from the angle of supplier and largest single source of short term financing from the angle of the customer. The supplier should be able to recover the amount of interest on the credit investment he has made. How? Recovery of debt within the stipulated credit period Taking interest from the customer for the period of delay Volume sales Surplus capital to offset these negative impacts on rotation of funds Proper formulation and execution of credit policies by the finance manager Discipline in collection policy and its execution. Discounts Cash discounts, quantity discounts and trade discounts are offered by many firms to the customers to encourage credit sales, favoring bulk purchases. A firm cannot be expected to survive long by pursuing the policy of cash sales while similar firms can overtake it by adapting to liberal credit policies. The main aspects of receivables management decisions are as follows: Time period of credit Credibility of the customer Cash discounts Trade discounts Learn the basics of the Income Statement, Balance Sheet and Cash Flow Statement and understand how they fit together. Credit Policy Credit policy on one hand stimulates sales and so also its gross earnings, but on the other may be accompanied by added costs, such as: 1) Clerical expenses involved in investigating additional accounts and servicing added volume of receivables, 2) increased bad-debt losses due to credit extension to less credit worthy customers, 3) higher cost of capital. Incremental earnings from increased sales should be matched with incremental costs that arise due to credit terms, to avoid funds being tied up in receivables. In course of time it would deprive you of your profits. The pivotal consideration of your credit policy would be the selection of credit worthy customers or debtors. If your funds become sticky, recovery becomes next to impossible and you need to proceed legally to claim your rights. Properly maintained accounting records and vouchers will stand as a testimony in your favor, in the court of...