Posted by Managementguru in Accounting, Financial Accounting, Management Accounting, Principles of Management

on Nov 27th, 2014 | 0 comments

Some Definitions of Cash Accounting: 1. An accounting method where receipts are recorded during the period they are received, and expenses are recorded in the period in which they are actually paid. Cash accounting is one of the two forms of accounting. The other is accrual accounting, where revenue and expenses are recorded when they are incurred. Small businesses often use cash accounting because it is simpler and more straightforward, and it provides a clear picture of how much money the business actually has on hand. Corporations, however, are required to use accrual accounting under generally accepted accounting principles. 2. An accounting system that doesn’t record accruals but instead recognizes income (or revenue) only when payment is received and expenses only when payment is made. There’s no match of revenue against expenses in a fixed accounting period, so comparisons of previous periods aren’t possible. 3. An accounting method in which income is recorded when cash is received, and expenses are recorded when cash is paid out. Cash basis accounting does not conform with the provisions of GAAP and is not considered a good management tool because it leaves a time gap between recording the cause of an action (sale or purchase) and its result (payment or receipt of money). It is, however, simpler than the accrual basis accounting and quite suitable for small organizations that transact business mainly in cash. Also called cash accounting. Cash Accounting Basics It is the simplest method of accounting. Transactions are recorded only on the actual flow of cash in or out of business. Revenue is recognized only when cash is received from the customer while expenses are recorded only when cash is paid. There cannot be any match of the revenue against expenses in an accounting period. Cash accounting is ideal for sole proprietors or businesses with no inventory. Cash basis is considered beneficial from the taxation point of view as recording income can be put off to the next year and expenses can be booked immediately. Advantages of Cash Basis of Accounting: It is very simple as adjustment entries are not required for prepaid and outstanding expenses. This approach is more objective as very few judgements are required. This is suitable for all organizations whose transactiona are on cash basis. Data can be taken from minimal sources – bank statements, cheque book, deposit book. People with limited accounting knowledge can more easily understand the financial reports,. Disadvantages of Cash Basis of Accounting: It ignores prepaid and outstanding expenses, accrued income and income received in advance. It does not follow the matching principle of accounting. This does not differentiate revenue and capital items, and as a result there is no consistency in the profits of consecutive years. Less insight into long term trends. No structure for invoicing. Does not conform to...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Jun 25th, 2014 | 0 comments

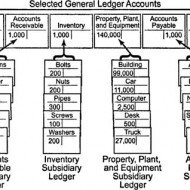

Ledger is a register with pages numbered consecutively. Each account is allotted one or more pages in the Ledger. If one page is completed, the account will be continued in the next page. An index of various accounts opened in the Ledger is given at the beginning of the Ledger for the purpose of easy reference. A general ledger is a complete record of financial transactions that holds account information needed to prepare financial statements, and includes accounts for assets, liabilities, owners’ equity, revenues and expenses. What is meant by Posting? Transactions recorded in the Journal and Subsidiary journal are transferred to the concerned accounts in the Ledger in a summarized and classified form. This process is called posting. “Interesting Statistics on Accounting The first book on double-entry accounting was written in 1494 by Italian mathematician and Franciscan friar Luca Bartolomeo de Pacioli. Although double-entry bookkeeping had been around for centuries, Pacioli’s 27-page treatise on the subject has earned him the title “The Father of Modern Accounting. Accounting plays a major role in law enforcement. The FBI counts more than 1,400 accountants among its special agents. The state of New York gave its first certified public accountant (CPA) exam in 1896. Rules for posting: Separate account should be opened in the Ledger for posting transactions relating to separate persons, assets, expenses or losses as shown in the journal. The account concerned which has been debited in the journal should also be debited in the Ledger. However, a reference must be made of the other account which is to be credited in the journal. In other words, in the account to be debited, the name of the other account to be credited is entered in the debit side for giving a meaning to this posting. The debit posting is prefixed by the word ‘To’. Similarly, the account concerned which has been credited in the journal has to be credited in the Ledger, but a reference should be made to the other account which has been debited in the journal. This posting is prefixed by the word ‘By’. Advantages of keeping a Ledger: Ledger provides information regarding all transactions of a particular account whether it is personal a/c, Real a/c or nominal a/c. The final effect, of a series of transactions of a certain customer or a certain property or a certain expense is known at a glance. Ledger provides immediately the totality of certain dealings. E.g., total purchases, Total sales, total expenditure, on a specified head. What is a Ledger account? Give a Proforma of a Ledger account. A Ledger account is nothing but a summary statement of all transactions relating to a person, asset, expense or income, which have taken place during a given period of time showing their net effect. Proforma of a Ledger account: What are the methods of balancing the Ledger account? At the end of the each month or year or any specific day it is essential to determine the balance in an account. To do that, add the totals of both sides (Debit and credit sides) and find out the difference in both the sides. The difference in both the sides is ‘Balance’. If the Debit is greater than the credit side, it is a Debit balance or vice-versa. There are two methods: The bigger total is taken first and is written on both sides of the account. On the smaller side, the balance is Witten above the total next to the last entry on that side. This method is more commonly used. In another method, the totals are written on both sides, one side showing smaller amount and the other showing bigger amount. The difference is...

Posted by Managementguru in Accounting, Financial Management, Management Accounting, Principles of Management

on Mar 29th, 2014 | 0 comments

Profitability ratios are metrics that assess a company’s ability to generate income relative to its revenue, operating costs, balance sheet assets, or shareholders’ equity. Profitability ratios show how efficiently a company generates profit and value for shareholders. Accounting Basics for Success in Business and in Life! In general two groups of profitability ratios are calculated. Profitability in relation to sales.Profitability in relation to investments. Profitability Ratios can be Classified into five types Gross profit margin or ratioNet profit margin or ratioOperating profit margin or ratioReturn on AssetsReturn on Equity 1. GROSS PROFIT MARGIN OR RATIO It measures the relationship between gross profit and sales. It is calculated by dividing gross profit by sales. Gross profit margin or ratio = Gross profit X 100 / Net salesGross profit is the difference between sales and cost of goods sold. 2. NET PROFIT MARGIN OR RATIO It measures the relationship between net profit and sales of a firm. It indicates management’s efficiency in manufacturing, administrating, and selling the products. It is calculated by dividing net profit after tax by sales. Net profit margin or ratio = Earning after tax X 100 / Net Sales 3. OPERATING PROFIT MARGIN OR RATIO It establishes the relationship between total operating expenses and net sales. It is calculated by dividing operating expenses by the net sales. Operating profit margin or ratio = Operating costs X 100 / Net sales (0r) Cost of goods sold + Operating expenses * 100 / Net sales Operating expenses includes cost of goods produced/sold, general and administrative expenses, selling and distributive expenses. 4. RETURN ON ASSETS Return on assets is the ratio that is used to measure the company’s ability to generate profit by using its whole resource, the assets. It shows the percentage of the net income or net profit comparing to the average total assets. Return on assets shows how efficient the company is in using the assets to generate profits in a period of time. The high return on assets usually shows that the company performs well in making a profit from the assets it has. Return on assets can be calculated by comparing net income or net profit after interest and tax in the period to average total assets. Return on Assets = Net Profit / Average Total Assets 5. RETURN ON EQUITY Return on equity is the ratio that is used to measure the company’s ability to generate profit by using its investors’ money. It shows the percentage of the net income or net profit comparing to the average total equity. Return on equity shows how efficient the company is in using the investor’s money to generate profits in a period of time. The high return on equity usually shows that the company performs well in making profits from its investors’ money. Return on equity can be calculated by comparing net income or net profit after interest and tax in the period to average total equity. Return on Equity = Net Profit / Average Total...

Posted by Managementguru in Operations Management, Project Management

on Feb 24th, 2014 | 0 comments

Materials Handling Minimize Movement and Maximize Productivity Manufacturing organizations handle many types of materials in their production environment. Raw materials, materials-in-progress, finished goods, accessories, components, packaging materials, maintenance and repair supplies, scrap and many more must be handled in an efficient manner to make the operations cost-effective and to avoid wastage. The principle behind material handling process is said to be “no handling”, which is not practicable in reality. So it would be appropriate to say, that the objective of materials handling would be, to reduce the number of handlings as well as reducing the distances through which the materials are handled. Why efficient materials handling is inevitable in a manufacturing set-up? The movement of materials from the receiving area to the shipping area through the production line does not add value to the product but only to the cost. Further, plant layout and materials handling are complementary to each other. A production facility must incorporate a good plant layout that enhances the efficiency of movement of materials with ease and should deliver maximum productivity. Principles for Efficient Materials Handling There are certain principles that serve as a guide for efficient materials handling. These provide a framework for selecting specific materials handling equipments that form the core of the production system. Eliminate handling-If not, reduce the distance travelled by the materials Keep moving-If not, reduce the time spent at crucial points Simple patterns of material flow is appreciated-If not, reduce back tracking, cross overs, congestion Carry pay loads Carry full loads Use reliable and inexpensive source of power Materials handling should be considered in the light of movement of men, machines, tools and information. It also depends on the type of product manufactured, quantity, value and size of the organization. Cost effectiveness can be achieved if the firm is able to reduce the manufacturing cycle time through faster movement of materials and thus work-in-progress inventory costs can also be controlled and reduced. Design of the plant layout that facilitates sequential flow of materials through the production facility, improved working conditions, safety in the movement of materials, contribution to better quality by avoiding damage to the materials due to inefficient handling and workers being appraised about the importance of smooth materials handling result in higher productivity at lower manufacturing cost. Interested in being served food by Robots! Factors to considered while deciding on material handling equipments: Adaptability, flexibility, load capacity, power, speed, nature of supervision required, space requirements, ease of maintenance, environment friendliness and cost are some of the factors to be taken into consideration while deciding on the type of material handling equipments. Also the capabilities of manpower to operate the equipment and safety of personnel cannot be overlooked. It is important to select and design, materials handling system that are expensive to purchase and operate. For instance, if overhead cranes are to be used, the structure of the building should be strong enough to support the installation. Spacious aisles are mandatory if the loads are heavy and transported across the shop floors. Equipments used: Elevators, hoists, industrial trucks like fork-lift trucks, pallet trucks, pipelines, automatic transfer devices, automated guided vehicles, and industrial robots are some of the handling equipments that have found their ideal place in this process. Materials handling activity should be evaluated like any other activity to gauge its effectiveness. The focus should be on the manufacturing cycle efficiency, equipment utilization, percentage of time lost, total number of moves and material handling costs as percentage of manufacturing...

Posted by Managementguru in Accounting, Financial Accounting

on Feb 14th, 2014 | 0 comments

Double Entry System of Book Keeping Accounting is not to be feared Accounting is a subject that is intertwined with our day-to-day lives yet people think it is quite a complicated subject to deal with. The fancy of the subject is such, that many of us fail to understand that it is quite simple, un-complicated and all it talks about is balance. Rather than barging into equations that make us grip with fear, let us start with the basic question of WHAT=WHO? “What” deals with whatever we have in hand or otherwise ASSETS and “Who” deals with the claims, both other’s claims and our own claims on the product we have in hand. Other people’s claims are known as LIABILITIES and our own claim on the product is called Owner’s equity. Now if we take “WHAT=WHO”, it can be translated into the following equation ASSETS= LIABILITIES+OWNER’S EQUITY Accounting: Get Hired Without Work Experience UNDERSTAND WHAT = WHO What = Who Stuff = Who Assets = Who Assets = Who Has Claim Assets = Claims Assets = Other People’s Claims + My Claims Assets = Liabilities + My Claims Assets = Liabilities + My Equity Assets = Liabilities + Owner’s Equity Simple Equation to Remember There are two types of claims: other people’s claims and my claims. Assets = Other People’s Claims + My Claims Claims are also referred to as equities. Assets = Other People’s Equities + My Equity. Accountants have a fancy word for other people’s equities. These are known as liabilities. Assets = Liabilities + My Equity Because I am the owner, we will call My Equity Owner’s Equity. Assets = Liabilities + Owner’s Equity This is the formal equation of accounting. The structure of accounting is based on this one perspective. Accounting students memorize it. And try to decipher it. You are way ahead of the game because you understand that what = who! WHAT ARE ASSETS AND LIABILITIES Assets are on the left of the Big T. Asset accounts increase with debits. Liabilities and Owner’s Equity are on the right of the Big T. They increase with credits. Income ultimately increases owner’s equity so it behaves like owner’s equity: it increases with a credit. Expenses increase with debits. The best way to improve your expertise in accounting procedure is to practice; in due course your hand movement and thought process start synchronizing. Examples of Asset accounts – Vehicles, Furniture, Cash Examples of Liabilities accounts- Accounts payable, Owner’s equity Purchasing a TV- Example ASSETS (what) = LIABILITIES + OWNER’S EQUITY (who) Say if you invest Rs.5,000 as down payment from your end and take a loan of Rs.20,000 from the bank to purchase the product. Now, the bank has a claim on your asset to the extent of Rs.20,000 and your claim is Rs.5000. Here liability is Rs.20,000 and Owner’s equity is Rs.5,000. On the asset side we have a TV worth Rs.25,000 You can see that the value of the asset is equal to the value of liabilities, i.e., what = who. ASSETS = LIABILITIES + OWNER’S EQUITY 25,000 = 20,000 + 5,000 Just how you see a hand with five fingered palm on one side and five fingered nails on the other side, this accounting equation has two different perspectives to strike a balance between assets and liabilities. The Big Balancing ‘T’ The Big Balancing ‘T’ BIG “T” FOR PRODUCT PURCHASE WHAT (ASSET) VEHICLES (Rs.25,000) = WHO (LIABILITIES) ACCOUNTS PAYABLE (Rs.20,000) + PAID IN CAPITAL (Rs.5,000) Do I Debit or Credit? When we receive cash for completing a consulting job we know that cash has increased so we debit cash. The corresponding account...