Posted by Managementguru in Management Accounting

on Mar 24th, 2015 | 0 comments

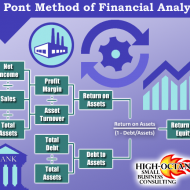

What are the advantages and limitations of ratio analysis? Advantages: It is an important and useful tool to determine the efficiency with which working capital is being managed in a business organization. It is a ‘health test‘ for a business firm in that it can gauge whether the firm is financially healthy or not. It aids the management of business concern in evaluating its financial position and performance efficiency. It clearly shows the trend of changes in the market position (upward, downward or static), as it covers a number of previous accounting (financial) periods. The progress or downfall of a firm is clearly indicated by this analysis. It assists in preparing financial estimates for the future (financial forecasting). It facilitates the task of managerial control to a great extent. It helps the credit suppliers and investors in deciding upon a business firm as a potential investment outlet or desirable debtor. Ideal or Standard ratios can be established which can be used as reference points of comparison for a firm’s progress over a period of time. It communicates important information with relation to financial strength, earning capacity, debt (borrowing) capacity, liquidity position, capacity to meet fixed commitments, solvency, capital gearing, working capital management, future prospects etc. of a business concern. This analysis is also useful for bench marking purpose- to compare the working result and efficiency of performance of a business enterprise with that of other firms engaged in the same industry (inter-firm comparison). It helps the management to discharge their basic functions of planning, coordinating, controlling etc. It serves as an instrument for testing management efficiency too. It acts as a useful tool for deciding on certain policy matters. Limitations: Accounting ratios calculated based on ratio analysis will be correct only if the accounting data on which they are based are correct. It is only an analysis of past financial data. In certain cases ratio analysis might prove to be misleading with regard to profits. Continuous fluctuation in price levels ( or, purchasing power of money) seriously affect the validity or comparison of accounting ratios calculated for different accounting periods and make such comparisons very difficult. Comparisons become difficult also on account of difference in the definition of several financial (accounting) terms like gross profit, operating profit, net profit etc. There is lot of diversity in practice as regards to the measurement of ratios. Different firms use different accounting methods and the validity of comparison is severely affected by window dressing in the basic financial statements. A single ratio will not be able to convey much information. This analysis only gives part of the total information required for proper decision-making. This should not be taken as a substitute for sound judgement. It should not be overlooked that business problems cannot be solved mechanically through ratio analysis or other types of financial analysis. Follow ManagementGuru Net’s board Accounting – Financial and Management Accounting on...

Posted by Managementguru in Accounting, Financial Management, Management Accounting, Principles of Management

on Mar 27th, 2014 | 0 comments

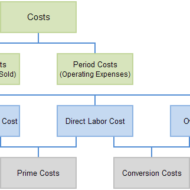

Costing is the technique and process of ascertaining cost whereas cost accounting is the application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and ascertainment of profitability.