Posted by Managementguru in Accounting, Decision Making, Management Accounting, Project Management

on Apr 1st, 2014 | 0 comments

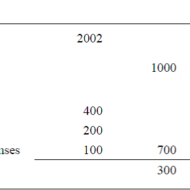

ACCOUNTING AND DECISION MAKING – IDENTIFYING THE PROBLEM SITUATION Learn accounting and finance basics so you can effectively analyze business data to make key management decisions. Business owners are faced with countless decisions every business day. Managerial accounting information provides data-driven input to these decisions, which can improve decision-making over the long term. Fig 1.1- ACCOUNTING INFORMATION FOR A SINGLE PRODUCT The above illustration clearly depicts that there has been a loss of Rs.100 in one year’s time for this particular product. The reason can be attributed to the increase in the “cost of goods” whereas other expenses have remained the same in both the years. For a single product manufactured, the problem is identifiable and solvable. But when the organization is producing a range of products, you need to apply some accounting technique by which the product losing money is identified and suitable measures are taken to cut down the escalating cost. Fig 1.2- Accouning Information for a Product Range The above illustration compares and contrasts the relationship of three products a company manufactures. It is seen that products P1 and P2 are doing well. Though the cost of sales has gone up for P1 and P2, the sales volume has also increased thus increasing the gross profit over the period of time. Here the product that has to be dealt with is P3 whose sales volume has drastically gone down, yet with the same cost of sales. When there is an increase in cost of sales, two things have to be considered. Identifying the problem-product Either cut down the production cost or increase the selling-price if the product has a real demand in the market. Uses of Accounting Data: Accounting information helps the management to arrive at make or buy decisions, to outsource production of certain components to cut down or control costs, to expand the production, to increase the sales volume or to downsize their project capacity. Techniques like Break-Even Analysis, Costing and Budgeting aid in going for the right production-mix, marketing-mix and sales target plans for the respective financial years. Aggregate Planning: As we all know planning is the key to the future and financial planning has to be given utmost importance for a production process. Aggregate planning involves translating long-term forecasted demand into specific production rates and the corresponding labor requirements for the intermediate term. It takes into consideration a period of 6 to 18 months, breaking it into work modules weekly or monthly and planning for the specific period in terms of men, material and...

Posted by Managementguru in Operations Management

on Feb 24th, 2014 | 0 comments

Types of Production Systems -I Continuous Production What is continuous production? The manufacture of products requiring the sequential performance of different processes on a series of multiple machines receiving the material for manufacture through a closed channel. For example, continuous production is generally conducted in the paper and chemical business. Characteristics 1. Dedicated plant and equipment with zero flexibility. 2. Material handling is fully automated. 3. Process follows a fixed sequence of operations. 4. Component materials cannot be readily identified with final product. 5. Planning and scheduling is a routine action. Technical Web Testing 101- Introducing the tools, techniques and thought processes that help you become more technical, and test more thoroughly. Benefits 1. Standardisation of product and process sequence. 2. Higher rate of production with decreased cycle time. 3. Higher capacity utilisation due to line balancing. 4. Manpower is not required for material handling as it is completely automatic. 5. Person with limited skills can be used on the production line. 6. Unit cost is lower due to high volume of production. Limitations 1. Flexibility to accommodate and process number of products does not exist. 2. Very high investment for setting flow lines. 3. Product differentiation is limited. Mass Production What is mass production? The manufacture of a product on a large scale. The mass production of items is often done by using an assembly line, or another efficient means of production. The process is often carefully determined, to try to produce the greatest quantity of items while using the fewest resources (such as labor and/or time). Mass production has become popular since the assembly line became prominent in the 1900s, although the process embodies principles of efficiency that have been around much longer. Characteristics: 1. Standardisation of product and process sequence. 2. Dedicated special purpose machines having higher production capacities and output rates. 3. Large volume of products. 4. Shorter cycle time of production. 5. Lower in process inventory. 6. Perfectly balanced production lines. 7. Flow of materials, components and parts is continuous and without any back tracking. 8. Production planning and control is easy. 9. Material handling can be completely automatic. Benefits 1. Higher rate of production with reduced cycle time. 2. Higher capacity utilisation due to line balancing. 3. Less skilled operators are required. 4. Low process inventory. 5. Manufacturing cost per unit is low. Limitations Following are the limitations of Mass Production: 1. Breakdown of one machine will stop an entire production line. 2. Line layout needs major change with the changes in the product design. 3. High investment in production facilities. 4. The cycle time is determined by the slowest...