Posted by Managementguru in Accounting, Financial Management, Management Accounting, Principles of Management

on Mar 27th, 2014 | 0 comments

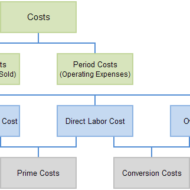

Costing is the technique and process of ascertaining cost whereas cost accounting is the application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and ascertainment of profitability.

Posted by Managementguru in Economics, Financial Management, Management Accounting

on Feb 14th, 2014 | Comments Off on Concept of Cost

Cost-A Key Concept in Economics for Managerial Decision Making The concept of cost along with demand and supply constitute three of the basic areas of managerial economics. Analysis of cost is essential when it comes to large-scale production, where the firm is in a position to factorize the economies of scale. For a profit-maximizing firm, the decision to add a new product is done by comparing additional revenues to additional costs associated with that project. Aids in Decision Making Decisions on capital investment are made by comparing rate of return on investment with the opportunity cost of the funds used to make capital acquisition. Costs are equally important in non-profit sector. For example, to obtain funding for a new dam, a government agency has to demonstrate that the value of the benefits of the dam like flood control and water supply, will exceed the cost of the project. It is necessary that we define the term ‘cost’ for better understanding. The traditional definition tends to focus on the explicit and historical dimensions of cost. In contrast, the economic approach to cost emphasizes opportunity cost rather than historical and includes both explicit and implicit costs. Opportunity Cost: Opportunity costs are fundamental costs in economics, and are used in computing cost benefit analysis of a project. Such costs, however, are not recorded in the account books but are recognized in decision making by computing the cash outlays and their resulting profit or loss. Opportunity cost is the minimum price that would be necessary to retain a factor-service in it’s given use. It is also defined as the cost of sacrificed alternatives. For instance, a person chooses to forgo his present lucrative job which offers him Rs.50000 per month, and organizes his own business. The opportunity lost (earning Rs. 50,000) will be the opportunity cost of running his own business. Fixed and Variable Cost: A company’s total cost is composed of its total fixed costs and its total variable costs combined. Variable costs vary with the amount produced. Fixed costs remain the same, no matter how much output a company produces. Semi-variable is the type of costs, which have the characteristics of both fixed costs and variable costs. Fixed costs and variable costs comprise total cost. Total cost is a determinant of a company’s profits which is calculated as: Profits = Sales – Total Costs. The cost which remains same, regardless of the volume produced, is known as fixed cost. A variable cost is a corporate expense that changes in proportion with production output. Variable costs increase or decrease depending on a company’s production volume; they rise as production increases and fall as production decreases. Feel free to share this infographic on “Concept of Costs” Cost Reduction: Cut Costs and Maximise Profits: Be flooded with ideas on how to cut your...