Posted by Managementguru in Accounting, Decision Making, Management Accounting, Project Management

on Apr 1st, 2014 | 0 comments

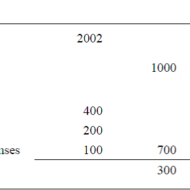

ACCOUNTING AND DECISION MAKING – IDENTIFYING THE PROBLEM SITUATION Learn accounting and finance basics so you can effectively analyze business data to make key management decisions. Business owners are faced with countless decisions every business day. Managerial accounting information provides data-driven input to these decisions, which can improve decision-making over the long term. Fig 1.1- ACCOUNTING INFORMATION FOR A SINGLE PRODUCT The above illustration clearly depicts that there has been a loss of Rs.100 in one year’s time for this particular product. The reason can be attributed to the increase in the “cost of goods” whereas other expenses have remained the same in both the years. For a single product manufactured, the problem is identifiable and solvable. But when the organization is producing a range of products, you need to apply some accounting technique by which the product losing money is identified and suitable measures are taken to cut down the escalating cost. Fig 1.2- Accouning Information for a Product Range The above illustration compares and contrasts the relationship of three products a company manufactures. It is seen that products P1 and P2 are doing well. Though the cost of sales has gone up for P1 and P2, the sales volume has also increased thus increasing the gross profit over the period of time. Here the product that has to be dealt with is P3 whose sales volume has drastically gone down, yet with the same cost of sales. When there is an increase in cost of sales, two things have to be considered. Identifying the problem-product Either cut down the production cost or increase the selling-price if the product has a real demand in the market. Uses of Accounting Data: Accounting information helps the management to arrive at make or buy decisions, to outsource production of certain components to cut down or control costs, to expand the production, to increase the sales volume or to downsize their project capacity. Techniques like Break-Even Analysis, Costing and Budgeting aid in going for the right production-mix, marketing-mix and sales target plans for the respective financial years. Aggregate Planning: As we all know planning is the key to the future and financial planning has to be given utmost importance for a production process. Aggregate planning involves translating long-term forecasted demand into specific production rates and the corresponding labor requirements for the intermediate term. It takes into consideration a period of 6 to 18 months, breaking it into work modules weekly or monthly and planning for the specific period in terms of men, material and...

Posted by Managementguru in Financial Management, Management Accounting, Marketing, Principles of Management

on Mar 27th, 2014 | 0 comments

Costing and Profitability Analysis Relationship between Cost of Production and Sales Volume: The cost of production and volume of sales are the inter-dependent determinants of profit. The analysis of cost behavior in relation to the changing volume of sales and its impact on profit is very important to determine the break even level of a firm. The level at which total revenue equals total costs, is said to be the break even level where there is no-profit or no-loss. Sales beyond break-even volume bring in profits. Generally production is preceded by the process of demand forecasting, to decide on the volume of production, the produce of which will be absorbed by the market. Pricing and promotions come at a later stage. Costing is done to predict the costs of production and resultant profits at various levels of activity. Download this comprehensive power-point presentation on Break-Even Analysis. Cost Volume Profit or CVP Analysis: CVP analysis or Cost-Volume-Profit analysis helps a firm to study the interrelationship between these three factors and their effect on clean profit. The process also includes an analysis about the external factors that affect the volume of production, such as market demand, competitor threat and internal factors such as availability of infrastructure, capital and labor force. This CVP analysis is a boon to the managers to locate the bottlenecks that hinder the productivity and find a way out, by adjusting either the levels of activity or controlling the cost. Picture Courtesy : The Power of Break-Even Analysis Pricing: Pricing is the most important factor that makes your product competitive. The costs of production can be classified into fixed costs, variable costs and semi variable costs. Fixed costs remain constant and tend to be unaffected by the changes in volume of output; whereas variable costs vary directly with the volume of output and semi-variable as the name implies are partly fixed and partly variable. Cost accountants of the modern era fully support variable costing for the purpose of cost accounting, listing its merits as follows: Variable costing talks about contribution margin, which is the excess of sales over variable costs. If this is going to be high, sufficient enough to cover the fixed costs, then profit is assured for the firm. It is a key factor to determine the percentage of profit. Variable costing assigns only those costs to a product that varies directly with the changing levels of production, which is helpful in making a distinction of profit made from sales and those resulting from changes in production and inventory. Segregating the costs into fixed and variable is done for the purpose of providing information to reflect cost-volume-profit relationships and to facilitate management decision-making and control. Some applications of variable costing that facilitates management decision making: Profit planning: By increasing the volume of sales or decreasing the selling price of the product. Performance evaluation of profit centres:Like, sales division, marketing department, product line etc., Decide on product priorities: In view of market potential and profit potential Make or Buy Decisions: Depending on the production capacity and sales demand. Budgeting: Flexible budgeting and cost control are possible by variable costing technique and the striking feature is the treatment given to fixed costs, where it is treated as a period cost and not apportioned among all the departments and products that enable the firm to understand the movement of profits in the same direction as that of the sales. Although considered to be a controversial technique and weighed against the conventional methods of costing such as absorption costing, it is believed that it is to stay and exist as the next step in the evolutionary method of cost accounting....

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

Debtor Management or Receivables Management Profit is directly proportional to the volume of sales, provided all your business transactions are cash based. Is it possible for a manufacturer, wholesaler or retailer to carry on his business without offering credit in this competitive business environment? The answer is a definite “no”, because extension of credit improves your sales and thus your profit. Problems arise only when a firm is not able to recover the debt within the stipulated period of time from the customers. What is receivables management or debtors’ management? It covers two aspects- one, the kind of money that is being invested in debt rotation; second, the risk factor which includes loss of money or the opportunity cost foregone by the organisation. Had these funds not been tied in receivables, the firm would have invested the same elsewhere and earned income thereon. A transaction entirely through cash is definitely a possible option, but whether it is lucrative in the long run must be subject to consideration. When customers are not offered credit, they choose concerns that extend credit facilities and thus you may lose your earlier customers and also exposed to the risk of declining sales proportions. Credit Sales In credit sales, the supplier offers credit for a specific time period, which is an investment from the angle of supplier and largest single source of short term financing from the angle of the customer. The supplier should be able to recover the amount of interest on the credit investment he has made. How? Recovery of debt within the stipulated credit period Taking interest from the customer for the period of delay Volume sales Surplus capital to offset these negative impacts on rotation of funds Proper formulation and execution of credit policies by the finance manager Discipline in collection policy and its execution. Discounts Cash discounts, quantity discounts and trade discounts are offered by many firms to the customers to encourage credit sales, favoring bulk purchases. A firm cannot be expected to survive long by pursuing the policy of cash sales while similar firms can overtake it by adapting to liberal credit policies. The main aspects of receivables management decisions are as follows: Time period of credit Credibility of the customer Cash discounts Trade discounts Learn the basics of the Income Statement, Balance Sheet and Cash Flow Statement and understand how they fit together. Credit Policy Credit policy on one hand stimulates sales and so also its gross earnings, but on the other may be accompanied by added costs, such as: 1) Clerical expenses involved in investigating additional accounts and servicing added volume of receivables, 2) increased bad-debt losses due to credit extension to less credit worthy customers, 3) higher cost of capital. Incremental earnings from increased sales should be matched with incremental costs that arise due to credit terms, to avoid funds being tied up in receivables. In course of time it would deprive you of your profits. The pivotal consideration of your credit policy would be the selection of credit worthy customers or debtors. If your funds become sticky, recovery becomes next to impossible and you need to proceed legally to claim your rights. Properly maintained accounting records and vouchers will stand as a testimony in your favor, in the court of...