Posted by Managementguru in Financial Accounting, Financial Management, How To, Human Resource

on Jun 24th, 2019 | 0 comments

Starting a Small Business? Here Are 4 Ways to Pay Your Employees Hiring employees is a major milestone for any business owner who has previously done it alone. Even if the help is quite welcome, some important related decisions will almost always need to be made. This is true even of the most basic issues, such as how workers will be paid. Fortunately, business owners who are armed with a bit of knowledge will always be equipped to choose appropriately. Taking the Next Step Toward Long-Term Success Sole proprietors who have no workers to worry about, deal with what are generally among the simplest of all possible business arrangements. As soon as employees enter the picture, issues like employment taxes need to be accounted for, lest the government’s wrath descend upon a business owner. Many entrepreneurs find it worthwhile to make use of small business payroll services that virtually rule such problems out. Being able to rely on the expertise of specialists makes potentially costly mistakes a lot less likely and provides a firm foundation for future growth. Determining the Best Way to Pay Any Company’s Workers Even with payroll being handled by an expert, though, business owners still face an important choice. Pay can actually be issued in any of at least the following four common ways, each of which comes with certain benefits and drawbacks. Choosing the means most appropriate to a particular company and its workers will always make things easier, in general. The four options that are available to most business owners when it comes to paying workers are: Checks. Bank drafts authorized by means of check are traceable, accessible, and well-established. The paper trail that writing and depositing or cashing a check creates can prove useful if any issues arise later on. On the other hand, not everyone today has access to an account that can be used to convert a check into a balance. Workers who are forced to cash their checks by other means sometimes end up paying a fair amount for the privilege. Direct deposit. As the more modern relative of the old-fashioned check, direct deposit is an increasingly appealing option. In this case, things are even more restrictive, though, as only employees who have accounts in good standing will be able to make use of this approach. Unfortunately, about 1.7 billion adults worldwide still lack such resources entirely. Prepaid cards. Certain cards associated with networks like those operated by Visa and Mastercard can also be loaded with paychecks on demand. Particularly where some workers might not have checking accounts, this is an increasingly popular choice. Some payroll cards, however, impose maintenance fees and the like, so business owners will always do well to put in plenty of research. Cash. Although it might sometimes seem a bit crude, cash is still very much a valid way to pay wages. Relatively few business owners opt for this approach, though, because of the exposure and hassles it tends to create. The Right Choice is Usually Clear Business owners who wish to do the most they can for their employees will always put some thought into choosing a means of payment. In many cases, it will even make sense to offer at least a couple of choices, from which each worker can select the most personally appropriate. In practice, it tends to be fairly straight forward to figure out how best to pay any small business’s employees....

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting, Principles of Management

on Nov 27th, 2014 | 0 comments

Some Definitions of Cash Accounting: 1. An accounting method where receipts are recorded during the period they are received, and expenses are recorded in the period in which they are actually paid. Cash accounting is one of the two forms of accounting. The other is accrual accounting, where revenue and expenses are recorded when they are incurred. Small businesses often use cash accounting because it is simpler and more straightforward, and it provides a clear picture of how much money the business actually has on hand. Corporations, however, are required to use accrual accounting under generally accepted accounting principles. 2. An accounting system that doesn’t record accruals but instead recognizes income (or revenue) only when payment is received and expenses only when payment is made. There’s no match of revenue against expenses in a fixed accounting period, so comparisons of previous periods aren’t possible. 3. An accounting method in which income is recorded when cash is received, and expenses are recorded when cash is paid out. Cash basis accounting does not conform with the provisions of GAAP and is not considered a good management tool because it leaves a time gap between recording the cause of an action (sale or purchase) and its result (payment or receipt of money). It is, however, simpler than the accrual basis accounting and quite suitable for small organizations that transact business mainly in cash. Also called cash accounting. Cash Accounting Basics It is the simplest method of accounting. Transactions are recorded only on the actual flow of cash in or out of business. Revenue is recognized only when cash is received from the customer while expenses are recorded only when cash is paid. There cannot be any match of the revenue against expenses in an accounting period. Cash accounting is ideal for sole proprietors or businesses with no inventory. Cash basis is considered beneficial from the taxation point of view as recording income can be put off to the next year and expenses can be booked immediately. Advantages of Cash Basis of Accounting: It is very simple as adjustment entries are not required for prepaid and outstanding expenses. This approach is more objective as very few judgements are required. This is suitable for all organizations whose transactiona are on cash basis. Data can be taken from minimal sources – bank statements, cheque book, deposit book. People with limited accounting knowledge can more easily understand the financial reports,. Disadvantages of Cash Basis of Accounting: It ignores prepaid and outstanding expenses, accrued income and income received in advance. It does not follow the matching principle of accounting. This does not differentiate revenue and capital items, and as a result there is no consistency in the profits of consecutive years. Less insight into long term trends. No structure for invoicing. Does not conform to...

Posted by Managementguru in Accounting, Financial Management, Management Accounting, Principles of Management

on Mar 27th, 2014 | 0 comments

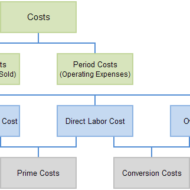

Costing is the technique and process of ascertaining cost whereas cost accounting is the application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and ascertainment of profitability.

Posted by Managementguru in Financial Accounting, Financial Management

on Feb 20th, 2014 | 0 comments

What is fund ? Cash, total current assets, net current assets and net working capital are also interpreted as fund. So, it is necessary to clearly define the meaning of fund and demarcate its scope and function. To put it precisely, fund is nothing but, net working capital of a firm. The flow of fund occurs when a business transaction takes place that leads to an increase or decrease in the amount of fund. Firms prepare fund flow statement to explain the sources and applications of fund, which also serves as a technical tool to ascertain the financial condition of a business enterprise. Balance Sheet In a business firm, everyday numerous financial transactions take place. These are summarized into a balance sheet that gives an idea about the assets and liabilities at a specific point of time. When two balance sheets of consecutive periods are compared, we come to know about the inflow and outflow of funds and thereby the net working capital available is ascertained. This is step one. Profit and Loss Statement The next step would be to prepare an adjusted profit and loss account to determine fund inflow or fund lost from business operations. Accounts have to be prepared to ascertain hidden information (for all non-current items of assets and liabilities). Finally fund lost or gained from operations is arrived at and presented in a statement form. It is not that, only accountants could understand these operations and adjustments. Any person with logical reasoning and business acumen can understand the nuances of accounting, of course with some guidance. Few points that highlight the ways in which funds flow outside and inside a business enterprise will give you a better idea on the nature of fund flow: Sources of fund: Sale of fixed assets – sale of land, building, machinery, furniture etc. But you have to take into consideration a factor called “depreciation“. It is nothing but the wear and tear of the assets due to continuous usage, reduction in market value over a period of time, obsolescence, accidents etc. Remember, land is a non-depreciable asset in developing countries like India, whereas it may not be so in certain developed countries where the real estate values are nose diving. Issue of Equity shares – To raise capital free of interest, many big corporate firms go for equity capital from the general public. But the firms should make it a point to declare dividends if it happens to reap enormous profit to retain their market share. Their main aim should be to protect the interests of the equity share holders who are also the owners. Fund that comes into the firm through business operations – through sale of goods and services. Here the firm has to factorise its cost of production and economy of scale in order to make it cost-effective and fix a feasible profit margin. Borrowing of loans from banks and other financial institutions – Although it is a quick way of raising fund, care should be exercised in that, you should be in a comfortable position to “service the debt“. If not, there lurks the danger of bankruptcy where the firm might become insolvent, if it is unable to repay the interest and principal over a period of time. Issue of debentures – Debentures are also a form of equity but it comes with a price. The firm has to pay a percentage as interest on debentures and repayment period is also fixed in advance. The only solace for the firms would be the tax rebate that can be availed on loans and...

Posted by Managementguru in Accounting, Financial Accounting, Management Accounting

on Feb 14th, 2014 | 0 comments

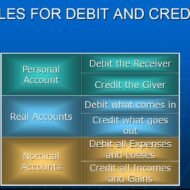

Classification of Accounts Accounts are classified as follows: •Accounts in the names of persons are known as “Personal Accounts” •Accounts in the names of assets are known as “Real Accounts” •Accounts in respect of expenses and incomes are known as “Nominal Accounts” Personal Accounts: It deals with accounts relating to persons, firms, companies and man-made institutions. It is further classified into three categories as shown below. PERSONAL ACCOUNTS NATURAL PERSON’S A/C : e.g- David, Customer ARTIFICIAL PERSON’S A/C : e.g- Banks, firms, companies REPRESENTATIVE’S A/C : e.g- Capital, Drawings Real Accounts These are accounts of assets or properties. Assets may be tangible or intangible. Real accounts are impersonal which are tangible or intangible in nature. Eg:- Cash a/c, Building a/c, etc are Real Accounts related to things which we can feel, see and touch. Goodwill a/c, Patent a/c, etc Real Accounts which are of intangible in nature. Nominal Accounts These accounts are impersonal, but invisible and intangible. Nominal accounts are related to those things which we can feel, but can not see and touch. All “expenses and losses” and all “incomes and gains” fall in this category. Eg:- Salaries A/C, Rent A/C, Wages A/C, Interest Received A/C, Commission Received A/C, Discount A/C, etc. DEBIT AND CREDIT Each accounts have two sides – the left side and the right side. In accounting, the left side of an account is called the “Debit Side” and the right side of an account is called the “Credit Side”. The entries made on the left side of an account is called a “Debit Entry” and the entries made on the right side of an account is called a “Credit Entry”. Golden Rules of Book-Keeping Personal Accounts : DEBIT THE RECEIVER & CREDIT THE GIVER Real Accounts : DEBIT WHAT COMES IN & CREDIT WHAT GOES OUT Nominal Accounts : DEBIT ALL EXPENSES AND LOSSES & CREDIT ALL INCOME AND GAINS What is an accounting equation? It is a statement of equality between the debits and the credits. It explains that the assets of a business are always equal to the total of liabilities and capital. It is also called the balance sheet eqaution. Assets = Liabilities + Capital A = L + C ASSETS ARE THE TOTAL VALUE OF PROPERTIES OWNED BY THE BUSINESS LIABILITIES ARE THE RIGHTS OF THE THIRD PARTIES TO THE PROPERTIES OF THE BUSINESS OR THE AMOUNT DUE BY THE BUSINESS TO THE THIRD PARTIES. Basics of accounting – Accounting Equations Made Simple With Solid Clarity from Shyama...