Currently Browsing: Financial Management

Posted by Managementguru in Architecture and Interior Design, Business Management, Financial Management, Project Management, Real Estate Investment

on Mar 25th, 2022 | 0 comments

Getting onto the property ladder is a life goal for many people, particularly those who want to own their homes and have the freedom to create the perfect living space for themselves. However, while becoming a homeowner is great in its own right, real estate is possibly one of the best options available if you are looking for general investment opportunities. If this sounds interesting to you, here are a few benefits of investing in real estate that you might want to know. A Great Source of Income If you own multiple properties, this could be an excellent opportunity to make some additional income. You could either choose to lease your vacant property to tenants and make a profit from the rent charges, but if you do choose to become a landlord, be aware that there are certain legal obligations and regulations that you will need to follow. Alternatively, if you are not looking for full-time tenants to manage, you could lease the second property as a vacation rental or do some renovations to it to boost its value and sell it for a profit. If you want help with the legal side of purchasing and selling properties, search for specialist attorneys such as the Avenue Law Firm. Tax Breaks While there are expenses to consider if you are going to invest in real estate, you might also find that you are eligible for certain perks when it comes to tax deductions. If you are using the property as a source of income, you could deduct the cost of owning and managing the building within reason from your taxed income. Demand Whether you are looking to lease commercial property or residential, there will always be a demand for it. While there are still risks involved in investing in real estate, generally speaking, it is one of the more stable areas to invest in due to this high demand. As this demand increases, you can raise your rents to match these prices, particularly if the area surrounding your properties is becoming more desirable and make larger profits as a result. Building Equity If you want to improve your overall net worth, building equity is a good way to do this and real estate investment, in particular. As you pay off the mortgage on a property, your equity increases, and this can give you more leverage should you want to invest in other properties or make other investments. Back-Up Residence Another perk of owning more than one property is that it can provide a back-up home to stay in should your main residence need renovations, is damaged, or some other circumstance has resulted in you having to move out temporarily or permanently, provided it was vacant at the time, and you weren’t leasing it out to anyone. This would mean a more comfortable living environment for you should you ever have to leave your usual home. If you have been thinking about making some investments and have been wondering about real estate as an option, consider these benefits and see if they would work well for...

Posted by Managementguru in Financial Management, How To, Personal Finance

on Mar 22nd, 2022 | 0 comments

The majority of households go through times when their finances are a little out of control; it is a question of being able to catch them before they start really spiraling downwards. That can be the hardest part since you have to admit to yourself that things will have to change in order for control to be regained. Whatever you are going through, you can be guaranteed that you are not alone, which is good because it means that there are businesses and people out there to help and give advice, even about the trickiest financial issues. Draw up a budget plan Regardless of whether you feel that you are swimming against the tide with your finances or that you’re doing well, it is a good idea to draw up a budget plan and stick to it. This is so that all your hard-earned money doesn’t get flittered away and will instead be spent on things that you enjoy. Obviously, if you are finding things tight, then a budget will help you reach the goals that you’ve set and can provide that little piece of willpower that you may struggle to find in certain situations. Reduce your outgoings This can be easier said than done; however, there are savings that can be had even if it is only a couple of dollars off of your electricity bill. Changing your utility suppliers can reduce your monthly outgoings, as they often have special offers available; similarly, if you let your supplier know that you are looking to move, they may be willing to do a deal in order to keep your business. However, if you feel that you could very well be past this stage and you are looking into bankruptcy, you will have probably asked yourself the important question of will I lose my home if I file bankruptcy, and this is where you will need more specialist help. Filing for bankruptcy is not an easy decision to come to, and having a specialist on board to take care of you and answer all your questions honestly could be a way to put your mind at rest. Change the way you shop When the money situation is not going well, one of the best ways you can cut back on your spending is to change the way you shop. This does not mean to say that you must go without, as this is a very hard thing to do and can mean that you will resent your new lifestyle. If you are the sort of person that likes to go clothes shopping every week to buy the latest trends, then you may find that going once a month could very well suit your pocket better, or if you like to focus on label buys, then sourcing used clothes from the manufacturer or stores that you buy from could drop the price tag enough that it then becomes an affordable luxury. Now you know how to stay on top of your...

Posted by Managementguru in Business Management, E Commerce, Entrepreneurship, How To, How to make money online, International Business, Sales

on Jul 10th, 2021 | 0 comments

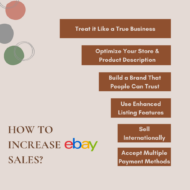

While it is a platform that has been around for many years since the internet started to take off in popularity, eBay continues to be a hugely profitable and useful place to do business. However, there are plenty of other people who have realised exactly the same thing, so you need to be on top of your game to ensure that you stand out from the crowd. Here are a few tips that you can put into practice: Decide What to Sell It may seem like a very obvious starting point, but it is certainly worth mentioning nevertheless. You need to have a clear idea of what you are actually going to be selling in the first place. Obviously, you need a product that works for you – one that you can easily source and ideally know something about. Don’t forget about logistics here. You need to think about where you are going to be placing the product and consider eBay shipping at Shiply as well. Also, check out if there are any restrictions regarding what you can actually sell online. If you are stuck for items to sell, it is worth researching popular products online. You may well find that there is something out there that proves to strike you well. Set Up Your Store Account The store account is going to be the hub of your business, so not only do you need to ensure that it is properly set up and established, but you should also make sure that you know about all the ins and outs of how it works from a technical standpoint. There are plenty of different packages here, so you need to work out which ones suit you the best. Remember, you want this to be right from the start as people are going to start leaving reviews, and you want to get your scores up as high as possible right from the offset. Make the Business Official The business also needs to be official from a legal standpoint as well. This means that you need to check out the legal structure and work out which one is most appropriate for your company. For example, whether you have the sole proprietorship, partnership, limited liability company, etc. Again, it is worth checking out the ins and outs of what each and every one of these actually mean. Start Selling Now the time has come to start selling your goods on eBay. You should take a moment to understand the fees that you are going to be expected to cover, as well as determining the payment method that you are going to accept from your buyers. You can then create your seller account and your listings. Everything needs to be priced accordingly, and it is a good idea to check out what sort of competition is out there. There you have a few top tips that will hopefully start off your eBay selling journey in the best possible manner and put you on the route to...

Posted by Managementguru in Financial Accounting, Financial Management, How To, Management Accounting, Productivity

on Mar 24th, 2021 | 0 comments

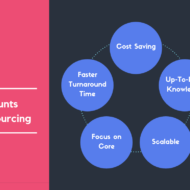

Outsourcing has become increasingly popular over the last few decades as companies have realised that delegating a variety of business operations to a third-party provider can give them a number of benefits. Indeed, outsourcing your business operations can provide you with a number of benefits, especially in relation to your accounting functions while you should also understand that a variety of third-party providers are available on the market. This is especially pertinent if you are starting up a company and you do not have the relevant accounting experience to carry out this particular management function of your business. In addition, you should also be aware that accounting is essential so that you can generate profitability as well as reduce your operating costs. However, if you are unaware about how to go about the process of outsourcing your accounting function, you should think about consulting an online business directory as you will be able to identify a number of providers that you can contact. 1. Increase your profits One of the main benefits that your business could enjoy by outsourcing your accounting function is that you can increase your profitability. Indeed, outsourcing allows you to spend your resources on the important core business operations so that you can generate more profit. This is definitely an advantage if you are looking for an outsourcing provider, such as Acclime, that can give you the highest quality accounting services in Vietnam. It is also important to understand that you can minimise your risk as well as ensure your financial statements are prepared correctly. This is especially pertinent if you do not have the in-house accounting knowledge while making sure your financial statements are correct at all times is imperative if you want to be legally compliant at all times. 2. Reduce your operating costs Furthermore, you should also be aware that outsourcing a particular business function can allow you to reduce your operating costs. Indeed, by outsourcing your accounting function, you will not have to pay salaries or other recruitment expenses to hire qualified and experienced accounting personnel. As a result, you can focus on your core operations if you are just starting out in business, instead of the support functions that are required for you to carry out your business. 3. Improve your decision making process Finally, you should be aware that if you are looking to outsource your accounting function, you can improve your decision making process. Indeed, this is especially important if you hire an experienced and professional third-party provider as they will be able to provide you with information pertaining to your accounts as soon as possible. This can allow you to improve your decision making process as well as yield reliable information so that you can make better decisions in a short amount of time. Increase profitsReduce costsImprove decision makingThe Main Benefits of Outsourcing Accounting Function Therefore, in conclusion, if you are a business owner and you are looking to increase your profitability as well as reduce your operating costs and improve your decision making process, you should consider outsourcing your accounting function to a third-party provider as soon as...

Posted by Managementguru in Accounting, Financial Accounting, Financial Management, How To, Productivity

on Feb 17th, 2021 | 0 comments

Outsourcing is a trend that’s on the rise for a good reason — it works! Almost two-thirds of all businesses outsource some of their positions and processes, and many more are sure to join in soon. You can outsource anything, from marketing to property management, and there are huge benefits to it. Accounting can take a lot of your time and be extremely stressful, but if you outsource it, you can focus on what you do best and leave the pros to deal with the boring stuff. Here are some of the major benefits of outsourcing your accounting. It Can Be Cost-Effective It may seem at first that hiring an in-house team could pay off in the long run, but the truth is quite the opposite. Apart from their regular salaries, there are many expenses you need to account for, such as training, benefits, accounting software and suitable hardware, as well as office supplies, and more. You could train some of your other staff to do accounting, but if they are not sufficiently competent, their mistakes could cost you even more. So enlisting the services of an external accounting provider might prove to make the most financial sense. What’s more, you may not even require their services all the time, but rather call them as needed. It Can Improve Your Operational Efficiency If you have to allocate hours of your busy day to dealing with payroll, bills, and other issues, that can slow down your progress significantly. Instead of running a business and focusing on your main responsibilities, you have to deal with equally important but menial tasks that you could delegate to someone else. However, if you don’t have an accounting team, you would have to burden one of your employees with these tasks, even though you could have used them for something more relevant. The point is, no one in your company has to deal with financial records, invoicing, and similar tasks. If you outsource them, you and your team can focus on your day-to-day operations freely and without hindrances. You Get to Work With Experts in the Field One of the main advantages of hiring an outsourced provider is the fact that you get expert help. You are likely to end up working with an accounting agency, which specializes in all things accounting related, unlike your team. The accountants you hire will have extensive knowledge and experience in what they do, and you can even find someone who specializes in your particular industry. These professionals always strive to improve so that they can offer the most reliable services possible. Moreover, they will make sure to keep track of any potential changes in the law that could affect you in any way. This can be particularly beneficial when it comes to tax benefits and similar issues. You Get Access to Top-Notch Accounting Resources Just like you try to always keep up with the trends in your area of expertise, so do accounting agencies. If you have an in-house accountant, chances are they’ll be stuck working with the same old program for years, without ever updating and missing out on many innovations. An accounting agency wants to stay on top of their game, so naturally, they will make sure to follow the latest industry trends and thus increase their efficiency. That means that your financial information will be analyzed and operated in the most state-of-the-art accounting software. You don’t have to think about updating your hardware or software; your outsourced provider will take care of that. You Don’t Have to Worry About the Security of Your Records You may be surprised to learn that trusted employees all over...